Day in and day out we have read that the Mortgage default in China has started but none of the article is able to give detailed explanation that why the borrowers are defaulting against loans. Not only borrowers but business loans defaults are also taking place in China. The only reason given at present is fall in real Estate activities and its spiral effect. In this blog we will discuss with our readers in depth that why Borrowers are not repaying loan and how Banks are in deep mess due to non-repayment of loan.

Let’s start with our favorite Evergrande mess from where we started writing Blogs related to Chinese Debt crisis.

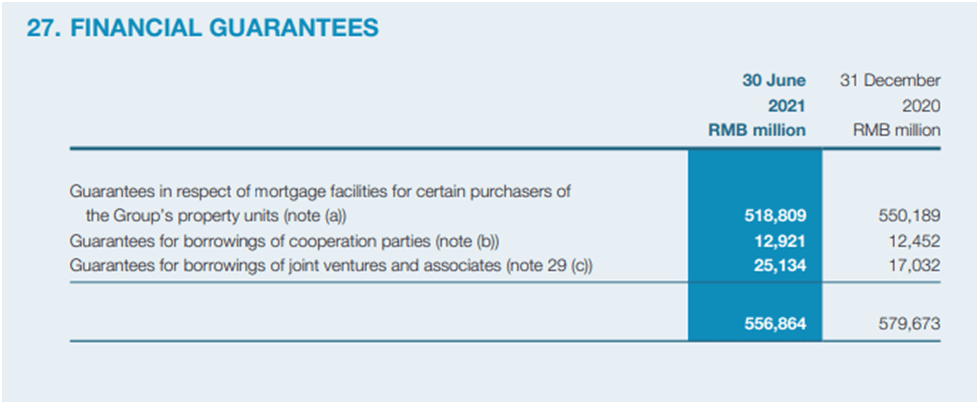

When converted into dollars the liability comes out at 87 Billion dollars alone for Evergrande. Out of this 87 Billion dollar, 81 billion dollars is for mortgage loans.

Let’s see what are these financial guarantee means for Company?

Now let’s understand in layman language with simple example

(a) Mortgage Loans

Suppose Mr. X is China wants to buy property in China from Evergrande for RMB 500000 but Mr. X doesn’t good Creditworthiness (Banks have doubt on his repayment capacity). In order to increase sales, growth of company and considering the past 20 years trend of appreciation in property, Evergrande gives guarantee to Bank for Mr. X that in case of default Evergrande will pay his debt to Bank and will take back the flat from Mr. X.

In this case Banks get sufficient collateral in the form of Flat as well as Guarantee of Second largest developer of china. So in this case the quality of loan is superior.

The concept is not a rocket science to understand but let’s go further deep into this concept:

Suppose Evergrande is constructing 20 floors Tower and Mr. X booked his flat at 16th Floor. Till date 60% of loan has been disbursed whose Equal monthly installment was repaid by Mr. X on time.

Now Evergrande gets into financial crisis. At the time of crisis, Evergrande was able to construct 14 Floor structure and the work remains standstill. Now what will be situation?

Mr. X was never having repayment capacity. Bank will invoke guarantee of Evergrande which is already into deep financial mess. Further Bank was having Flat as collateral security in the form of under construction tower whose 14 floor structure was completed till date.

Now why will Mr. X pay and Evergrande guarantee will not work due to financial crisis. At last Bank will try to sell the flat booked at 16th Floor but who will buy those flat which have never come into existence.

So at the end Bank will try to recover money from Mr. X only who will always refuse to pay back his loan.

In nutshell, this is the real problem of Chinese Banking collateral wherein the asset has never came into existence and Banks are considering as secured loan. At the end who will be pressurized? Its disgruntled Mr. X whose property has never came into existence and he repaid EMI for that un-built property.

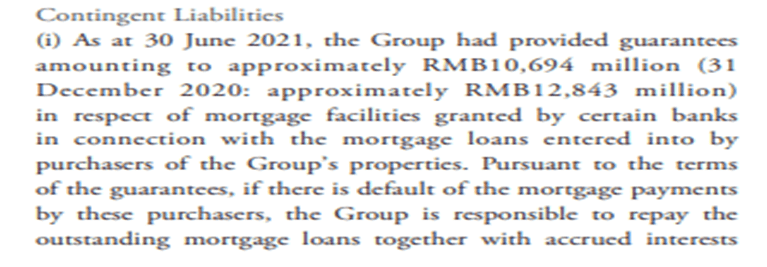

So alone Evergrande holds guarantee of $81 Billion on such Mortgage loans and media claiming $40 Billion liability.

Business Loan

Recently, news related to business defaults have also floated business defaults of Loan provided. What is the most common practice in china was Bills of discount.

Let’s understand in laymen language. Suppose Mr. Y was awarded construction contract from Evergrande for RMB 20 Million and Mr. Y has only RMB 1 Million cash. He starts the work where he raises his first bill of RMB 2 Million. Now as per payment terms of Evergrande, post approval of Bill Evergrande will take two months to pay the bill. In between, Mr. Y needs to pay his workers and discharge his direct tax liabilities. So he request Evergrande to release payment within month’s time. Instead of releasing payment, Evergrande ask Mr. Y to go to Bank and get the bill discounted i.e. Banks will pay Mr. Y 98% of amount due and keep 2% as commission. The payment released by Evergrande will directly be repaid to Bank instead of Mr. Y. So in this case Mr. Y will get RMB 0.98 Million and Evergrande will pay RMB 1 million directly to Bank.

So all in all this was the face value Evergrande to keep that Bill as security. The size of such business loans are big as in case of defaults Banks will again ask Mr. Y to repay the amount to Bank and this situation will force Mr. Y to default on such loans.

Let’s see the liabilities of Country Garden, China Vanke and Fantasia.

Country Garden

In USD terms it’s $59.817 Billion for Mortgages.

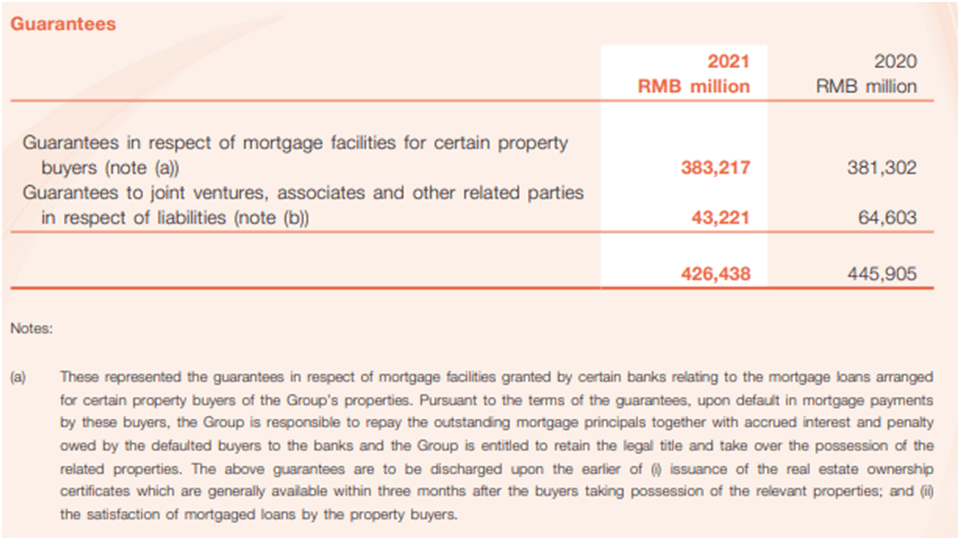

China Vanke

In USD terms it’s $35.66 Billion for Mortgages.

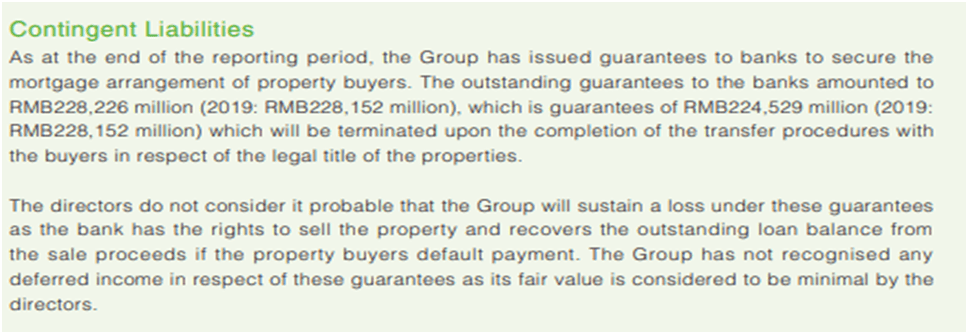

Fantasia

In USD terms it’s $1.67 Billion for Mortgages.

In USD terms it’s $22.83 Billion for Mortgages.

Conclusion

If we present the liability of Top 5 Builders, it comes out at $201.03 Billion Dollar.

| S.No | Particulars | Guarantee for Mortgage Loans |

| 1 | Country Garden | $59.817 Billion |

| 2 | Evergrande | $81 Billion |

| 3 | China Vanke | $ 35.66 Billion |

| 4 | Sunac | $22.83 Billion |

| 5 | Fantasia | $1.67 Billion |

| Total | $201.03 Billion |

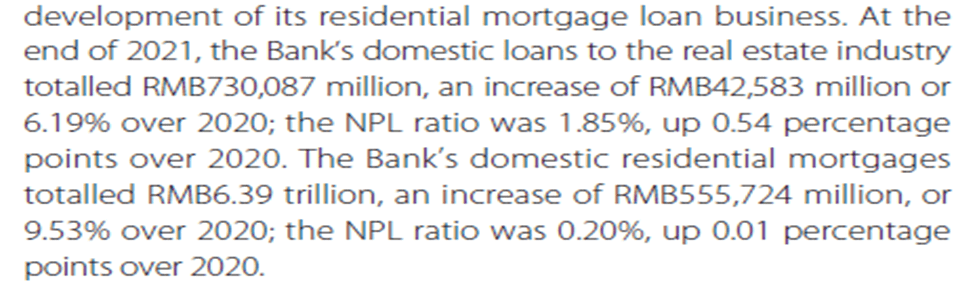

What media floated articles claim of $40 Billion seems to be much lower as the same is evident from above contingent liabilities. Further in order to cross verify the same, we came across the figures of China Construction bank. The abstract is as follow:

In terms of Dollar Mortgage Loans are $1 Trillion and Real Estate loans are $114 Billion. So all contingent liabilities of developers were indirect means of Finance to Real Estate Developers. Its methodology to distribute the defaults to individual buyers at the cost of mismanagement of Real Estate developers.

At the end the official numbers of Mortgage loan can be too high and One Trillion dollar is just offically verified figure. One thing readers can try to remember is that big real estate players like Evergrande were targeting peripheral areas outside the big Chinese cities whose prices will have seen a higher negative impact of the pandemic as compared to the city area. Therefore even less incentive for these buyers to pay the remaining of their mortgages unless their assets are worked upon.

By CA Nishant Maheshwari, Vishal Vora

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Account Holder Name: Rashi Maheshwari

IFSC:SBIN0030115

One thought on “CHINA’S MORTGAGE DEBT DEFAULT- TRILLION DOLLAR RISK!”