When it comes to achieving success in life, most people accept that hard work and luck with determination and courage to stick the course are most important factors. However, when it comes to investing these factors are rarely practised. Most people try to use their luck in full gear expecting to strike a gold mine by taking letters from a stack used to play scrabble.

Most of us have heard various one liners in stock market like ” Buy low and sell high”, “Buy right, sit tight”, “Rule number one don’t lose money and rule number 2, don’t forget rule number 1”, etc. While such quotes are used to remind the investor about the process and discipline, most investors rarely follow the same.

If making money is so simple then why only few people in stock market become millionaires while rest of the people end up with list of penny stocks (Long list of delisted and penny stocks).

Most often investors get trapped into complex and enticing financial investments which only profits those who create and sell them.

Another doubt arises that when making money is so simple then why we Indians have less than 12.9% of Direct and Indirect Investments in equity in comparison to 26.1% for rest of the world in share market? The image differentiates the Investing pattern of rest of the world with investing pattern of Indians:

Source: Economic Times

Why the probability of making return in stock market is so low i.e. the number of people making money is lower than the number of people losing money despite the fact the market has grown over multiple times?

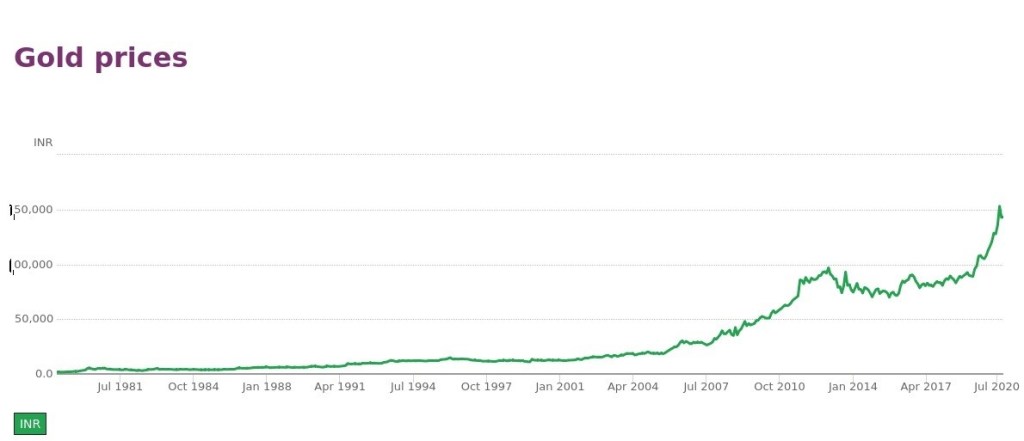

Before making emphasis on above questions, one must compare stock market returns with other assets since 1978. The charts below shows the return of stock market with other assets.

Source: Investingfunda.com

Source: Investingfunda.com, gold.org

As per etmoney.com, the average 10 year return in Real estate investment has been 10%. The basis of such return is based on reports published by several real estate research firms that compared returns from nine biggest cities in India. However, the return on Real estate is relative concept and it may vary from city to city basis.

As per Globaleconomy.com, Real interest rate i.e. Bank lending rate minus inflation

The average value of return since 1978 to 2019 is 5.88 percent with a minimum of -1.98 percent in 2010 and a maximum of 10.77 percent in 1978. The latest value from 2019 is 6.99 percent. For comparison, the world average in 2019 based on 90 countries is 7.16 percent.

After reviewing the above data, the return from Stock market returns does appear to be lucrative and superior than Other Assets class. The difference is that in other asset classes returns don’t change much but in equities, the stocks or index or mutual fund that you pick has different returns than other set of stocks, index or fund. For e.g., if you had invested in gold or real estate 20 years back, the returns are similar across the individual asset class. If you bought 24 carat gold, then the price appreciation will be nearly same for all investors across the investing period. Similarly, real estate will also show similar price appreciation within a location/region. However, one must also consider the fact that the stock market constituents never remained same since 1978. The constituents changed from time to time. Like in 1994, the index had 14 Tata group companies as constituents in BSE but right now the number has been reduced to 3. Reshuffling of constituents always occur from time to time. But for other assets, the nomenclature has always remained same. The constituents of assets since inception remained same.

Plus, there are allocation issues. For e.g., consider a scenario where you invest 1% of the portfolio in a stock which you have less conviction on and invest 10% in a stock where you have more conviction. If the stock where you had less conviction, rises 200% while the one where you had a strong conviction falls 20% you earn nothing. Since investing requires diversification, as a less diversified portfolio becomes risky of not yielding any returns in case systemic or asystemic risks come into play, it is therefore difficult to yield higher returns on a portfolio basis unless your allocation is right which is not the case with some other asset classes.

Therefore, for an investor to pick the best stocks in equities as an asset class is much more difficult than other asset class and hence the probability of investors making returns reduces.

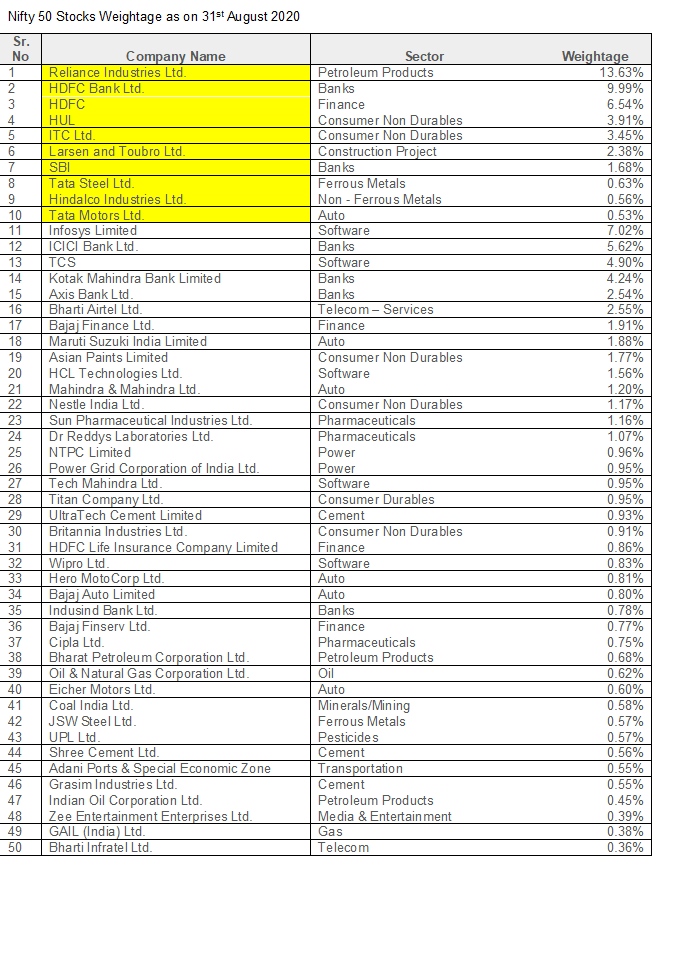

The data below shows the constituents of Index as on 31.08.2020 along with weight in index:

Source: NSE

The Companies marked in yellow colour are the companies which remained in NSE since inception. So out of 50, only 10 companies remained same since inception of NSE.

Most of us have heard that if Rs 100 invested in 1978 in BSE INDEX can turn out to be more than Rs 40000 as on date. Now the biggest question is how the same can happen when the index itself consisted of some companies like Satyam which proved to be laggard and destroyed the wealth at the rate of 90% in three days. The same happened with Zee group stocks. Many instances were noticed. Even the stock of ACC went up to more than 8000 mark in 1994 and then hammered to a value of 20%-to 30% from the peak. Who would have imagined such stocks could form part of index and later they were thrown out from index.

Further day in and day out the weights of companies always changes at rampant pace. So, one can imagine the amount of hurdle if one had invested in 1978 in index companies and the same person reshuffle its portfolio based on weight. The concept of long-term investing would end up as trading in such scenarios. Had it been in other asset class, the investor could have peace of mind in holding asset without reviewing the day to day movement and price fluctuation. That is why Indian women holding Jewellery have outperformed various indices without any efforts.

In past 100 years, several large crashes happened in market like1929 (US Market), 1987,2001, 2008, 2020, etc but what we have heard all the time is that ” This time is different”. To the contrary at each and every time, difference is that the participants in the peak market changed. The hands in which the stocks were dumped were always new. Besides, the problem exists with information asymmetry as managements over time have been found short in protecting investor’s interests and frauds have dented the image of many companies leaving behind a big trail of investors who have lost their hard-earned money. While caveat emptor can be applied in all cases, in case of stock market it is bit difficult. Even if one tries to analyse the balance sheet and look at all the aspects of business, one may fail to understand the issues ongoing. Case in point is the recent NBFC crisis. Nobody ever sees it coming.

Why people tend to lose money during crashes?

All bubbles occurred with certain themes. In 1999, the theme was technology with internet (so called dot com bubble) or the theme for 2008 was real estate, infra and capex cycle.

All these themes have been executed and are practically visible on grounds but investors practically lost massive amounts of money in stock market by investing in such stocks.

The reason is very clear. Roughly the retailers participate when the story of prevalent themes get bloated and published in media. The streamlined media like newspapers, journals, Twitter, TV channels, what’s app groups floats all the biased information. This tempts investors to invest in even stocks with questionable management and business practice with the aim to get multi bagger returns in stock. It is believed that investors enter into a story or bubble when greed index crosses 70 percentile. In fact, they get provoked with easy money in stock market. Repeated positive messages about a particular stock or a theme makes investors complacent or even over confident without understanding the risks. This borrowed conviction proves to be faulty. Even at the peak of the bubble, you can listen recommendations of stocks from your neighbours or from your relatives who never had any interest. The diaspora of easy money makers is at peak during such time. Many follow them just trying to catch up and make some money in the process. Thus, investors become victim of such euphoria. The herd grows without anyone noticing. If history is any indication, most returns are made when a theme is in its infancy. Identifying a theme or a sectoral play is not an easy job and requires deep understanding of how physical markets/sectors work.

How does permanent loss of capital arise in peak bubble?

During peak bubble, people tend to avoid fundamentals and start picking stocks which are trading at prices far above fundamental value. Further, in case of cyclical stocks people tend to enter at the peak of cycle believing that cycle is structural change and will continue forever. In fact, at that time 99% of investors never study the fundamentals or Audit report or do due diligence analysis. But one thing never gets changed “The though process of being long term investor”. They enter with the intention of quick short-term return and end up being long term investors under the gist of frustration.

The example is the recent rally post March 2020. Most of the top Nifty stocks got doubled from the lows. These stocks had underlying fundamentals. But to the contrary the most searched stocks in Google were those penny stocks whose scams have been disclosed before the crash of 2020.

One example is Yes Bank. After burning massive amount of capital, still retailers are busy in averaging the stock. They believe that the rally in market will also take this stock to old glory. This is how the rally in market diverts people from fundamentals and the divergence becomes too large that people end up burning their hands at the peak of bubble.

Why the probability of making return in stock market is so low i.e. the number of people making money is lower than the number of people losing money?

Often an advertisement is floated in Media saying if you had invested Rs. 17 in Eicher Motors in 2003, it would have turned into more than Rs. 20000 in 2018, or if you have invested Rs. 360 in MRF 2006 then it would be converted to more than Rs. 70000 in 2018. Then comes the peak hype about stocks like Wipro, Infosys or ITC than an “X” amount invested in Infosys in 1990 decade could have earned you more than 10000% return as on date. Yet nobody mentions that Infosys IPO was under subscribed by retail and no investor was betting the farm on it. It wasn’t the flavour of the season. Consider today that an IPO can get 100x subscription in the same sector even though it may not be comparable to Infosys. Or how many people would have had 10000 Rs to invest in those times. In hindsight, everybody is a market expert. But how many had the vision that a particular stock would achieve such great heights.

These advertisement looks lucrative and makes one believe that easy money can be made in the equity markets. As one enters during a bull market, chances of loss are less and investors enjoy initial success which reinforces their belief that they can make easy money only to end up losing their investment capital during end of a business cycle.

So when such stocks are easily available then why we have less than 12.6% investors invested in market. It definitely matches with the probability i.e. number of people losing money is higher than number of people making money.

To explain this concept, we need to think contrary. Various companies in the market quoted at tripled or four digits valuations from just single or double digit valuations. Like from the above para we can take example of Wipro or Infosys values reaching at skies during technology bubble. Or take example of MMTC which crossed Rs 20000 or OMDC which crossed Rs 91000 from Rs 1200 levels or ACC whose value was bloated from Rs 300 to 8000 in 1994 or Suzlon whose value was more than Rs 720 during 2008 Boom or Reliance Communication whose value was more than Rs 700 or DHFL which went up to more than Rs 600 was Rs 80 or Yes Bank which went up to more than Rs 1200 or Educomp which went upto 1600 from Rs 80. Are these stocks not multi-baggers? The answer is yes. But what happened to the investors and their returns in present? Look at the value of such companies at present like Reliance Comm trading at less than Rs 2, or Educomp at Rs 3.20 or Yes Bank at Rs 14 which even touched Rs 5 or DHFL which is at Rs 14.40 or Suzlon at Rs 3.30 or MMTC at Rs 18.05.

Majority of Investors have burnt hands while entering into such stocks when the same stocks quoted at half price from their peaks. Remaining people would have burnt their hands by entering when such stocks became 25% of its value from its peak. Now question is why people enter into such stocks? The answer to such question is very simple. The media and management tries to play with the sentiments of retailers. The fake news games start, story of mergers and acquisitions picks up the pace and sentimental stories starts. The idea of something good available cheap makes people want to invest even in uncertainty as they feel that the management will be able to turn around. However, few take the effort in understanding the problem. In nutshell, people start catching falling knives. People becomes slave of such news in order to become rich within short span of time. The greed picks up the pace to acquire huge quantity of such stocks at dirt cheap (As per correction) levels, volatility of stock price conquers the mind and fear of missing out the opportunity starts. In short, the love for such stock develops. Soon such shares become a permanent feature of the portfolio when the management gets exposed. And at last the retailers who bought such stocks becomes long term investors. This concludes the fact that the greed for return in short span of time becomes so heavy that investors take short steps to jump big in life. But they end up by hurting themselves throughout their life. In our country, investors don’t have the skills to do balance sheet analysis. Cash flows are only now been looked at closely. Investors have rarely taken to education. Not to mention most like to follow other investors who have been successful and try to imitate them. But living with borrowed conviction hurts and it is only a matter of time before an investor commits a mistake.

Another thought of lower probability of return is the patience. How many of us would have thought about Infosys would have given more than 10000% return excluding dividend when it was quoting at dirt cheap levels or who could have thought that Eicher would have quoted at more than Rs 20000 from Rs 17 levels. To have that kind of vision, requires exceptional skills and patience with the understanding of the market and macro-economic environment. Not to mention the understanding of management capabilities and competition analysis with deep understanding of the balance sheet. 1 out of 100 who would have thoroughly researched such companies. But out of those 100 also, only 2-3 could have patience to hold such companies for more than 10 years or 20 years or 30 years. Those 2-3 are rarely found in market. It takes extreme efforts to control your mind and heart. Further it requires strict discipline too.

In general, one can only see portfolios which are 30-year-old and multiple scrips appearing in portfolios which are either not traded or delisted or the companies went bankrupt.

At last to emphasise this point, we can only say that there is no free lunch in life. Investing in equities is pure casino without patience and hard work and such people end up by applying 100% of their luck in market and later criticise their destiny.

Conclusion

To conclude with above, we can only advise to do your due diligence before investing. Listen to the gossips or news or any material from media but do invest after your proper homework.

Before jumping in direct equities, one must learn the tools to analyse them. Basic understanding of the macro and micro economic environment, global currency, debt and bond market understanding, sector analysis and balance sheet and cash flows are necessary to deal with systemic risks. Most important however is management analysis and here it is even more difficult as their actions have to be compared over the years on delivering returns and maintaining promises.

Whether you become a short term trader or long term investor, always think in terms of the company’s ability to deliver. If the history of the company has been such that it has given poor returns over a long period then the risk in investing increases irrespective of the time period of investment.

Over the past six months, we have seen many friends and relatives asking for tips and stock names for investing. We have always refrained from giving names because we believe it is the process that is more important than the end outcome. If investors are unable to understand the business and management and are investing on borrowed conviction, long term investing will seldom work.

As the world markets becomes increasingly volatile due to geopolitical issues, investors patience and understanding will be tested severely and very few will be able to maintain emotional stability and stay in the game for the long term.

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.

One thought on “Investing Psychology”