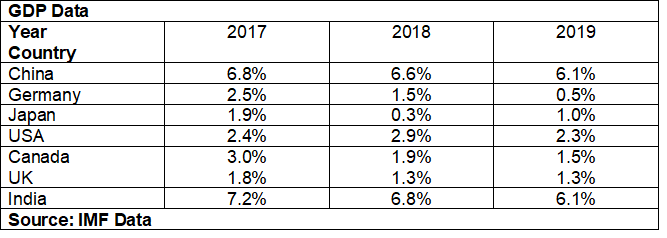

As we discussed in Part I, while the virus may have been the needle, the bubble was already looking to deflate. Global economies were seeing lower growth projections. China had already reduced its GDP growth estimate to 6% from 6.5% with analysts further reducing target GDP Growth to below 5%. Similarly, India’s GDP growth dipped to 5% while US GDP growth was stuttering around 2.4% (2019) and only kept up by tax cuts. Unemployment has been creeping in and real estate sales around the world were weakening. The stock market was the only place booming with daily repo operations saving the markets from reversing. It was only a matter of time when a single snowflake would cause the avalanche. However, risk comes from the most unexpected places. In this case a global pandemic threatening economies and businesses in particular. Below stated GDP numbers of last three years depicts the state of global economy in recent times.

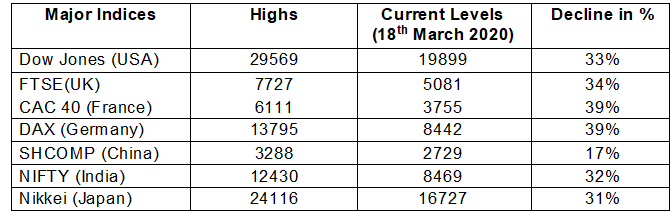

While impact of corona virus has been felt in most countries, the biggest impact has been on financial markets and businesses. Worldwide, governments have already started bailing out the major corporations that have suffered heavy losses due to the pandemic. They even need to bail out consumers. At this moment, Hong Kong and Australia are already providing financial support to consumers and small businesses. USA government officials are also thinking on similar lines. While there is a need to take measures to prevent the rot, there is a possibility that the medicine will be more dangerous than the disease. Major central banks have no ammunition to fight another slowdown and have spent all their ammunition in fighting the economic depression wrath of the virus. The Financial markets are in deep pain and are in bear markets zone (Down 20% and more).

Given past experiences, it is already known that some stimulus will be needed. But the extent of stimulus announced is dwarfing the entire stimulus announced during the past ten years (For details on stimulus measures announced, visit https://sebmarketwrap.blogspot.com/2020/03/global-central-banks-capitulation.html?m=1 From Sebastian Sienkiewicz twitter handle @Amdalleq). The reason for the stimulus may be debatable but the basic problem is that majority of the consumers, businesses or governments are knee down in debt and it is impossible to kick start the economy without the stimulus. One can’t argue that truth. But it is the same remedy that was prescribed in the last crisis and surely it hasn’t worked. Even though many experts have warned against this, I am sure the same policy will be implemented going forward because difficult decisions require leadership to execute and bear pain. At the moment of writing, we are witnessing a deluge of stimulus measures. Cheques sent to each household, bailing out corporations, discount windows for banks are some of the measures already announced.

Yet there are questions that need answering.

1. Will this be enough?

2. What happens if the virus persists and we still are in a depression?

3. What are the side effects of the stimulus measures?

Most governments are worried about been short of doing enough and hence they are intervening daily in the markets and announcing stimulus measures on the go. Day in and Day out, the quantum of money in the form of stimulus is increasing and it is difficult to say whether it will be enough but there is reason to believe that there will be no effort left in providing as much stimulus as required. The problem is whether we overdo it. If excessive stimulus is provided and economy is provided with huge liquidity, it will reduce purchasing power and increase money velocity while adding to inflation. Bond yields may increase and credit markets will freeze forcing central banks to buy their own debt, kicking them into a corner.

It will be difficult to ensure financial discipline and markets will get used to this moral hazard which will be demanded every now and then. The biggest worry is if the underlying currency starts losing value and stimulus needs keep on repeating due to weak economy, there is every possibility we may see episodes of high inflation in many countries.

Therefore, in trying to remove the effects of the virus central banks may create unintended side effects and cause a deep financial crisis that takes years to resolve.

There are always Markers

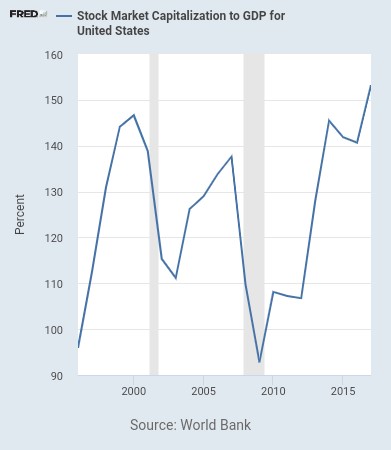

Could this have been foreseen? The answer is that some markers always exist. The choice is whether we look at them and try to find out what they are actually indicating or we just ignore them. One of the markers was the Buffet’s favourite Market Capitalization to GDP ratio which went as high as 160% for the Dow Jones.

The other was the repo operations indicating that there were serious issues of liquidity in the USA market. The third was declining GDP growth rates in spite of constant stimulus. Valuations were already extreme and PE expansion had reached for the sky. Bursting of the start-up bubbles was another. Insiders were selling at every opportunity. Increasing retail participation with high number of accounts opening with insiders selling meant last stage of a bull market. Multiple warnings from IMF and BIS pointing towards debt crisis were left unheard. Multiple factors were all pointing to a slowing global economy.

Yet investors were buying hand over fist and deploying all their cash. The herd had become insane and began trading as a pro. The bubble was waiting for the pin.

The Bursting of the bubble

Tops are a process. They take time and so is the bursting of the bubble. It waits and waits and sucks in everybody till a single snowflake is enough to cause an avalanche.

The snowflake came in the form of virus. It started initially in China, spread to its neighbours. Even though the virus was spreading, it was thought to be localized initially. Most countries were not planning on much except banning travel. But once the virus started spreading, the uncertainties started growing with respect to the supply chain. The stock markets grew worried as they had not factored in the implications of the hit to the global growth and to the earnings estimate. Most of them were already too rosy and were dependent on stock buybacks to boost E.P.S. Markets hate uncertainty and they started falling. The initial selling was met with buy the dip mentality as markets have been trained to follow over the past few years. If they fell more, the Central bank ‘Put’ will be activated and a stimulus measure would lift all boats. This was the typical mentality that had worked so well in bull market.

However, it was not much different. Central banks did come to the rescue. But by then, the virus had reached the western shores and throughout the globe. With markets falling, passive investments and risk parity funds started breaking. Losses beget more selling and it soon became and avalanche. With the system having no asset unencumbered, collateral became difficult to post. Liquidity became scarce. Central banks did try to pump in liquidity but the world needs dollars and that too in trillions to pay off their debts. This is now a liquidity crisis. Credit markets are also responding with the H.Y. spreads rising to levels comparable to 2016. Oil has fallen below 22 dollars indicating depression and huge supply issues with little demand to support. Currencies of commodity exporting countries are into free fall with strong dollar aiding the fall. Rate cuts are a daily exercise. So is trillion dollars stimulus. It needs to be seen if the liquidity crisis causes a default wave of corporations which comes to haunt the banking sector. That to me is the biggest threat in the financial side.

In the real economy, the number of unemployed is increasing as corporates cut back on expenses and depend on government bailout packages. Those that are not reducing employees will cut back on salaries. Defaults on credit card debt and household debt needs to be watched. Even though government are announcing fiscal stimulus for consumers (income for a small-time frame to meet the expenses and mitigate disaster), most of it may be used to pay their expenses and reduce their debt. This won’t spur demand which is now getting hit from all sides. Already estimates state that the US may see unemployment rise by 3 to 6 million. This is even higher than the 2008 global financial crisis.

There are now multiple shocks to the system:

- The volatility shock to the markets

- The liquidity shock

- The demand shock

- The supply chain shock

- The credit markets

- The debt burden in the emerging markets & dollar shortage

- Banking system stability

- Currency shock

With the data that’s coming out, comparisons are now been drawn to the 1929 Depression. Inflation may become a risk in the short term given supply constraints. But an outright Depression can’t be ruled out too in the medium term given the loss of jobs and demand destruction as firms go bankrupt and consumers have low income. Central banks will try their best not to let deflation take hold of the system by trying to protect asset values. Which is why an inflationary event is a possible side effect. We hope that neither happens but given the issues at hand, they are possibilities that can’t be ruled out yet.

It must be said that this is the perfect storm that none could predict but the warnings where there to be seen. In the last Global Financial crisis, the system was saved by the central banks pumping in liquidity and China reflating the global economy. But the current financial crisis is on a much larger scale encompassing all of the world with little fuel left in the system to fight. Will the Central Banks pull it off? Judging by the reaction, they will be throwing the kitchen sink at it with support from respective governments. But who will save us from the madness that resulted in the crisis in the first place?

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.

Superb

LikeLike