In our previous blogs, we have written in detail about China’s real estate mess where we have described that how the crackdown on real estate sector can trigger contagion effect in the economy, its impact and then we further emphasised on Collateral Loan Obligation implosion. But somehow all those blogs are not complete if we don’t emphasise on How this Contagion disease is born in China or how it helped to nurture this credit bubble? In this blog we will concentrate only on Local Government Financing Vehicle (LGFV). Though the data of China is difficult to extract but we will try to give overview about the size of this market.

Local Government Financing Vehicle of China

Background

LGFVs have special roles in supporting regional economic development but also constitute a major portion of local government liabilities. Local government funding vehicles (LGFVs) are a sub-group of SOEs in China, typically founded for financing infrastructure and other regional development projects and usually do not operate for profits. Since the 2000s, the LGFV debt market has grown at an even faster pace given the policy support on boosting regional economies by investing extensively in infrastructure and social welfare projects.

But mounting debt and high leverage carried by LGFVs have led to concerns of overleveraging which has typically been off-balance sheet so far. While onshore bank and bond markets have been traditional sources of funding, in recent years, a large number of LGFVs have tapped the offshore bond market as well. As the LGFVs usually operate social welfare or infrastructure projects which do not generate constant and immediate cash flows, government support for their operations becomes even more critical.

AS per Goldman Sachs report, it is believed that the size of LGFV rose from 16 Trillion Yuan or $2.5 Trillion in 2013 to 53 Trillion Yuan or $8.2 Trillion in 2020. The size of loan is equivalent to 52% of GDP of China.

Model of working with simplified example

Let us take an example how this model works. Suppose local government in Jiangsu region is having surplus land bank and wants to strengthen the financial position of that area. But the local government cannot borrow the same directly. Now what do they do? They incorporate a company which is also known as Local Government Financing vehicle, gives it surplus land to that company and raise debt from investors in the form of Debentures or Bonds or Municipal bond or Chengtou Bonds and securitise that land in favour of Investors. The duration of Bond can be categorised as short-term duration bond (Medium term notes, promissory notes or commercial paper) or long-term duration bonds (Corporate Bonds, Enterprise Bonds or private placement bonds) fully backed by local government.

Initially ratings for these Bonds were not an issue as the guarantee is given by local government along with securitisation of Land but post 2014 it is done with stringent regulation in force. Although the amount raised against that land is 70% of the value of Land. Now the amount raised from that Bonds is used to finance Infrastructure projects or Real estate developers.

Policy changes for LGFV in China

Since the budget law revision in 2014, the government has taken further steps to tighten policies on local government funding and LGFVs’ borrowing activities. Government authorities released Article No. 43 in 2014 and Article No. 4 in 2016 to separate the financing function of LGFVs from local governments and to prevent LGFVs from using land pledges to obtain financing. Higher-tier local governments were only allowed to issue bonds directly but not through LGFVs or enterprises. The authorities also introduced the bond swap program to refinance legacy LGFV debts – basically it is a practice to swap LGFV debts into lower-yielding munis so that interest on these products can be effectively reduced. The government thereafter introduced several more regulatory measures, including: 1) Document No. 50 (May-2017), which reinforces the policy goal of Article No. 43 to prohibit local government off-budget borrowing, 2) Document No. 87 (June2017), which prohibits illegal financing behavior in purchasing certain services of LGFVs by local governments. In April 2018, the Ministry of Finance (MoF) released Notice 23 to regulate state-owned bank lending activities, particularly to LGFVs.

Size of LGFV in 2020 and status

At end-2020, local government outstanding debt reached RMB25.49 trillion ($3.95 Trillion). There were 9 provincial governments with outstanding debt over RMB1 trillion. Most of the provinces recorded increase in debt ratio (total debt over budgetary fiscal income and over GDP) in 2020, given the increase of debt from the counter-cyclical measures, together with the decline in GDP and fiscal income amid the COVID-19.

Provinces in eastern China with well-developed economies generally recorded higher broad based outstanding debt (sum of local government’s outstanding debt and LGFVs’ interest earing debt), due to the larger number of LGFVs and the higher amount of LGFVs’ debt in these provinces.

Eg: Jiangsu province’s broad-based debt exceeded RMB 8 trillion at end-2020, followed by Zhejiang, Shandong and Guangdong provinces. LGFVs’ debt accounted for 50-70% of the total broad-based debt in these provinces. However, given the support from strong local economic performance and local governments’ fiscal conditions, these local governments enjoyed wider access of funding channels and lower financing costs. On the contrary, less-developed provinces in north western, north eastern and southwestern China faced higher repayment burden. These local governments had higher debt balance compared with their fiscal income. For example, Qinghai province and Inner Mongolia autonomous region recorded high debt ratio at end-2020, due to their slow GDP growth of 1.5% and 0.2%, respectively. Guizhou and Gansu provinces also recorded high debt ratio at end-2020. Therefore, they had limited room for issuing new debt and their fiscal conditions remained tight. 28 out of 31 provinces recorded slower growth rates of broad-based outstanding debt than that of local government debt in 2020. It shows that some of the LGFVs debt is gradually being replaced by local governments debt, and the proportion of local governments debt to the broad-based outstanding debt is becoming more explicit. Local governments are required to control their debt growth and strengthen their debt servicing capacity, whereby their budgetary fiscal income should be adequate to support or even exceed the principal and interest payments burden during the same period.

Review of Half year LGFV’s in 1H2021

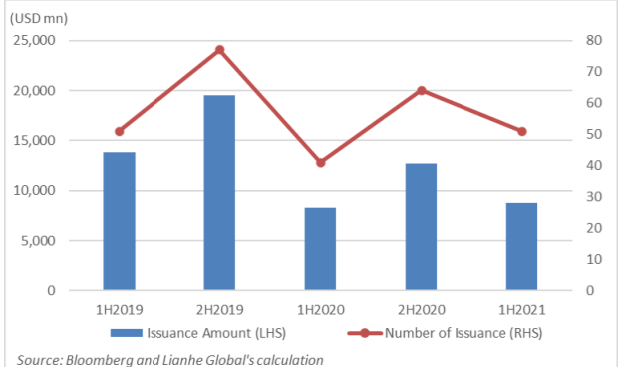

LGFVs went through a rough patch in 1H2021 with subdued issuance as a result of the spill over effect of the changing investor sentiments from a spate of SOE defaults. With the rebound of the Chinese economic growth, the need for refinancing and relatively more favourable financing cost offshore, the issuance amount of China LGFVs’ offshore USD bond reached USD8.7 billion in 1H2021.

Here is the chart of Offshore LGFV USD Bond Issuance and number of Issuance

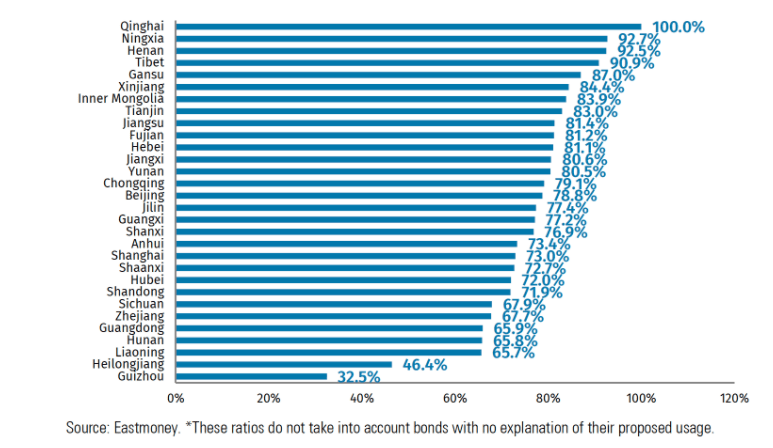

Ratio of LGFV Bond proceeds used for repayment, by province, Jan 2018-April 2019

The refinancing portion has further increased at rampant pace with widespread default in 2020-21 due to failure of various private entities along with State owned entities.

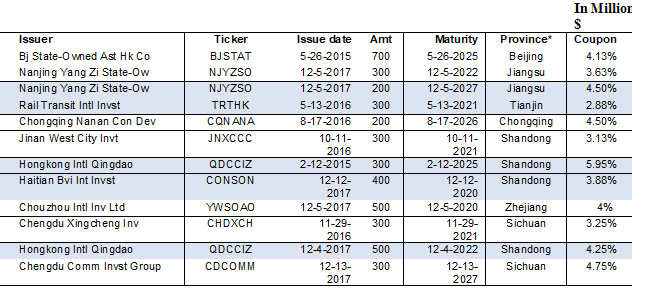

List of few LGFV Dollar denominated Bonds

While this amount represented a year-on-year increase of 5.7% compared with the trough in 1H2020, it was still lower than 2H2020 and 1H2019 by 31.3% and 36.7%, respectively. Under the regulatory requirements, issuance was mainly used for refinancing LGFVs’ offshore debt instead of new financings.

The Chinese government has urged local governments to strengthen their debt managements, such as strictly controlling and resolving the risk of implicit debt, improving the efficiency of the use of fund from financing, and reinforcing the management of specialty debt, etc. Moreover, LGFVs are prohibited from raising new debt and repaying the implicit debt for local governments. According to the Ministry of Finance, total new bond issuances by local governments showed a year-on-year decrease of 20.4% to RMB2,546.3 billion for 5M2021, compared with RMB3,199.7 billion for 5M2020.

Status of Onshore LGFV

Spreads for LGFV debt rose in 4Q20 following the high-profile default of Yongcheng Coal & Electricity Holding Group and other state-owned enterprises (SOEs).

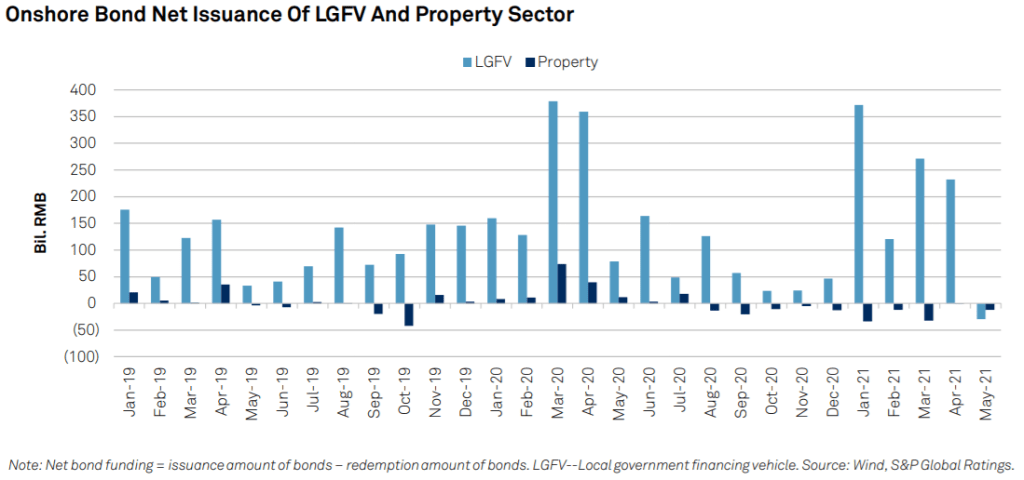

Onshore LGFV bond issuance fell significantly in response to the defaults. Issuance in 4Q20 totalled CNY859 billion, 22% lower than 3Q20 volumes. Net financing fell to CNY45 billion from CNY300 billion in 3Q20. LGFVs have taken on record levels of debt in 2020, including through the issuance of “anti-epidemic bonds” for public welfare duties.

Here is the chart of Onshore LGFV issuance:

LGFVs to see tighter funding conditions and refinancing pressures in 2021 as the central bank pursues long-term reforms in the local government debt market.

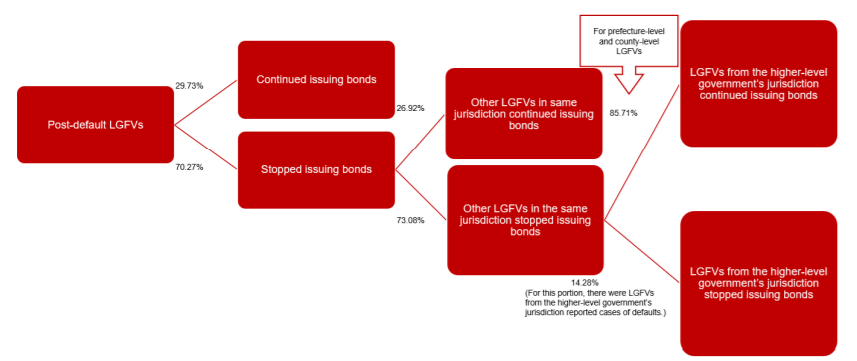

Situation of Defaults in LGFV

China’s local government financing vehicles (LGFVs) have reported more cases of non-standard product defaults since 2018 after the government strengthened the regulatory efforts and oversight over the sector’s financing. According to the statistics, China has seen 90 non-standard product defaults by LGFVs involving 117 entities (including both issuers and guarantors) from January 2018 to November 2020. A large number of default cases happened in provinces including Guizhou, Yunnan, Inner Mongolia and Sichuan, with higher proportion of defaults by county-level LGFVs and LGFVs with no bond issuance record. In addition, it is worth noting that when a prefecture-level LGFV reports defaults, it is typical that the lower-level LGFVs under its jurisdiction may have already reported defaults several times.

The short-term debt as a percentage of total debt of LGFVs that have reported non-standard product defaults rose rapidly, from 13.58% at the end of 2016 to 24.34% at the end of 2019, while the cash to short-term debt ratio decreased from 5.73 in 2016 to 0.31 in 2019.

A presentation of flow chart will describe the post default scenario in LGFV

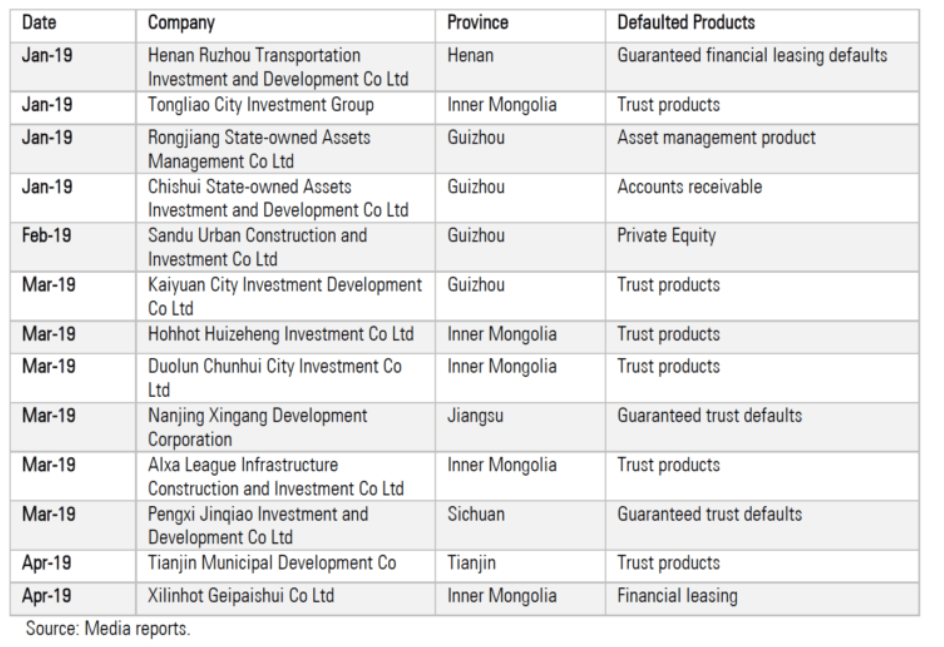

List of Reported Defaults

The list has further increased with bad situation of cash flows in many provinces but we are here reporting the public domain list.

Conclusion

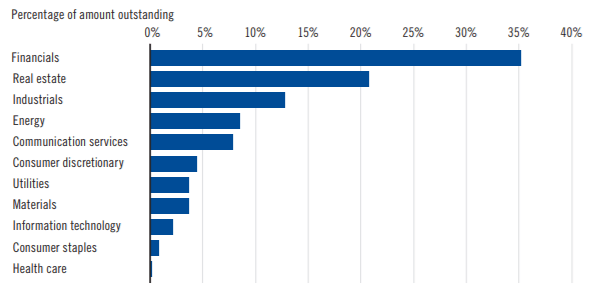

While land in China played a crucial role for these LGFVs as the skyrocketing prices of land was being used as collateral portion to finance the needs of the states. But with the recent crackdown on real estate and the contagion effect on Bond market, the trouble in real estate in China has spread the malignant disease in LGFVs segment. The deleveraging effort of CCP will continue with greater force and the termites in Shadow Banking will slowly be killed. The shadow Banking of China in the form of LGSV is nothing new. Even though the defaults have occurred in the past but they were never exposed. But at present the crackdown created by CCP has created a severe impact on the financial system of China. The interesting point to note is that people claim that the China’s debt problem is mainly in local currency but most of them are missing one fact the finance is provided by the central banks which consists of large amount of offshore bonds liability denominated in USD, Euro and Yen. China offshore bond sector exposure (US$) as on 04.06.2021

Land has always played crucial role in China to sustain GDP portion since a long time. The targets set by CCP to Local states were met through these Land transaction. Those exorbitant deals of land added substantial portion in revenue due to large size real estate transactions.

Annual revenues from land usage right transfers in US$ December 1, 2009–December 1, 2020

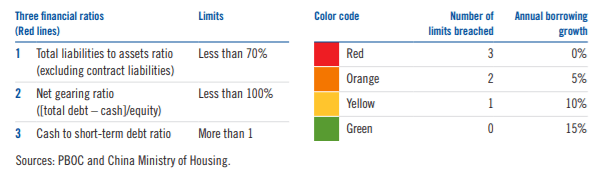

But now with three red lines in force i.e. Liabilities to assets ratio (Excluding contract liabilities) less than 70%, Debt to equity less than 100% and cash to short term debt ratio less than 1 will create a systematic risk for existing real estate developers and create substantial reduction in real estate activities as more than 90% developers will fall in these ratio as they have breached one of the three conditions. Three financial ratio limits and annual borrowing growth caps

With now imminent crash in real estate activities, the prices of land will substantially get reduced. This will create contagion effect in LGFVs as the value of land used as collateral at exorbitant value will all of a sudden fall down, the yields will spike in these bonds and will disable them to reissue bonds while they will be trapped with upcoming maturities. The fall in value of land will further deteriorate the books of of central banks and expose those hidden debt or shadow banking system. This will result in spike of offshore bond yields of these banks.

CREATION OF ANY LEVERAGE IN SYSTEM IS VERY EASY JOB BUT WHEN IT COMES TO DELEVERAGING THE TREMOR EFFECT ON CURRENCY, INDUSTRY AND SERVICE SECTORS WILL ALWAYS CREATE AFTER EFFECTS. IT ONLY DEPENDS ON THE INTENSITY OR THE MAGINITUDE AT WHICH THE SHOCKS ARE PROVIDED.

- By Nishant Maheshwari, Vishal Vora

Disclosure: This article is for information only and should not be construed as a financial advice.

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Name: Rashi Maheshwari<br>IFSC Code: SBIN0030115

Name of Bank: SBI India,YN Road Branch Indore-India

One thought on “Local Government Financing Vehicle (LGFV) – How it helped fuel the Chinese housing bubble”