Whenever we speak about this yellow metal, a lot of the debates rage regarding its usefulness or the lack of it. Gold has been part of our daily lives for thousands of years. Been used primarily as an ornament material and for some centuries as a commodity money, gold has been the shining metal that everybody liked. But a few years back, gold was losing its mojo especially during the economic boom of 1980 to 2000.

There are many loosely held conceptions of gold. Some think it is a lousy investment. Others argue it doesn’t have value as it doesn’t yield anything. Most people agree that it works well in inflation but doesn’t work well in deflation. There seems to be general agreement that gold works well in times of uncertainties and fear (we live in one of the most peaceful times in earth’s history). Yet when we look at it, the demand for the product remains high. As per World Gold Council, gold backed ETFs have seen their holdings and assets reaching new all-time highs and the assets in global gold backed ETFs have grown nearly 50%. So why is the demand for gold so high?

Separating wheat from the chaff

First, we will deal with why many people fail to really understand gold.

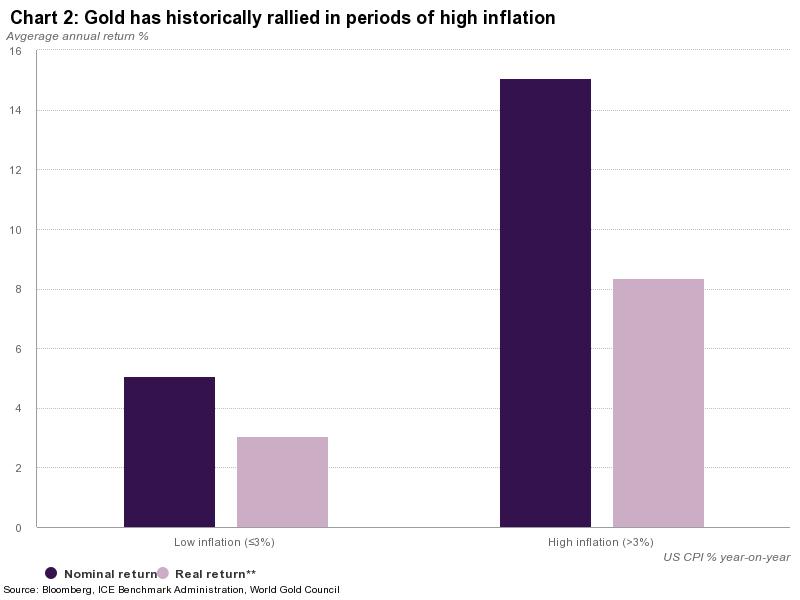

Source: World Gold Council, Investment Case of Gold, March 2019

This chart is taken from World Gold Council Report March 2019. As we can see, correlation with inflation is strong only in times when inflation is high and low when inflation is moderate or lower. But gold has done well even in times of deflation as suggested by repricing of gold in dollar terms from 20.67 dollars per ounce to 35 dollars per ounce in 1932.

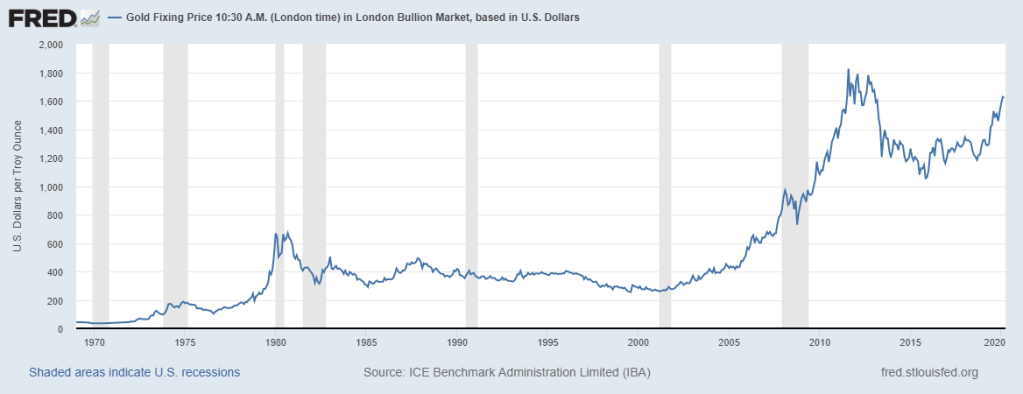

The other common understanding is that gold rises during times of uncertainty. When the economy was going through a recession in 2008, gold prices fell 30%. Gold had fallen from 1980 to 2000 but has also risen from 2000 to 2020 and both were equally good times for global economic growth.

Source: St Louis, FED

Source: https://snbchf.com/2017/02/bhandari-india-fastest-economy-2/3-india-china-gdp-comparison-png/

Source: St Louis FED

So, what really gives gold the reason to rally in the current times? Historically, gold has always been a commodity money. And being a monetary metal priced in other currencies, it has always competed with other currencies. Whenever the price of the underlying currency has fallen in value either through inflation or loss of purchasing power due to increased supply of underlying currency, gold has risen. It is not so much as gold rising but the currency falling that is priced inversely. Hence gold acts as a hedge against fall in value of the currency. While small loss of value in currency may not have significant effect in the short term, it is the cumulative effect over the long term that is dangerous for wealth creation for an individual.

Source: World Gold Council, Investment Case for Gold, March 2019

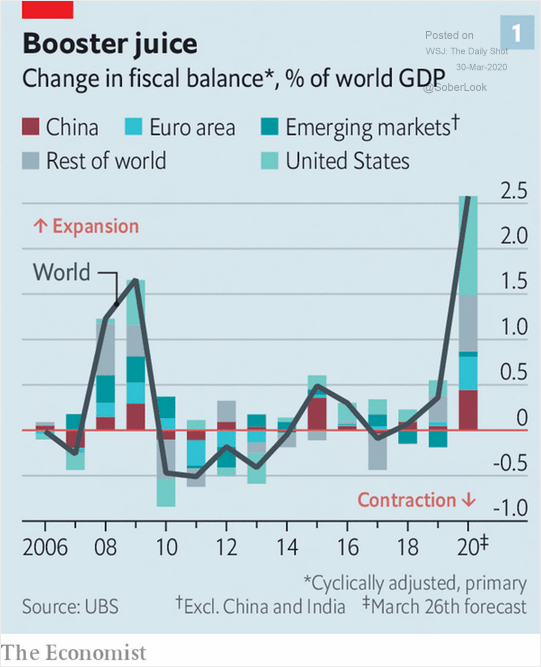

It is common knowledge that fiat currencies lose value over time. But the problem is aggravated if the fall in value of the underlying currency occurs over a short to medium term. Do we see such a possibility? While the current scenario may be a bit distorted due to the pandemic, we do see a significant stimulus based economic activity. Currently every country needs to announce stimulus either fiscal or monetary due to pandemic. There are wide range of estimates about the quantum of stimulus but they are typically between 4 trillion dollars to 10 trillion dollars.

Source: The Economist

As discussed in previous articles, with wages staying stagnant and prices of essential goods and services rising, the ability to save has been low. This has increased the debt burden on the consumers and there is limit to increasing consumption beyond current levels. This has forced government to increase spending without increasing debt levels to keep growth stable. However, this process has to be repeated year after year with increasing debt and reducing interest costs with lower interest rates. This makes the system vulnerable to external shocks. Therefore, when things like natural disasters, war or pandemic strike, there is no option but to save the failing corporations and distressed consumers as is happening currently.

The only way this can be done is through printing more money and putting it in the hands of the consumers and businesses to operate. This reduces the purchasing power as more money chases constant number of goods and services. It can stoke inflationary expectations. Fear about the future increases and propensity to save to retire debt will be at it’s peak which will force further decrease in consumption thereby affecting the GDP growth. This process can only be solved in two ways: either let the system clean itself or continue the low growth environment. Both are difficult choices for populace but for those in power the former is an even difficult choice.

The above process highlights why gold becomes necessary in such a condition. As debt burden increases, the need for stimulus either fiscal or monetary increases from time to time. To keep the narrative going, there is a constant reduction in the purchasing power or increase in the debt which further leads to the process repeating. Gold acts as a preservative of purchasing power against the underlying currency. Hence you will find that gold is making new highs in almost all currencies except dollar. The only reason the dollar is strong is because the other competing currencies have far weaker economies and they have dollar loans to pay increasing the demand for dollar. Besides, other governments don’t want a strong local currency as it reduces their export competitiveness.

So, what does the future hold for gold? While the dollar will remain strong given the factors discussed above, the constant stimulus and the declining growth prospects indicates the strength in gold is here to stay. Even if the world escapes the depression, the confidence in the economy is faltering and global growth will not be the same again. Hence our bet is that gold will continue to outperform the next decade until the problems of the current financial system are resolved either through pain now or later through forced austerity.

Gold is more of an insurance against the central banks’ policies of increasing money supply through stimulus measures.

Gold as Safe Haven

The total world gold market is greater than 7 trillion dollars and it is highly liquid as large number of transactions happen in physical and paper form. This makes gold as a hedge against liquidity events when markets break as it can be used as a pristine collateral demanded by banks. Because gold in physical form is free from counter party risk, it makes sense to have a small part of the portfolio in gold to have liquidity in case of systemic risks. Besides it has lower volatility as compared to risk assets which is useful when volatility shock causes risk assets to swoon.

Demand for Gold

Much of the demand for gold is currently coming from central banks. As per the proposed BIS rules, Basel III, physical gold bullion was to be on par with cash and sovereign debt instruments (Basel III has been postponed till 2022). Banks have been buying gold as part of their tier I capital needs as interest rates are negative in large parts of the world and gold provides them buffer against reserve rates charged by the central banks in negative rate regime. For the first time since the dollar went off gold standard, central banks accumulated more than 640 tonnes of gold in 2018. Much of the demand is from Russia who has sold its treasuries and bought gold to defend its currency against USA sanctions and China that is also looking at diversifying from US assets. Many other central banks in smaller countries are now increasing their gold holdings anticipating risk events. Besides repatriation efforts have increased as counter party risks have increased in current environment.

Source: World Gold Council, Bloomberg

Conclusion

So, while the investment case for gold may not be as strong, it is required as a hedge against loss of purchasing power in today’s stimulus dependent world. There is no guarantee that stimulus-based measures will stop in future and as such a constant threat of loss of purchasing power exists. Gold is an insurance against that threat. Hence a small portion of one’s portfolio should be allocated to protect against fall in risk assets. Most of the investors frown on gold. Yet, it is one of the best performing assets YTD and is up 52% since it’s bottom in 2015. Probably it is one of the best neglected assets. Got Gold?

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting their financial advisers.