Previously, Dividend Distribution Tax (DDT) was payable by the Domestic Company on declaration, distribution or payment of dividend. However, Finance Bill 2020, proposed to abolish Dividend Distribution Tax, and has shifted the burden of taxability to the recipient of dividend Income i.e. the shareholder or Unit holder (in case Mutual Fund).

Erstwhile Provision of the Act

Section 115-O provides that, in addition to the income-tax chargeable in respect of the total income of a domestic company, any amount declared, distributed or paid by way of dividends shall be charged to additional income-tax at the rate of 15 per cent. The tax so paid by the company (called DDT) is treated as the final payment of tax in respect of the amount declared, distributed or paid by way of dividend. Such dividend referred to in section 115-O is exempt in the hands of shareholders under section 10(34). In case of business trust, specific exemption is provided under sub-section (7) of section 115-O, subject to certain conditions. Similarly, exemption is provided for distributed profits of a unit of an International Financial Service Centre, on fulfillment of certain conditions, under sub-section (8) of section 115-O. Similarly, under section 115R, specified companies and Mutual Funds are liable to pay additional income-tax at the specified rate on any amount of income distributed by them to its unit holders. Such income is then exempt in the hands of unit holders under clause (35) of section 10.

Provision after Amendment in the Finance Bill

Budget has proposed to remove Dividend Distribution Tax the hands of Company. Therefore, dividend or income from units are taxable in the hands of shareholders or unit holders at the applicable rate and the domestic company or specified company or mutual funds are not required to pay any DDT.

Further Section 57 is also amended to provide that no deduction shall be allowed from dividend income, or income in respect of units of mutual fund or specified company, other than deduction on account of interest expense and in any previous year such deduction shall not exceed 20%. of the dividend income or income from units included in the total income for that year without deduction under section 57.

Rationale for Change in Budget

As per the Budget Memo, “The dividend is income in the hands of the shareholders and not in the hands of the company. The incidence of the tax should therefore, be on the recipient. Moreover, the present provisions levy tax at a flat rate on the distributed profits, across the board irrespective of the marginal rate at which the recipient is otherwise taxed. The provisions are hence, considered, iniquitous and regressive. The present system of taxation of dividend in the hands of company/ mutual funds was reintroduced by the Finance Act, 2003 (with effect from the assessment year 2004-05) since it was easier to collect tax at a single point and the new system was leading to increase in compliance burden. However, with the advent of technology and easy tracking system available, the justification for current system of taxation of dividend has outlived itself.”

Impact of Change and Outflow of Tax

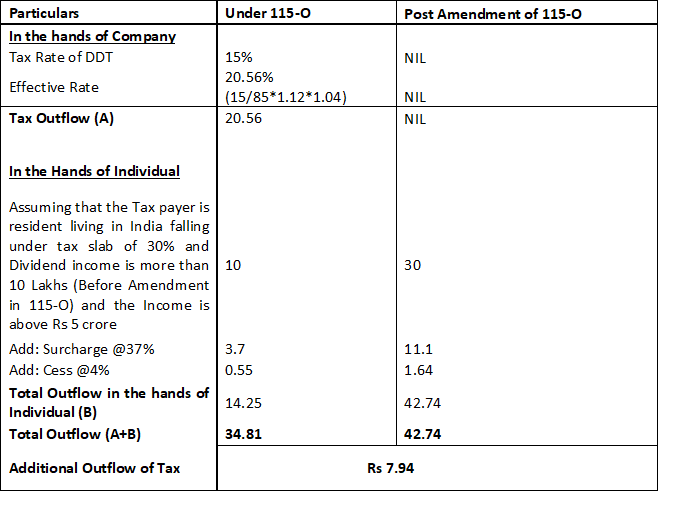

In order to explain the impact of Change let us take an example wherein the company intends declare and distribute Rs 100 per share as Dividend. The following tabular presentation will reflect the impact before the amendment and impact after the amendment:

It can be seen from the above table that in the erstwhile provision i.e. before removal of Dividend Distribution Tax Rs 20.56 is payable by the company and Rs 14.25 is payable by the resident Individual. Thus, the total outflow is Rs 34.81.

However, after the amendment in Finance Bill 2020 i.e. after removal of Dividend Distribution Tax, no tax outflow is in the hands of Company while declaring the dividend but Rs 42.74 is payable by the resident individual.

Thus Rs 7.94 is the additional outflow.

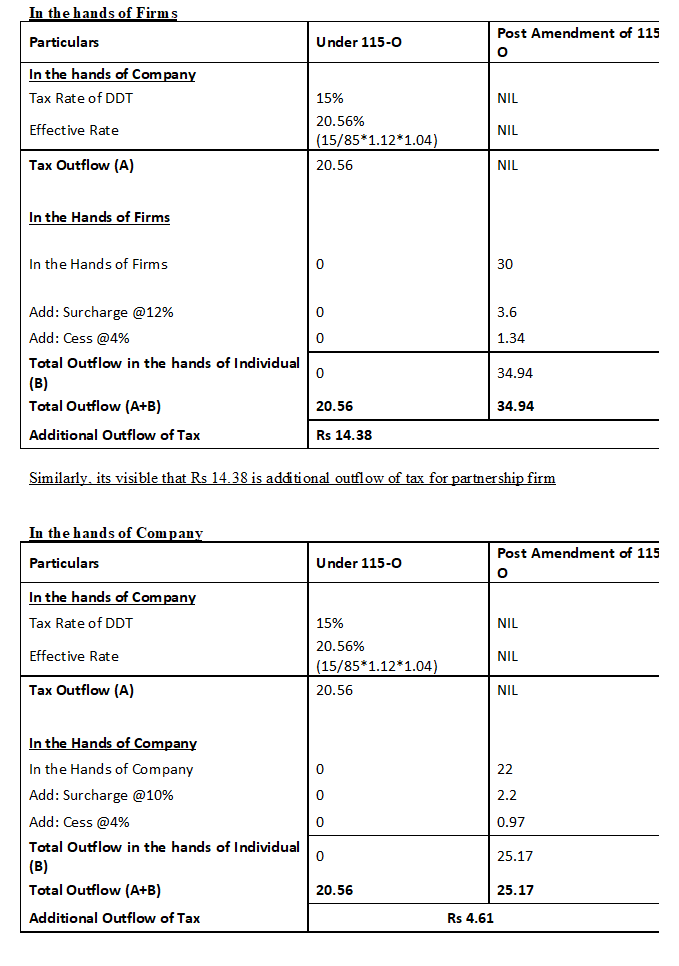

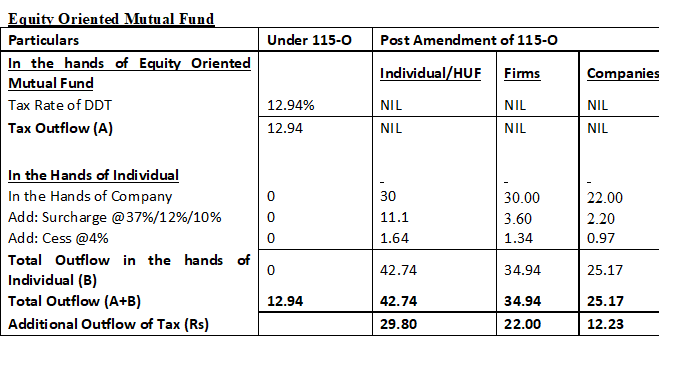

Similarly, its visible that Rs 4.61 is additional outflow of tax for Company. Further, the summarized Tax rate of Pre-Amendment and Post Amendment of Dividend distributed by Equity Oriented Mutual Fund are as under:

It is visible that the additional outflow in case of Individual/HUF is Rs 29.80 post amendment, Rs 22 in case of firms and Rs 12.23 in case of Companies.

Effect on Foreign Companies and Non-Resident

Dividends will now be taxed in the hands of non-residents, including foreign companies, at the rate of 20 per cent (plus surcharge and cess) under section 115 A. The T.D.S or withholding tax is governed by Section 195, for which rates are specified each year in Part II of the first schedule of the Finance Act as “rates in force”.

Such rate would be further reduced where the tax treaty provides for a beneficial rate, the rate of tax on dividend under most tax treaties is 15 per cent (e.g., Luxembourg, Netherlands, Singapore, and the UK), but may be as high as 15% (US), or as low as 5% (Mauritius).

Unintended Consequences after the removal of DDT

An unintended consequence of the new regime may result in Indian promoters evaluating whether to shift base from India to take benefit of the concessional rate of tax applicable to non-resident individuals. Further, this dichotomy in the rates of tax may lead to companies opting for other options for cash repatriation such as buyback which is still taxed at 20 per cent (plus surcharge and cess).

E.g.: If resident promoter is receiving dividend in India of Rs 100 and comes under slab of 30% and above then the tax outflow is Rs 42.74. Suppose Indian promoter shift the base from India to US the tax outflow will be Rs 20 (plus Surcharge and Cess) deducted u/s 195 and later the tax credit will be claimed in the country of residence.

Proposed Amendments in budget related to T.D.S after abolishment of Dividend Distribution Tax:

- Amended Section 194 to include dividend for tax deduction. At the same time the rates of 10% is proposed to be prescribed and threshold is proposed to be increased from Rs 2,500/- to Rs 5,000/- for dividend paid other than cash. Further, at present the mode of payment is given as “an account payee cheque or warrant”. It is proposed to change this to any mode. Amendments will be effective from 1st April, 2020.

- Amended section 194 LBA to provide for tax deduction by business trust on dividend income paid to unit holder, at the rate of 10% for resident. For non-resident, it would be 5% for interest and 10% for dividend. Amendment will be effective from 1st April, 2021 and will, accordingly, apply in relation to the assessment year 2021-22 and subsequent assessment years.

- New section 194K is being inserted to provide that any person responsible for paying to a resident any income i.e. Dividend in respect of units of a Mutual Fund specified under clause (23D) of section 10 or units from the administrator of the specified undertaking or units from the specified company shall at the time of credit of such income to the account of the payee or at the time of payment thereof by any mode, whichever is earlier, deduct income-tax there on at the rate of 10%. It may also be provided for threshold limit of Rs 5,000/- so that income below this amount does not suffer tax deduction. Amendment will be effective from 1st April, 2021 and will, accordingly, apply in relation to the assessment year 2021-22 and subsequent assessment years.

- Amend section 195 to delete exemption provided to dividend referred to in section 115-O since Dividend Distribution Tax has been removed. Amendments will be effective from 1st April, 2020. Amendments will be effective from 1st April, 2020.

- 196C is also amended wherein dividend under section 115-O is removed. Further “in cash or by the issue of a cheque or draft or by any other mode” is being substituted “by any mode”.

- 196D is also amended wherein dividend under section 115-O is removed. Further “in cash or by the issue of a cheque or draft or by any other mode” is being substituted “by any mode”. Amendments will be effective from 1st April, 2020.

Effect on Section 10 related Exemption relating to Dividend Exemption

- Section 10(34) shall not apply to any income, by way of dividend, received on or after 1st April, 2020.

- Section 10(35) shall not apply to any income, in respect of units, received on or after 1st April, 2020.

- The distributed income of the nature as referred to in clause (23FC) or clause (23FCA) of section 10 shall be deemed to be income of unit holder and shall be charged to tax as income of the previous year.

- Amend clause (23FD) of section 10 to exclude dividend income received by a unit holder from business trust from the exemption so that the dividend income is taxable in the hand of unit holder of the business trust.

- Section 10(23D) will be amended wherein mutual fund will be no longer required to pay additional tax.

The above amendments will be effective from 1st April, 2021 and will, accordingly, apply in relation to the assessment year 2021-2022 and subsequent assessment years.”

Impact on Section 115JB (MAT)

For the purpose of calculating Book profit under Section 115JB of Income Tax Act,1961 dividend income received by the domestic company would be considered for computing the book profit.

Impact on Section 14A of the Act to be read with Rule 8D

The removal of Dividend Distribution Tax as proposed in the Finance Bill 2020 would finally bring end to the expenditure in relation to exempt (dividend) income disallowed u/s 14A to be read with Rule 8D of the Act on the fact that the dividend income is now taxable in the hands of the investors.

Conclusion

Post abolishment of Dividend Distribution Tax, government will lose 25000 crore of revenue in the form of DDT. However, the probable collection of tax will be more from big HNIs, promoters of listed companies, etc. Though the provision is regressive in nature for high net worth individuals but at the same time it is fruitful for Foreign Investors and individuals having income below Rs 10 Lakh.

- By Vishal Vora,Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the author and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.

Gteat Article, Nishant and Vishal

– Nishant Batra

LikeLike

Thanks for the appreciation

LikeLike