In our first two articles published on the blog( here and here), we had highlighted how fragile the global economy was with its constant need for stimulus and lack of demand drivers. It was informed that the dependence on the equity and debt markets would increase and stock market would become the economy as asset prices get set and would impact significant amount of the population’s net worth. We had also highlighted how the stimulus would stoke inflation, a fall in purchasing power and cause central banks to buy increasing amounts of debt. The blog even discussed how China was on an unprecedented debt binge in history that is now raveling.

One of the points highlighted in the same article was about how trust and confidence keeps the economy going. Especially the trust in the local currency of the country. As we are navigating our way through the pandemic, the economic problems hidden due to the global stimulus are now resurfacing as the stimulus winds up. Inflation has affected the purchasing power and demand in terms of volume is low. Prices are merely compensating the lack of demand. As the supply shocks recede, a clear picture will emerge. But one can gauge an estimate looking at the cuts to the GDP the world bank and Central banks globally are making.

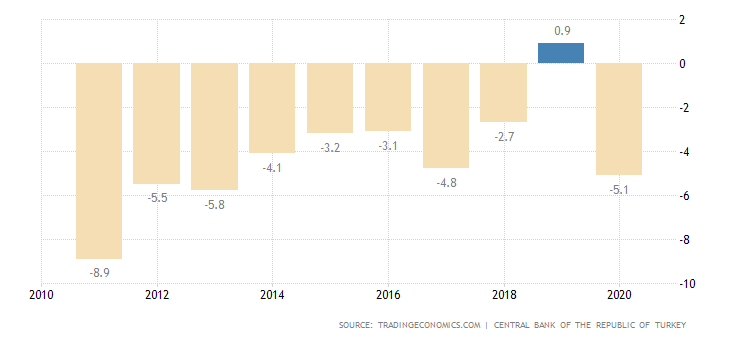

One of the problems that had subsided due to pandemic was the currency wars. The Euro and the Dollar are the most notable of the existing currencies and considered relatively stable. As the economy comes back to normalization, we are seeing side effects of the stimulus and increased debt due to stimulus plus a reoccurrence of the earlier problems. One such example is Turkey which is seeing a run on its currency as people dump Lira and buy dollars and gold. Their stock exchange was shut down as the markets realized the side effects of hyperinflation and began falling. And their leader keeps coercing the central bank to cut rates in spite of rising prices! The broad money supply has risen by 3.5 times in 7 years as per World Bank. Turkey has trade deficits for quite some time and heavily dependent on FDI. The leadership believes in reducing interest rates by increasing supply of money. The opposite effect is inevitable and the country is reeling under high rates of inflation.

Source: Tradingeconomics.com

In addition to this, Turkey is now guaranteeing losses on deposits of lira if the losses incurred are more than the interest rate. These losses will be pushed on the budget and the same will have to be recovered through taxes. It may help to stabilize the lira for the short term however longer term has been a nightmare as it has fallen from 3 to 11 against the USD in 4 years. One wonders what happens when the backstop falls.

Lebanon is another example of reduced purchasing power and rapid inflation. A typical currency crisis can happen basically due to lack of confidence in the underlying currency and usually happens when the central bank or the government goes on a printing spree on an unprecedented scale. It also depends on the structure of the economy and regulatory environment. China is one such case where the regulatory crackdown is making things worse and it is facing a different sort of currency issues.

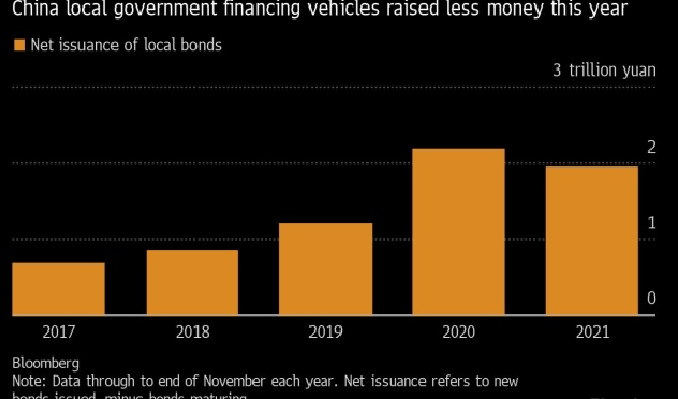

China is finding it unpalatable to increase its debt at a higher rate than usual to fight the lack of demand and maintaining asset prices. Also, political motives have made it difficult to continue with the same process of expansion of debt. The three red lines have forced the real estate companies into a liquidity and solvency trap they just can’t seem to get out. Recent crackdown on the technology sector has also not helped matters. The real estate and construction sector forms more than 30% of the Chinese GDP and a slowdown in this sector is not only going to bring down GDP, it will also bring down demand as the negative wealth effect of Chinese real estate sector flows through the economy (Chinese have 70% of their assets in real estate). Coupled with the fact, that western corporations are increasingly looking to invest in China and FDI has been increasing, China is seeing its currency become stronger with the day. But this isn’t what the economy needs. An export dependent economy would require a stable currency and with global supply chains trying to risk mitigate, it is even more undesirable for the Chinese economy. The economic output of China is slowing and consumer demand is not at the levels expected in spite of the last three years of government focus on increasing consumption. Besides, other economies are taking advantage of their weakened currency and increasing exports at the expense of China. Recently China tried to fix its currency lower but is seeing increased resistance. Also, it can’t leave its door open for currency withdrawals during an economic downturn as it will mean a repeat of 2015. What is impacting China is that while it may have a significant dollar reserve, it may not be enough to save it from a currency crisis. China has a surplus which it tries to redistribute and increase its clout in the global economy. The BRI and global real estate have been its beneficiaries. African governments have also received significant investments. While publicly it has a debt to GDP ratio of less than 60% at the national level, the number increases to 110% when local government debt is added which is assumed to be more than 50 trillion yuan. Banks are the biggest lenders to LGFVs who are the biggest hidden source of debt at the state level. As per Goldman Sachs report in Sept 21, the total debt of Chinese LGFVs is around 8.2 trillion dollars. With reduced revenues due to low interest in land auctions from real estate companies and coming maturities on debt, local government debt will have to be taken over by the CCP at the national level. It may have to backstop and buy the real estate companies as well and take them public too. All this indicate a tough journey for China in the near future and possibly a devaluation is in the offering. Notably China has begun reducing interest rates and revise the yuan lower daily.

Source: bnnbloomberg.ca

What has also happened due to the pandemic, is the need to explore alternative supply chains. China has seen its’ share of covid cases and its zero covid policy is affecting supply of goods globally. Some of its ports are operating at 30% capacity and there is shortage of empty containers as China controls the container market. The rising shipping costs are rising to cost of goods. The trade weighted yuan is also strengthened quite a bit and in some of the sectors, the cost of production is rising and matching with neighboring countries.

In spite of all this and recent steps of crackdown on the internet industry, there has been strong inflows in China while money can’t flow out of China easily and is putting upward pressure on the yuan and making it exports expensive. Recently the Chinese central bank PBoC has been marking the yuan lower and trying to set the expectations lower but the currency is still maintaining its upward bias and there is increased fear that a devaluation may be on the cards. Of course, China can ease the pressure by allowing outward flows but given the steps taken recently and in past, it seems highly unlikely. The only other possibility is buying dollars and increase liquidity which will push the dollar further upward.

One Important indicator of the currency crisis is the dollar index. At the time of writing, the dollar is between 98 and 99. One needs to see the same in the context of the stimulus that was announced in wake of the pandemic. Instead of becoming weaker, the dollar has been the stronger currency.

There are some other countries which are likely to face similar issues. But their size of the economy and ties to the global economy make it a local problem. As the equities market and the bond market remain under stimulus driven binge, problems are likely to appear in the currency market. Investors need to keep a tab on the same.

One of the famous economist Rudi Dornbusch, famously said that when it came to emerging market economies, crises take a lot longer to happen than you think they will. However, when they do happen, they do so faster than you thought they could.

India is another country that is expected to struggle with the currency. Its current account is increasingly becoming negative with crude prices rising and foreign investors pulling out money. While its growth in exports is a good sign, it also has huge dependency on oil. Past three months have shown record trade deficits. As the dollar strengthened it has put additional pressure along with oil. Should oil prices rise as USA moves away from it, the additional burden in terms of crude oil prices will create a further pressure on the rupee. Given it been an election year will polls in many states, the need to expand the budget will increase. The government has made it a policy to reduce imports of other items especially in defense where it has achieved significant success and is now focusing on semiconductors and electronics. The recent PLI schemes and China’s currency strength can add to the improvement in exports. Government is exploring various options to reduce dependence on imports of oil by focusing on renewables and other alternatives. Yet India has dependency in terms of raw materials for electronics and other items in the short term and it will not be easy to get imports under control. This is highlighted by the fact that the rupee was the worst performing currency in Asia in December for some time. India also has a short term debt repayment looming which will reduce its foreign exchange reserves. However, the threat is assumed to be low given record foreign exchange reserves.

However, India’s neighbors are struggling. Sri Lanka is facing blackouts and high inflation. Its foreign reserves are wiped out. Similar situation exists in Pakistan and Afghanistan. Many African countries who have recently taken loans in Euros and dollars will face similar issues as inflation is raging globally due to supply side constraints. Many of these smaller economies need to import medicines, health care equipment and capital goods items and have low export revenues to meet the same while struggling under previously accumulated debt for infrastructure projects.

Brazil, South America’s largest economy, and South Africa, Africa’s largest economy, both these countries now have record public debt levels that are approximately the size of their economies. They also have budget deficits that are now well into double digits as a percentage of GDP, which makes it all but certain that their public debt levels will keep increasing at a disturbing pace.

Hardly helping matters is the fact that both Brazil and South Africa have yet to bring their pandemics under control. Nor does it help that both are suffering from divisive politics that make it highly improbable that they will undertake serious economic reforms to address their public finance problem. The public debt to GDP ratio is around 90% indicating there is little scope to increase debt.

Conclusion

In the age of uncontrolled stimulus and rapid increase in debt, a currency crisis is not a distant possibility. To the contrary, some countries will see increased pressure on their local currency. Investors will have to monitor the same as the purchasing power loss coupled with increased inflation, interest rates and debt burden will be adding insult to injury.

- By Nishant Maheshwari and Vishal Vora

Disclosure: This article is for information only and should not be construed as a financial advice.

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317