Before starting with our Blog, lets analyse one important section from Federal Reserve Act,1913. Its Section 13(3) which states:

“In unusual and exigent circumstances, the Board of Governors of the Federal Reserve System, by the affirmative vote of not less than five members, may authorize any Federal reserve bank, during such periods as the said board may determine, at rates established in accordance with the provisions of section 14, subdivision (d), of this Act, to discount for any participant in any program or facility with broad-based eligibility, notes, drafts, and bills of exchange when such notes, drafts, and bills of exchange are indorsed or otherwise secured to the satisfaction of the Federal Reserve bank:

Provided, that before discounting any such note, draft, or bill of exchange, the Federal reserve bank shall obtain evidence that such participant in any program or facility with broad-based eligibility is unable to secure adequate credit accommodations from other banking institutions. All such discounts for any participant in any program or facility with broad-based eligibility shall be subject to such limitations, restrictions, and regulations as the Board of Governors of the Federal Reserve System may prescribe.”

And what Section 14 of Federal Reserve Act,1913 is related with Open Market Operations

During the course of March 2020 which is practical example of invoking section 13(3) of Federal Reserve Act,2013 when the economy saw a huge Turbulence on account of Corona Virus. The Fed used the provisions of Section 14 on account of invocation of Section 13(3) and came up with following actions:

- FOMC expanded standing U.S. dollar liquidity swap arrangements to enhance the provision of U.S. dollar liquidity to foreign markets as well as established temporary swap U.S. dollar liquidity lines to allow central banks to borrow U.S. currency against collateral in their respective jurisdictions. The temporary swap lines expired on December 31, 2021.

- On March 17, 2020, the Primary Dealer Credit Facility (PDCF) was established as a term loan facility that provides funding to primary dealers in exchange for a broad range of collateral and was intended to foster the functioning of financial markets more generally. The PDCF’s authority to extend loans ended March 31, 2021. All loans were subsequently repaid.

- On March 17, 2020, the Commercial Paper Funding Facility (CPFF) was established to provide liquidity to short-term funding markets. The CPFF’s authority to purchase commercial paper ended March 31, 2021, and CPFF II was terminated on July 8, 2021.

- On March 22, 2020, the Term Asset-Backed Securities Loan Facility (TALF) was established to provide loans to U.S. companies secured by certain AAA-rated asset-backed securities (ABS) backed by consumer and business loans. . The Treasury, using funds appropriated to the ESF through the Coronavirus Aid, Relief, and Economic Security (CARES) Act, made an equity investment in TALF II. The TALF’s authority to extend loans ended December 31, 2020.

- On March 23, 2020, the Corporate Credit Facilities was established to administer the Primary Market Corporate Credit Facility (PMCCF), which was established to support credit to employers through bond and loan issuances, and the Secondary Market Corporate Credit Facility (SMCCF), which was established to support credit to employers by providing liquidity for outstanding corporate bonds. CCF was terminated on December 17, 2021.

- On April 8, 2020, the Municipal Liquidity Facility was established to support lending to state, city, and county governments, certain multistate entities, and other issuers of municipal securities. The facility’s authority to purchase eligible assets ended December 31, 2020.

- On March 18, 2020, the Money Market Mutual Fund Liquidity Facility (MMLF) was established to provide funding to U.S. depository institutions and bank holding companies to finance their purchases of certain types of assets from money market mutual funds under certain conditions. The MMLF’s authority to extend loans ended March 31, 2021. All loans were subsequently repaid.

- On April 9, 2020, the Main Street Lending Program (MSLP) was established to support lending to small and medium-sized businesses and non-profit organizations that were in sound financial condition before the onset of the coronavirus pandemic.

- The facilities’ authority to purchase loan participations ended January 8, 2021.

Well the above facilities resulted in expansion of Balance sheet of Fed by 1.55 Trillion dollars since 31.12.2020 till 25th May 2022. The abstract of whole Assets side is as under:

Figures are in Million Dollars

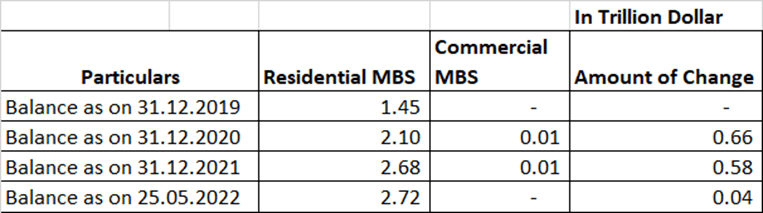

In order to normalise the economy, the US Federal Reserve aggressively bet on Mortgage Backed Securities:

It is interesting to see that 620 Billion dollars of Mortgage Backed securities have been purchased by Fed since 31.12.2020 till date. And the constant support of lower interest rates created mismatch in asset liability side. When Fed is present, people start aggressive investing in Housing market as mortgages are available at lower interest rates and under FHA scheme the upfront payment required was 3.5% instead of 20%. Further moratorium also played a great role in order to safeguard Banks assets as non-performing. The rotation of money became rampant. And the thing became normalised with mathematical numbers of GDP or Job report or Housing market or Manufacturing activity.

But like any devil, the result of this easy money was inflation not because of demand side but it was on account of supply chain issues.

As on 31.05.2022, situations have completely changed. All the liquidity support by Fed has been snatched away erasing all the easy money flows in the system. While we saw some interest rate hike from Fed to the extent of 0.75% since Jan 2022 till date but inflation has been trending up. In order to further curb the problem of Inflation, Fed proposed Quantitative Tightening of Balance sheet size as per following manner:

| TOTAL MONTHLY CAPS ON SOMA SECURITIES REDUCTIONS | ||

| Treasury Securities | Agency Debt and Agency MBS | |

| Jun-Aug 2022 | $30 billion | $17.5 billion |

| From Sep 2022* | $60 billion | $35 billion |

*Once caps reach these amounts, they are expected to remain in effect until otherwise directed by the FOMC.

However, the present circumstances are pointing towards softening of the Housing market where Mortgage Rates started spiking before than Quantitative Tightening and Inflation causing some unusual spikes in Bond yields.

Conclusion

As the National Debt size of US is more than 30.48 trillion dollar with the GDP of US at 23.59 Trillion dollar, 0.75% increase in Interest rate can cause additional outflow of 229 Billion dollars from system which is equivalent to 1/3rd amount of Purchase of mortgage backed securities by Fed in last 2 years.Further, additional outflow of 142.50 Billion dollars from system from June 2022 to Aug 2022 will result in further shrinkage of liquidity from the system. The bazooka of liquidity in the system provided by Fed is now acting like a drug addiction and taking away this liquidity will be like Fish in Pond without water. However, the interesting factor to watch out here is applicability of Clause 13(3) as discussed above. In order to provide more QE and bail out of liquidity to the system Fed needs unusual and exigent circumstances. With QT starting and geopolitics at elevated levels, a small fire would be enough to cause the damage to an individuals net worth.

From CA Nishant Maheshwari and Vishal Vora

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Account Holder Name:Rashi Maheshwari

One thought on “ Section 13(3) of Federal Reserve Act,1913-What does that mean for Economic revival?”