A quick look across the commodities pricing for the past one year reveals an inflationary picture.

Source: Visualcapitalist.com

This will certainly seem a lot given the returns posted here. Given that we have been through a pandemic induced supply shock and now a war like situation threatening additional supply sources, it is a general expectation that we are in for a long ride of inflation.

Yet under the hood, things are getting interesting. For one, lot of backlog on the ports is now getting resolved. Input prices are rising faster than output prices while consumers tap their savings and max out their credit cards. Central banks all over the world are looking at taking away the punch bowl and coupled with low fiscal stimulus, it seems the market is in for a rough period.

Enter China. It has had a tough 2021 and the problems in the real estate sectors are nowhere near their end. The Winter Olympics held in China was a huge flop. Given that China had stopped a lot of production for the Winter Olympics one would expect them to start getting on feet especially after the Omicron hit. China has many issues on its platter. Real Estate and allied sectors forms 30% of its GDP. And property sales have been tumbling 35% plus for past two months year on year. The debt burden is still high for many property developers and debt market is frozen for most of them with even the best trading at 65 cents to a dollar. It also got dragged in Ukraine Russia conflict trying to pacify Russia while keeping its trade relations with the west intact and given that it has its own geo political ambitions with respect to South China sea and Taiwan in particular, it will be closely watched for its actions. On the economic front, the problems don’t end with the real estate sector. A sharp rise in commodities which China heavily imports especially food which is becoming increasingly difficult to find, lack of consumption demand from within the country, a currency that is still strong and neighbours that are trying to garner further market share are some of its problems. Particularly, its currency. Chinas yuan has been climbing steadily and this has made its exports expensive. Given its place in the pandemic and the resulting supply chain issues, many companies have sought alternative sourcing locations and therefore there is ample of competition in sectors like textiles, etc. Given that there are perceived risks to manufacturing in China and better alternatives emerging, China will need to review its currency peg and/or allow it to fall or slightly devalue it to bring growth back to its manufacturing sector. With its high leverage and high cost of goods, there is little scope to increase infrastructure investment that would meaningfully add to GDP. In 2015, even a 3% devaluation sent shivers down the markets and spread deflation through out the world. Yet a similar event can take place given that China has multiple problems rearing their heads and amid an inflationary setting, it would like to keep social stability as prime area of focus.

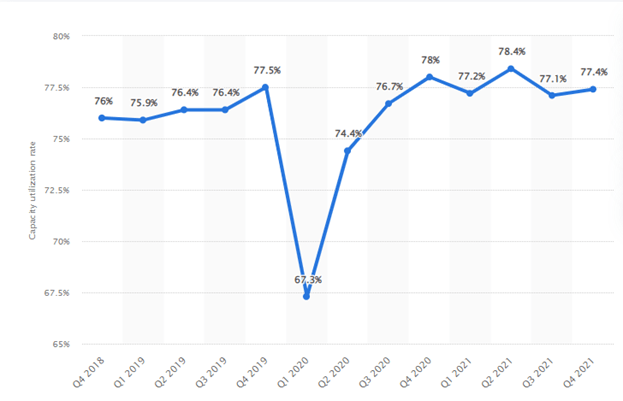

One more factor to analyze is Credit impulse data of China and Capacity utilisation of China.

This is industrial capacity utilisation clearly indicating the peak of event. Besides above due to real estate saga, the demand for cement, Steel and other Real estate material has decreased substantially. This is a kind of vacuum which the largest consumer of such materials has created at global level.

While prices of commodities have been looking at the supply constraints, one also needs to look at demand side. Given that the global economy is losing steam, it is only a matter of time before a correction takes place. Current geo political events may help prices remain high but it will kill demand and with the central banks forced to take steps to cut their market supporting measures, it is likely that stagflation turns into deflation very quickly. Till yesterday there was 0% probability for a 25 bps hike in March 2022 meeting now it is at 5% and may rise quickly if the yield curve bends further.

With Economy just getting back to normal (Still below 2019 normal), in come Central Bankers with timeline and Schedules for Quantitative tapering. Fed announcing full tapering before March 2022.Due to this squeeze of liquidity, we have seen emerging markets in turbulence even before the completion of tapering.

Globally people have developed the perception that the what is going in stock market is the real picture of financial market. To the contrary its vague assumption. The biggest market in this world is Currency market. Yes you read it right. It is currency market which is 11 times bigger than stock market and then comes your Bond market which is 5 times bigger than Equity market. The global financial picture is incomplete without Currency and Bond market.

What is happening at present and what is anticipatory?

As we all hear about market noises regarding inflation the Bond yields at present is indicating different picture. Yes you heard it right. The war between Ukraine and Russia and Sanctions on Russia added further supply chain woes to commodities like natural gas, Aluminium, Steel, Nickel, Wheat etc.

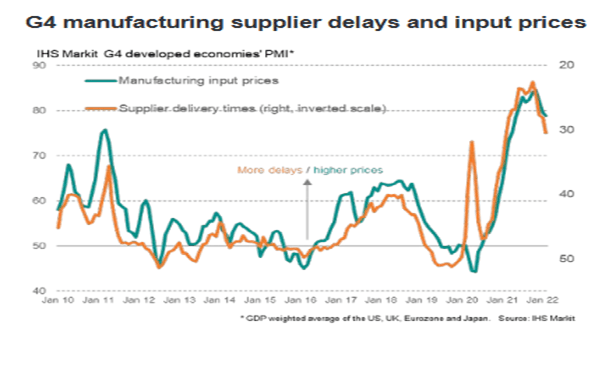

From market point of view, we are all anticipating further inflation fears but remember that all we have seen is supply side inflation till date. At present what Manufacturing supplier delays and input prices are telling? Let’s see it through charts.

From the above charts, it is very clear that the delivery period of supply is rapidly improving and input prices are on down side from peak. This itself stated that the demand side inflation was never present in market. We all know that market is always forward looking. The bond yields spiked much before the war and crossed 2% in US 10 year, while the war/ongoing invasion, we are seeing the Bond yields crashing like pack of cards. The German Bond yields which went to 0.24 from -0.83 and now back in negative territory (Yields crashing by 35% in a single day), or US 10 years Bond moving more than 2% and now again back to 1.75%. Many European yields have now been crashing.

What is being indicated by Bonds and currency is yet to be unveiled in future as the market is forward looking not concerned with present anticipation.

Post pandemic event, Q.E. was in full speed and with each coming year the central Banks Balance sheet expanding. Be it ECB or FED, none of them cared about future and considering pandemic situation provided full liquidity to market while keeping Interest rates at multi years low. With this liquidity and constant support of Central Banks, market have boomed in a very small time frame like from rock bottom to top of the mountain. But we need to see what is common between them. It’s the law of gravity. Jokes apart. Lets come into real analytical portion. All the liquidity created with all time low interest rates and supply squeeze helped to create huge inflation globally while Debt to GDP ratio of 90% of countries are now touching all time high.

Upcoming Currency crisis

Talking about above analysis and without correlating it with currency will be injustice. With ongoing war we all have seen Ruble plunging from 68 to 110 against dollar or before that we have seen Turkish Lira falling like pack of cards against USD or Currency crisis of Zimbabwe or Venenzuela or Argentina were well known events.

What will happen if China plans to Invade Taiwan?

Seeing the current stage of response of western world against Russia, it is very clear that Western Countries are not in a position to participate in war against Russia. Mere sanctions on Russia from Swift system that too excluding purchase of Natural gas won’t solve the problem. Russia external debt is 31% which is very negligible in comparison to the rest of world. Debt to GDP is 19% in comparison to US which is more than twice. So Russian Ruble falling will help flourish the exporters in long run as they are one of the largest owners of natural resources globally. Further any increase in prices of commodity will ultimately increase the asset value of Russia and the Gold reserve will ultimately provide buffer against all such crisis.

Due to this event, it will be very probable that China will become more courageous for its ambition to invade Taiwan and its activities have again started to provoke.

This is one of the biggest risks we see in financial markets. Forget about the war, think about financial side. Will the West impose sanctions against China if the above event were to happen? What will happen to the pegged currency in offshore Yuan rate? Is the world ready to see Yuan tumbling against dollar? What will happen to rest of the world manufacturing activity where China holds 19% share? When last time China devalued Yuan back in 2015 world market fell like pack of cards. This time it can be very alarming situation too. The capacity utilisation is low, so cheaper exports can drag down prices sending deflationary shock wave in rest of the world in humongous debt environment.

While everyone is focused on inflation, we see powerful deflationary forces waiting in the wings. It is said that the cure for high prices is higher prices. Central banks have clear paths but unpalatable choices.

Raise rates and burst the asset bubble they so dearly build the past decade or let the market price commodities even higher and cause stagnation before a deflationary event takes place. The bond markets are pricing the former.

Hello , You have Great Contents , Bravo 😉

Never Miss out this special offer

Thanks A lot

LikeLike

Greate post. Keep posting such kind of information on your

site. Im really impressed by your blog.

Hi there, You’ve performed a great job. I will definitely digg it and for my

part suggest to my friends. I’m confident they will be benefited from this website.

LikeLike

Thanks dear.

LikeLike