We live in interesting times. On one hand, we are living in one of the most prosperous ages the earth has ever seen. The technological advancement is unparalleled in human history. Global wars have not been seen since last 75 years baring a few small localised wars. The global population is 7 billion plus strong and yet there is enough to satisfy the needs of most of the people. Internet has made flow of ideas easy and communication has made the world smaller and more connected. Yet on the other hand, forces are converging and seem to indicate that the relative peace is merely a sign you see before periods of turmoil. The factors of global debt, the deflationary forces, the demography issues are merely combining and indicating a significant wave of defaults that may look impossible today but may happen over a period of time in the next few years.

Let’s look at each of these factors in isolation and how their combination can create a tumultuous period in human history.

Debt

As per International Institute of Finance, Global Debt rose 10 trillion dollars in 2019 topping 255 trillion dollars. This was 40% higher than the 2008 financial crisis. In 2020, we have the Covid pandemic causing heavy damage to the economy. Most countries have opened their financial war chests and trying to stem the global deflation through stimulus for households, small businesses and various industries. The total stimulus till date is in excess of 10 trillion dollars. Given that trade has been suffering for most of the year and local economies struggling to get back to pre covid levels, we expect majority of the stimulus to be debt funded and will further add to debt to GDP ratio which was already at a high of 322% (Source: IIF, April 2020). As global GDP is expected to decline by 3% and debt expected to increase by tens of trillions of dollars, one can be certain that the global debt to GDP will soon be touching 400%. The USA which is the largest country in GDP terms already faces trillion-dollar budget deficit has announced 6 trillion dollars of stimulus and is expected to announce further stimulus to get the economy on track.

The impact of the growth in debt and in Debt to GDP ratio will eventually lead to slow growth. As seen in most of the developed world, interest rates are below 1% while those in Japan and Eurozone are in the negative. The debt to GDP ratio of the developed world will further accentuate increasing the pressure to keep interest rates low. This also means further lower yields on bonds of developed countries. The impact on poor countries will be even more dire. Without global growth, servicing this mountain of debt is nearly impossible. One may even ask as to why investors/countries continue to buy bonds of sovereign if they are not supposed to yield anything and become increasingly risky.

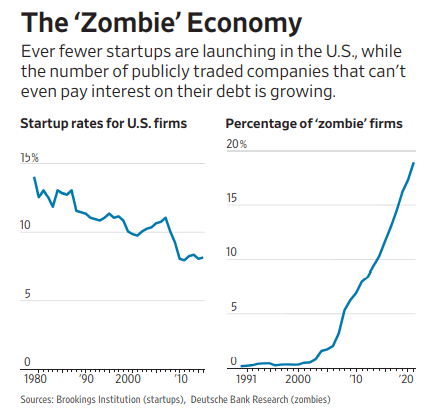

The problem with increasing debt burden is that every additional unit of debt is leading to decelerating increase in GDP growth which means at some point in future there will come a time when further debt will not only lead to stagnation or decline in GDP but will increase further debt burden and increased liability. Such scenario indicates an event where interest liability will be met by raising further debt. This is quite similar to marginal utility as more and more units of debt get poured in, they end up in places where the real benefits will be far lesser and the burden on the consumer gets further added up. Hence, we find that the number of zombie corporations has been increasing and is now touching 15-20% in some regions. This means more dead wood for the next fire as they line up for defaults.

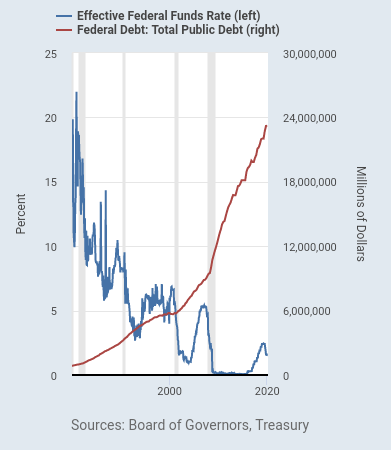

Source: US Fred

As can be seen from the above chart, the debt bubble started in 1980 when the interest rates peaked in 1981. Since then, interest rates have remained in a falling environment. This falling interest rates has enabled a risk on environment seen in the stock markets and economic activity was increasingly supported by additional debt. From 1980 to 2000, Total debt increased by 5 trillion dollars as interest rates fell from 21% to 5%. In the next decade, interest rates fell to 0 while debt went up to 12 trillion dollars. In the last decade, the debt has increased to 26 trillion dollars and expected to touch 30 trillion dollars. Not to mention there is a trillion-dollar deficit each year. At this rate, it is impossible for the FED to normalize interest rates. Hence rates will have to be kept low for long period of time. However, if interest rates were to rise, it would become impossible to make interest payments with existing revenue.

While the situation is similar in most countries as most countries have expanded their debt to GDP ratio using monetary policy tools, the monetary policy has run its course. Fiscal policy tools are now been used for creating growth. However, spending is increased in the same way with the only exception been that demand is pulled forward for some more time. This process has been repeated multiple times in 2008, 2016, 2020. There is no other policy tool left with government now playing this increasingly dangerous game of borrowing from the future. The above decisions have led to a decade long bubble in bonds and stocks and is only dependent on further stimulus and interest rate cuts. However, the room for further stimulus is decreasing day by day but the world seems to believe that central banks will not let asset prices drop much. There is now absolute confidence that the FED and other central banks will bail out investors. To that effect, they are already engaged in saving the bond holders. Equity may be the last resort.

Source:- TradingEconomics.com,

As can be seen, there is not much room left for interest rates or debt to go further down this lane of financialized markets. As the economic cake becomes smaller, each country will try to defend its share of the pie. Hence, we see trade tariffs and deglobalization becoming increasingly prevalent. There are now hotspots where conflicts are increasingly likely. Economies are trying to decouple from China which has become global manufacturing giant having worlds 28% market share in manufacturing. The force of debt is leading to low to negative economic growth absent any life changing innovation or technological breakthrough increasing productivity considerably.

Deflation

The corona virus pandemic has suddenly created demand for a lot of necessities as supply chains got disrupted. This has led to rising food prices. The rising prices coupled with central bank flooding the markets with stimulus is creating an environment of rising inflation. However, falling money velocity indicates no such thing. In fact, the real danger is deflation. The demand for housing and automobiles is down in most parts. Rents are falling even in best cities as people feel cities are not the best place to live anymore owing to protests and pandemic spread and lack of employment opportunities. Given the impact on wealth and the losses of jobs that has taken place, there is real threat that consumers will cut down on discretionary spend. This is already visible in automobiles where demand for used cars and bicycles is increasing but new vehicles sales are down even after reopening.

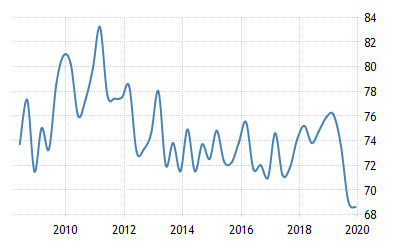

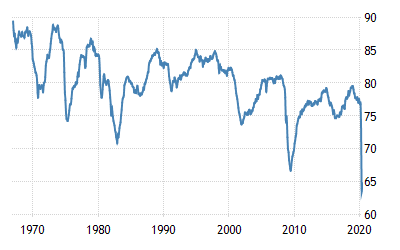

The reasons for deflation are many. But the most important signal lies in corporates interested in their buyback of shares rather than investing the same in capacity building. The real utilization rates in most countries is nowhere near their recent highs(Capacity utilization is below 70 in India and USA. It was near 77 in February Covid has played a major role but on average basis it is still lower than average for past 40 years

Source: Tradingeconomics.com

The reasons for such low capacity utilization are multiple.

- Prices have been increasing especially rents, housing, autos, food, etc

- Purchasing power has been weakening.

- Incomes have been growing at a slow rate

- Increased debt spending on social welfare reducing government ability to spend on infrastructure and other growth initiatives

Given that purchasing power has stagnated for decades and prices of essential goods and services increasing, it is causing the consumer to go into further debt to meet their needs. With moderate productivity growth and technological innovation, robotics and automation, the demand for labour is stagnating. Therefore, the number of available jobs is reducing while employees are forced to give up retirement as their pension might not be enough to meet their needs at today’s.

The early signs of deflation are already visible in interest rates as most developed countries are having rates below 1%. This means that demand for money is low as it can’t be utilized for productive use which will generate a higher rate of return. Further, looking at the yield curve for inflation-indexed bonds, investors do not appear to anticipate inflation type scenario. They do not see a substantial increase in the neutral rate: the yield curve for inflation indexed bonds is negative throughout the maturity structure. They do not see an increase in inflation any time soon: the expected inflation proxied by the difference between the rate on nominal bonds and inflation-indexed bonds is about 1% below the Fed target of 2% throughout. Moreover, increasing debt means it is possible to survive only at low interest rates. Hence, we find negative interest rates in most developed European countries. The fall in economic activity is a shock to the system and central banks are forced to increase money supply at unheard rates to keep the economy liquid and businesses operating. The slow recovery will further take more time to normalize. The losses of jobs due to pandemic are increasingly become permanent. In absence of real recovery, deflation is a real threat in spite of the record money supply pumped by central banks around the globe. The rising number of zombie corporations (those who don’t generate enough cash to pay interest or even fixed cost) is another example.

In part two, we talk about the issue of demography and defaults and the impact these factors will have on the economy.

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.

One thought on “The 4 Ds- Debt Deflation Demography and Default, Part I”