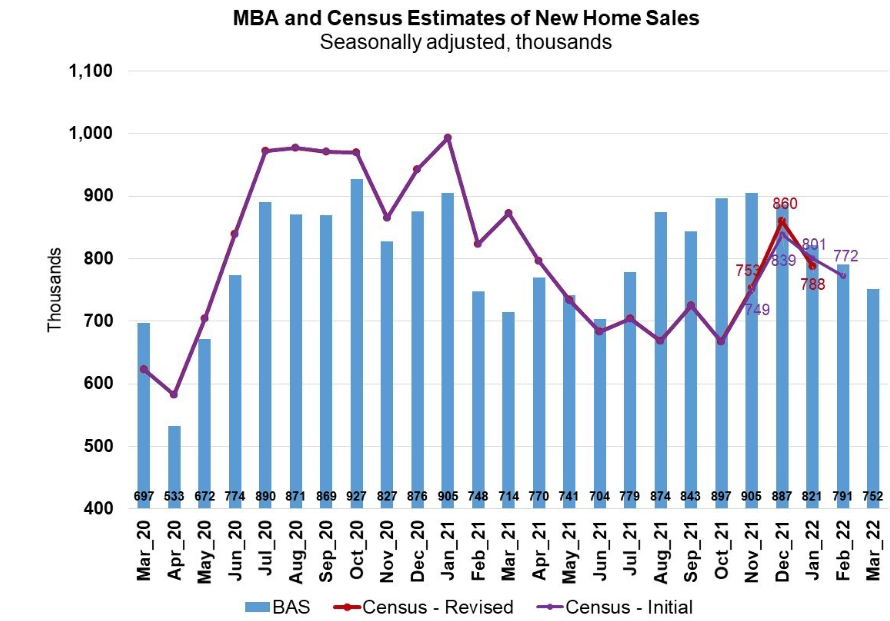

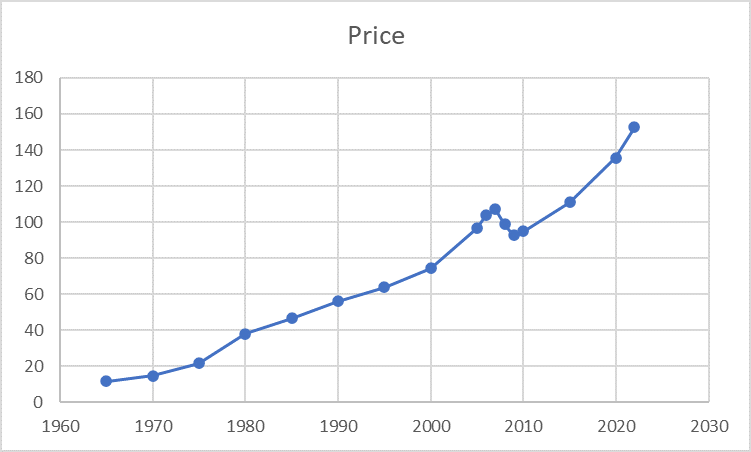

Source: BIS (Bank of International Settlement)

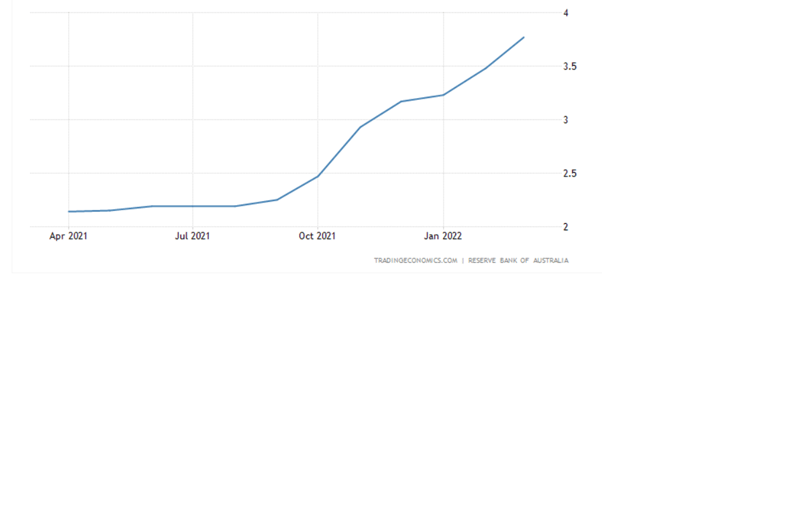

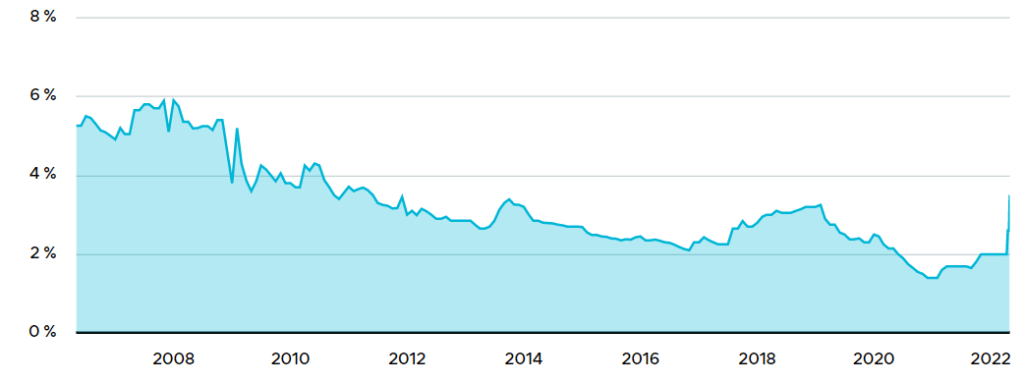

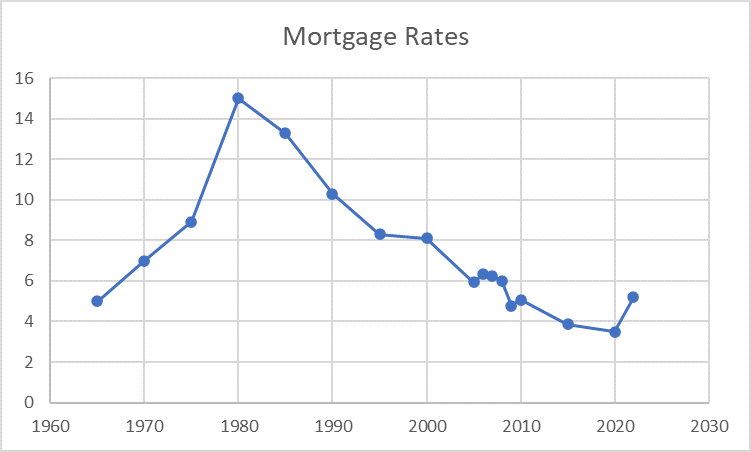

Mortgage Rate Chart

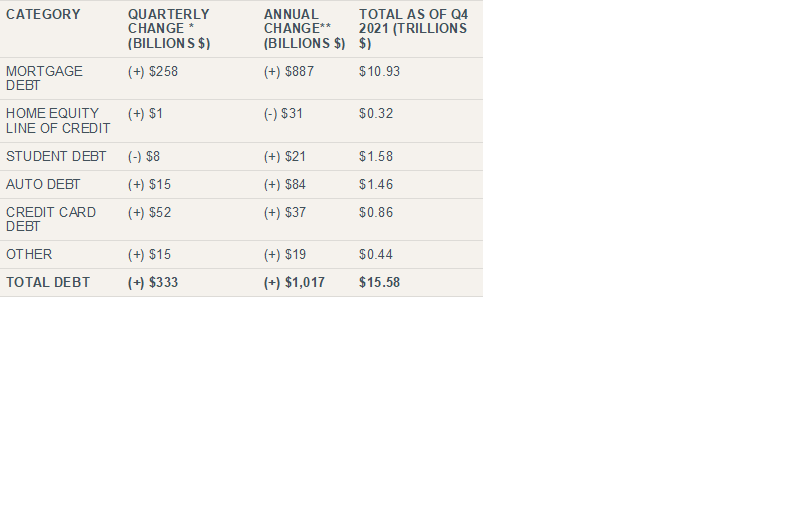

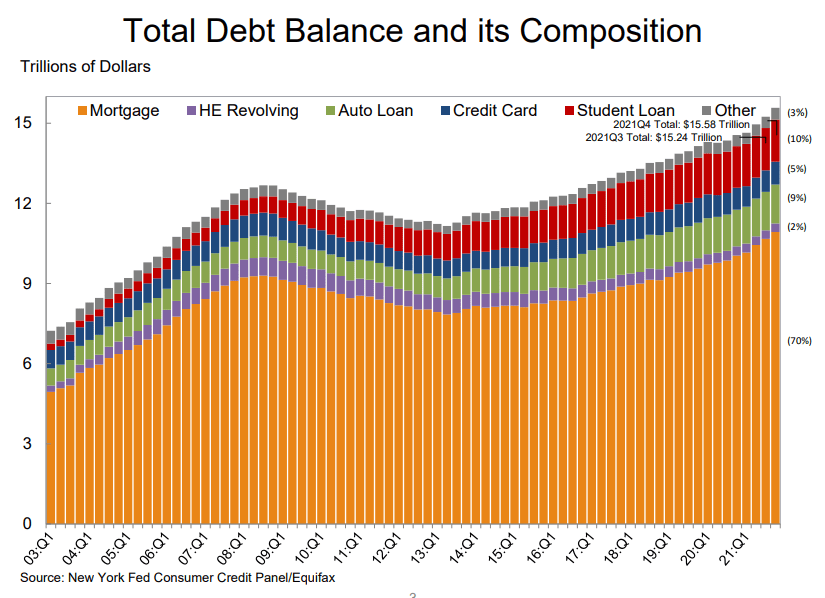

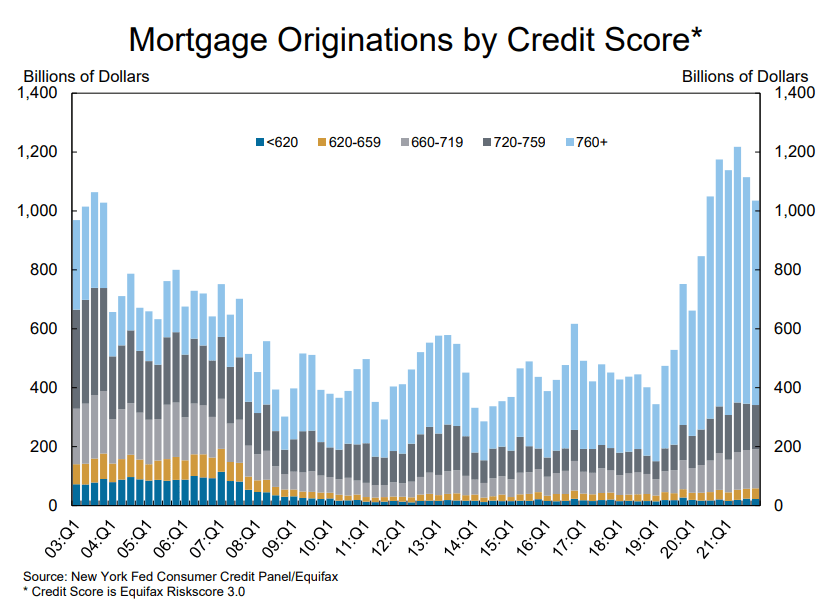

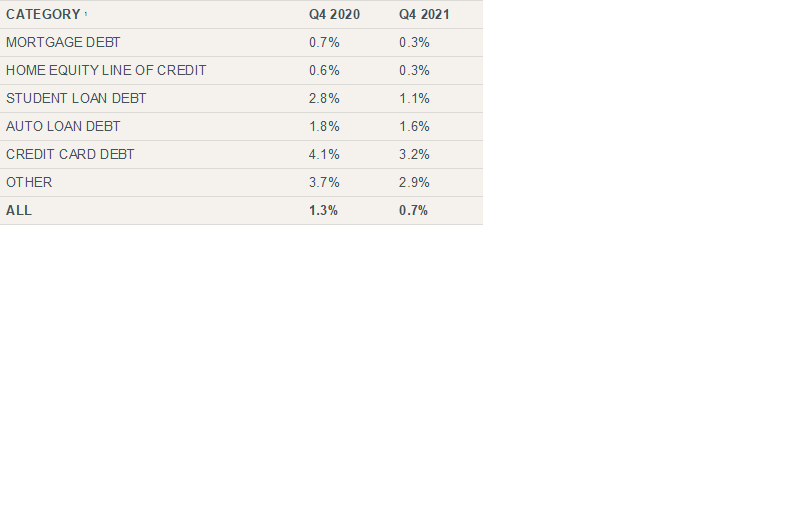

Household Debt and Credit Developments as on Q4 2021

The Total Mortgage debt is $10.93 Trillion at present.

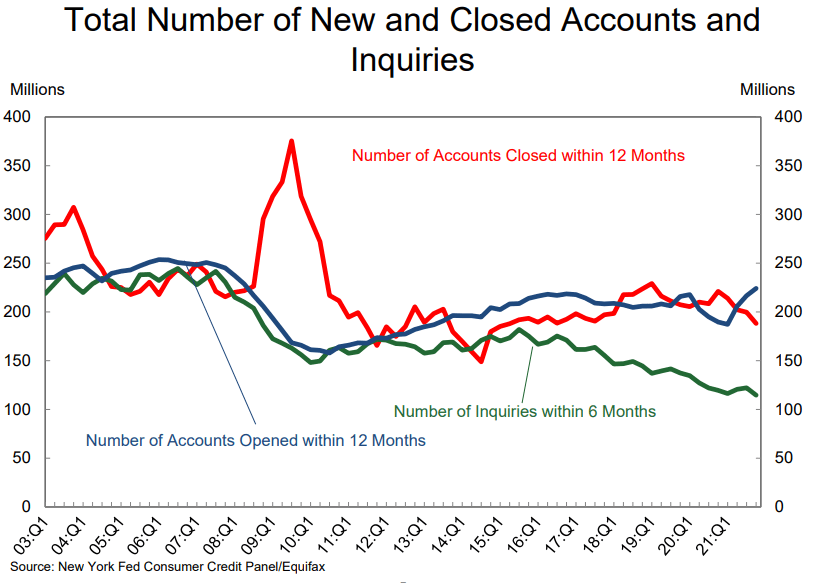

Flow into Serious Delinquency (90 days or more delinquent)

Source: New York Fed Consumer Credit Panel/Equifax

– By Nishant Maheshwari & Vishal Vora

Disclosure: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting their financial advisors.

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Account Holder Name: Rashi Maheshwari IFSC:SBIN0030115

I love reading this post. Looking forward to more ideas.

LikeLike