While the whole Financial experts of twitter are claiming different kinds of news about Credit Suisse which relates to probable failure of Bank. So before concluding whether Credit Suisse will be a real failure or not, let’s analyse new type of points which substantiate in detail about this Bank:

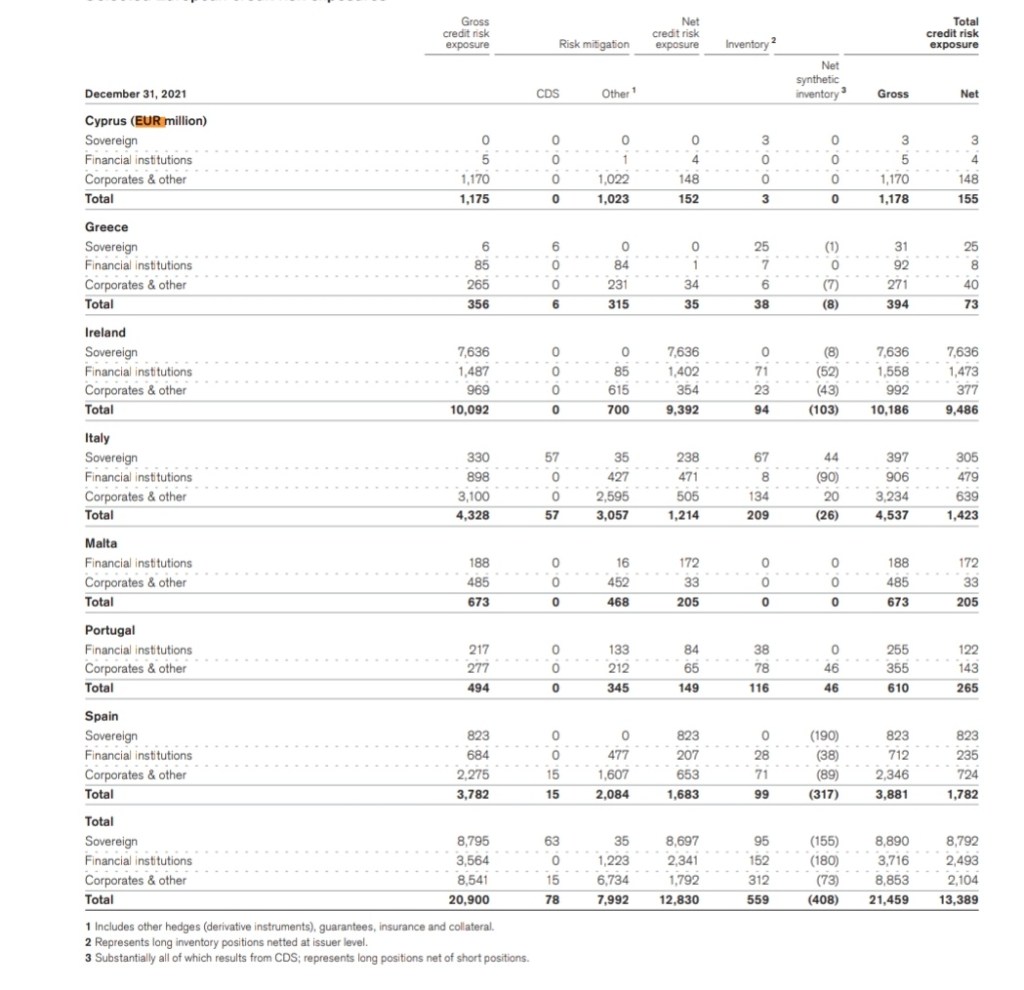

Contingent Credit risks

The following table provides the Bank’s current net exposure from contingent credit risk relating to derivative contracts with bilateral counterparties and special purpose entities (SPEs) that include credit support agreements, the related collateral posted and the additional collateral that could be called by counterparties in the event of a one-, two-, or three-notch downgrade in the contractually specified credit ratings. The table also includes derivative contracts

with contingent credit risk features without credit support agreements that have accelerated termination event conditions. The current net exposure for derivative contracts with bilateral counterparties and contracts with accelerated termination event conditions is the aggregate fair value of derivative instruments that were in a net

liability position. For SPEs, the current net exposure is the contractual amount that is used to determine the collateral payable in the event of a downgrade. The contractual amount could include both the NRV and a percentage of the notional value of the derivative.

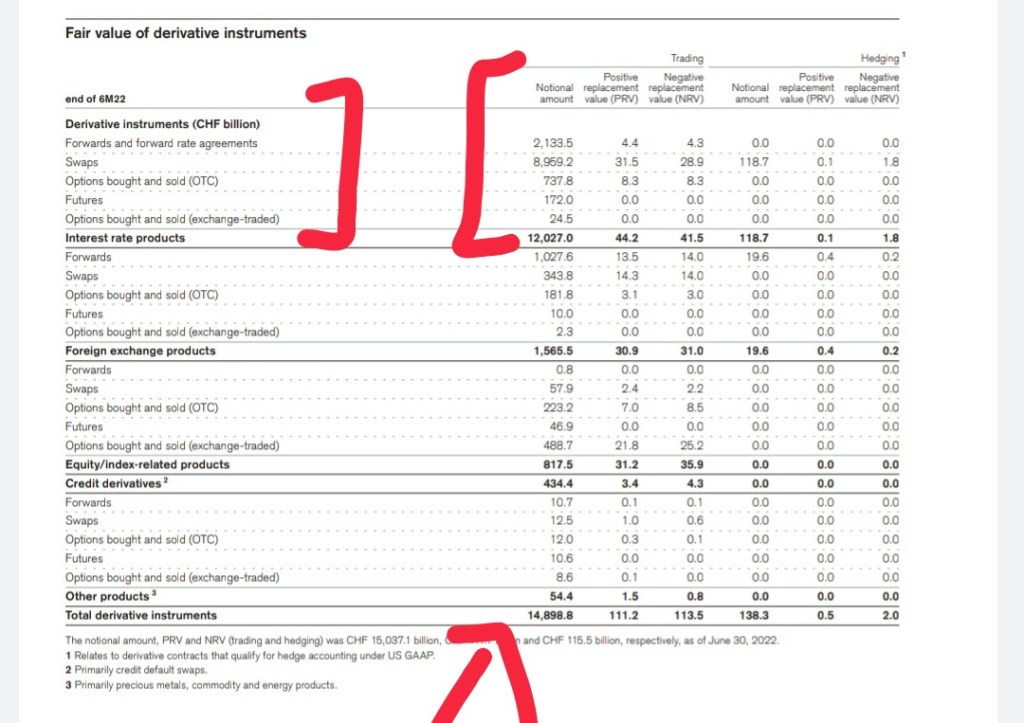

Derivatives and hedging activities

In the times of robust liquidity due to constant money printing, the biggest risk to any system is derivative market. This market flows can cause severe damage if the things are not properly hedged. Let’s see the exposure:

While the whole noise is related to derivative products but nobody was able to explain the quantum.and category of product. The notional amount of total derivatives is roughly CHF 14.89 Trillion or 14.74 Trillion dollar and major exposure is in Forward and Forward rate agreements and swaps where majority of movement has happened in recent market correction. The unhedged portion against the size of trade is now becoming costly for Credit Suisse. The synthetic products are real risk in system. It eats up the whole reserves like Turmites and everytime you need bailout to safeguard the investors against probable losses. $12 Trillion alone in derivatives and 1.54 trillion dollar in Interest rate products make weird combination and gives more signs of mis-happening when we see turbulence in this market since last January 22.

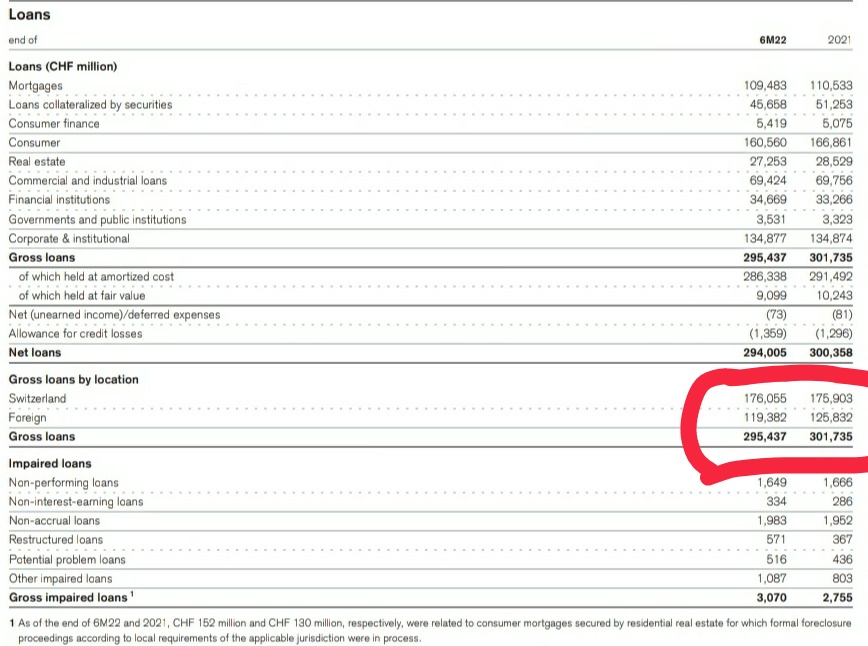

Loans

Life becomes miserable for any kind of Bank when you lend in domestic currency and recover the loan portion in that currency only. On the other side the balancesheet is required to be prepared in strongest currency like CHF or Dollar.Recent currency depreciation has caused severe dent in the books of CRedit Suisse. Specially the loans advanced in Euro or Lira or CNH got converted into huge losses due to constant depreciation in these currencies. Though the recovery could be smooth but capital erosion cannot be neglected but it can only be hided due to evergreening concepts in Banks.

The 41% of loan portion is exposed to risk of currency depreciation.

So.with all these points lest end our last point with stock prices.

Conclusion

The prices of this company is telling some severe problem in this company and the major portion of risk is related with synthetic derivative products and major cause of problem is currency and interest rates movement. Speculation and it’s excecution have acted in inverse manner. The cause of worry is big and people are again in hope of bail out. So after such correction in stock price let’s see how speculations will cause volatility in stock prices but the fundamentals will remain garbage.

The problem is long and carried prolonged. Now the same has reached the peak.

- By Nishant Maheshwari and Vishal Vora

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

IFSC Code: SBIN0030115

Name of Bank: SBI India, YN Road Branch Indore-India

Account Holder Name:Rashi Maheshwari