Since September 2021, we have written a lot about Chinese Real Estate problems along with Local Government Financiang Vehicle (LGFV) model of China. Since the same is talk of the wall street, we need to concentrate on future currency problem of China.

We all are tracking movement in market on day-to-day basis. But the real problem still lies with understanding of market as our concentration is more towards movement of market rather than what market is hiding. We have certain lead indicators which tells the future problem of Market at present. One such indicator is Chinese Yuan.

The foundation of this problem has been sowed by the real estate crisis which started two years back. The leaders like Country Garden, Evergrande, China Vanko, Fantasia etc were all sailing through in anticipation of bail out from the Government but the CCP had only one motive i.e deleveraging the Chinese economy by hook or by crook. Due to the real estate crisis, the bonds of leading companies like Evergrande are quoting at more than 100% yield and are trading like penny. stocks Some of them have been barred from trading.

The spiral effect of real estate further spread to the State-owned entities which were on the verge of Bankruptcy but were sailing through Land sales in order to raise new fund and discharge the existing debt or meet out coupon payment. But the same has stopped and now the situation is more cumbersome.

In spite of all such events and turbulence in debt, the Stock Market of China haven’t reacted. But the Markets in Hong Kong have reacted badly. We have seen the share prices of real estate leaders trading like a penny stocks. Chinese market did not react much as the market is opaque and game is related with more brokers and insiders. Thats why Chinese market has not given return since last many years.

The further spiral effect of Real state occurred in Banks where Retail borrowers or Housing loan defaults started. Now most of these loans default is on account of contingent event guarantee given by real estate developers but these events play a major role in deteriorating sentiments. Further in future we will see defaults in Bills of discounting where supplier of developers will default in loans. All in all, the last event will be collapse in value of artificially hyped collateral value against loans in the form of under constructed and fully constructed properties.

The next crackdown which has been already discussed in detail by media was Tech crackdown and probable delisting tech stocks from NYSE where leaders like BABA are quoting at one third value from peak high. We won’t discuss this in detail because the same has been analysed by media multiple times.

Another factor where major allegations will happen for all such disaster is Lockdowns in China for Zero Covid policy. However, the best thing about same is that the production never stopped in China. This policy made people restless in communal environment. People are forced to hunt for Survival causing high unemployment rates in double digits.

The above factors are all related to factors influencing Yuan.

Let’s analyse the impact on worlds largest market i.e Currency Market.

China makes up 28.7% of the total global output for manufacturing. World has highest level of dependency on China. Now coming on to USD. U.S. dollar is the dominant currency in international banking. About 60 percent of international and foreign currency liabilities (primarily deposits) and claims (primarily loans) are denominated in U.S. dollars.

Guess what, the frequent rotation is done with the help of China. While the world was importing from China, China with its pegged currency was rotating dollars globally. It is estimated that more than 17% of Global trade in dollar happened with the help of China. Not to forget that the QE or Stimulus or funny money played a big role in that. Till date the new dollars got printed, system never asked or anticipated for any problem. Now globally the Stimulus or Funny money stopped and QT of funny money or mad money started.

China is a exporting nation. In spite of the largest population,China is not a consumption based economy which it aspires to become. Rather, Chinese economy created a Assets class bubble in the form of Real Estate which directly contributed to GDP by 30% (Estimate) since 2010. But just like rubber band, you cannot stretch your bubble to indefinite period. In the same way, Chinese Asset class bubble has been stretched to its peak. This has resulted in decline of capacity utilization of Major capital goods producer like Cement, Steel & Other Construction material. In few cases the largest producers of Steel or Cement are on the verge of Bankruptcy. Almost a third of China’s steel mills could go into bankruptcy in a squeeze that’s likely to last five years. China’s steel industry is entering a precarious new era as a worsening property crisis imperils demand and Beijing’s construction-led growth model looks increasingly untenable.

Eg:Wuhan Iron & Steel Pipe Industry and Shandong Kerui Steel Plate voluntary applied for Bankruptcy

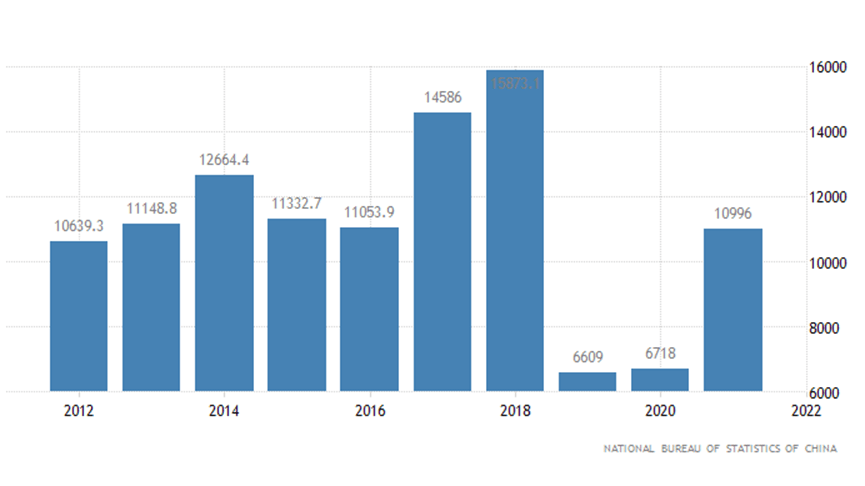

It will be a surprise for our readers to know that China has 803 Integrated Cement Plants with a 60% of Global Production. In 2020,China’s cement capacity utilisation rate was only a little more than half (52.3%) of the total, and in recent years, new replacement capacity has been put on the market, so the cement and clinker supply market has sufficient resources. Post crisis the same has fallen drastically and even the leaders of cement industry are operating below 40% capacity in China.

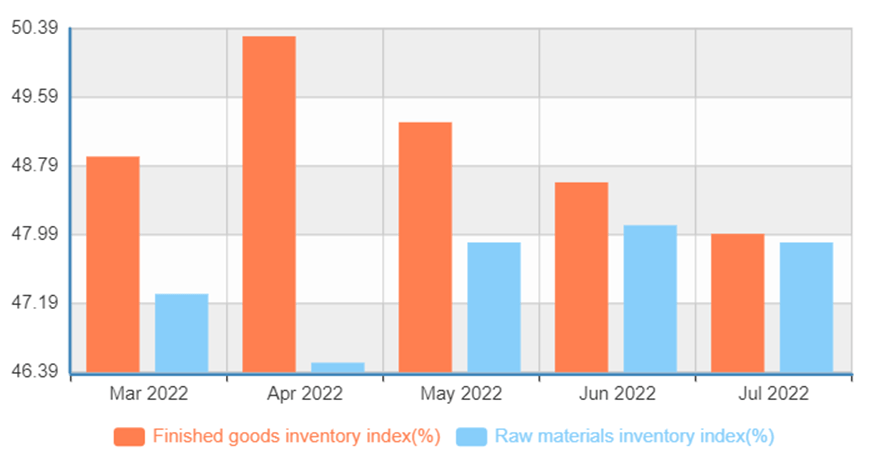

So, with above explanation we have justified our viewers about capacity utilisation problems persisting in China. Now coming on to Inventory levels in China. Lack of demand creates reduction in capacity utilisation but at the same time you need to operate your factory and produce something in order to keep your machines in running conditions. So lets analyse the level of inventories piling up in China.

So combining the Raw Material and curtailed production of finished goods, the largest manufacturer is experiencing some hidden problems.

Next one is the Slowing Capex whose effect is been seen in Countries like Japan and Germany. The dependency on China for these Countries was too much:

The slowdown is real in spite of the type of quality of Data which China publishes.

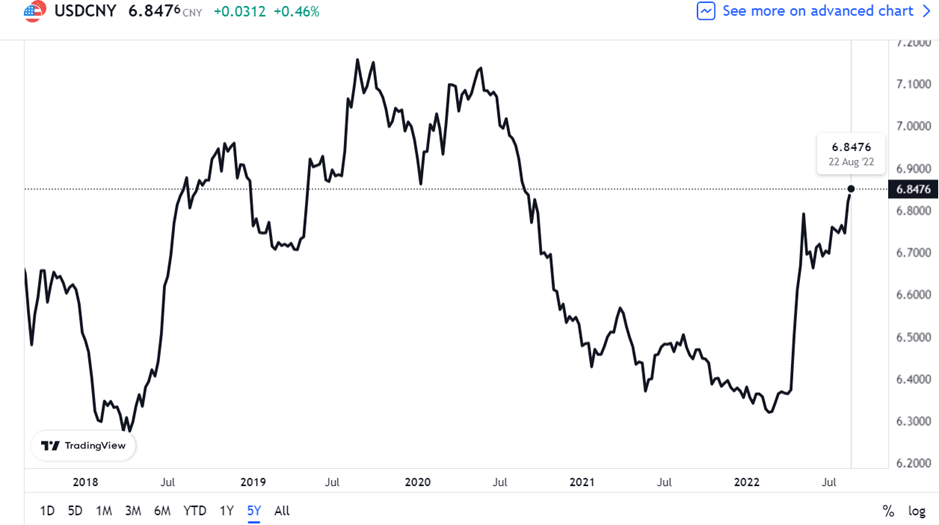

Last but not the least Interest Rates. The People’s Bank of China cut its rate on a one-year loan to 2.75% from 2.85% and injected an extra 400 billion yuan ($60 billion) into lending markets after growth in factory output and retail sales weakened in July and home sales fell by double digits.

Now in the times of competition for Interest rate hikes where the father of all central Bank Fed is speeding up the hike of Interest rate along with ECB and rest of the world, China is reducing the interest rates. A layman can also understand where will currency go when Developed nation’s central banks are hiking interest rates.

The charts are speaking below:

Conclusion

China’s growing economy was the engine of global growth. It is now seeing weakening real estate market, lower capacity utilization in industry, Taiwan issue leading to geopolitical interests rising, a weakened consumer and lot of defaults impacting credit markets. Adding to weakness in China, we are seeing impact of war in Europe and energy prices impacting demand in europe and USA. With high inflation, lower global growth and a tapped out consumer, China will be desperate or dollars. In 2015, a similar situation existed and China lowered it’s currency value . It sent deflation to the other parts of the world. China is once again in a similar situation. CAN THIS TIME BE DIFFERENT OR WILL IT CALL FOR YUAN DEVAULATION?

From CA Nishant Maheshwari and Vishal Vora

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Account Holder Name:Rashi Maheshwari

IFSC:SBIN0030115

Name of Bank:State Bank of India, YN Road, Indore