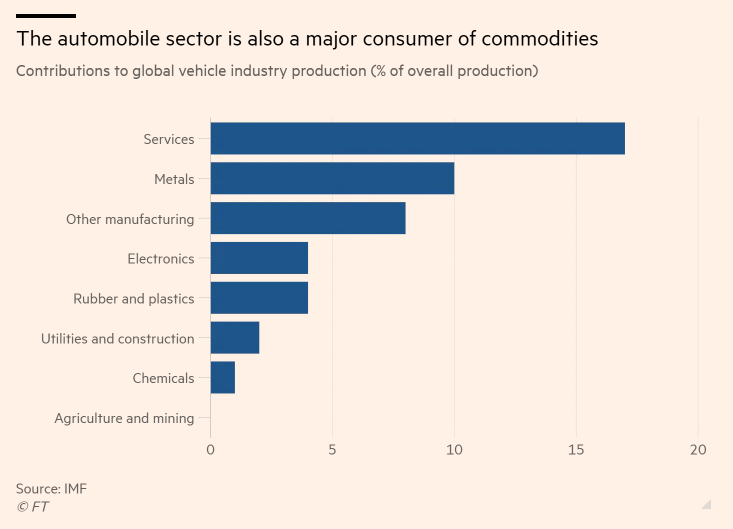

It is hard to escape the influence of Automobile Industry on Global economy. The impact of the auto market goes deep, with long supply chains and large consumption of raw materials like steel, iron, aluminium, plastic, glass, carpeting, textiles, computer chips, rubber and much more. In fact, the automobile industry is home to millions of jobs. According to statistics, about half of the world consumption of oil, rubber, about 1/4 of the glass output, and 1/6 of the steel output is accounted for by the automobile industry. In the economy of developed countries, growth in the automotive industry by 1% causes a GDP growth of 1.5%. Indirect impact of the automotive industry on GDP is strengthened through related industries, provided by orders from the automotive industry. The chart stated under reflects the contribution of Automobile Industry to various sector:

Source: IMF

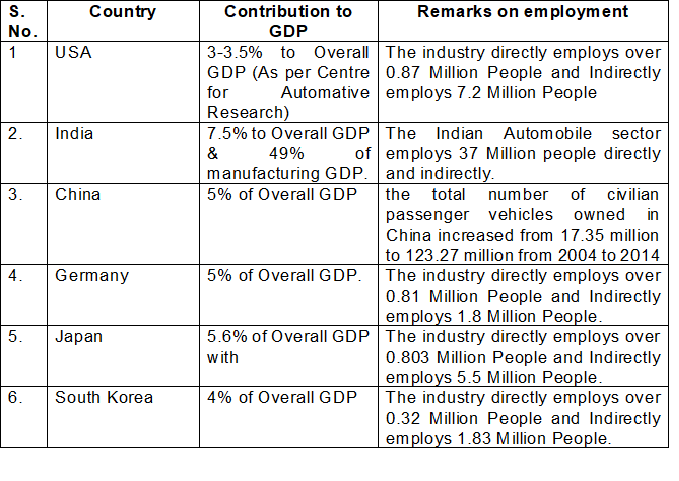

Before starting with causes of slowdown in automobile sector, let us emphasize on contribution of Automobile sector to GDP and employment globally:

Source: As per International Organisation of Automobile Manufacturers

It is always believed that like MACD indicators (where the early rally or plunge in stock is estimated as lead indicator), automobile sector growth or slump has worked as lead indicator of growth and slump in economy.The chart below reflects the real picture of Automobile sector globally:

Source: As per International Organisation of Automobile Manufacturers

From the above chart it is visible that the Automobiles sales numbers peaked in first quarter of 2007 and the second quarter reflected as lead indicator of slump in economy. Similarly, in mid of 2017, sales were at peak. Thanks to China which safeguarded the numbers from 2010 to 2017.From mid of 2017, a downfall is visible in the charts which indicated the slump in economy. However, the market got stretched longer till end of December 2019.

The production statistics for 2019 with YOY % increase or decrease is as under:

Source: As per International Organisation of Automobile Manufacturers

Main Cause of Slump in sales of Automobiles Globally:

- Plunging Demand

Trade tensions between US and China since 2018 shook confidence of Chinese. Although the Chinese economy was slowing down, the trade tensions accentuated it. Big giants like Jaguar Land Rover reported poor performance since 2018 on account of poor Chinese demand. Similarly, Ford also pulled plans to sell a Chinese made Ford vehicle in US due to impact of trade tariffs. Due to Brexit, investment in U.K. Car industry has fallen massively as British car plants rely heavily on components imported from EU, while most of the cars produced are exported to European mainland. No deal Brexit in previous years resulted in massive plunge in demand on account of uncertainties in the form of tariffs.

- Emission Issues & Taxation Concern

In Europe, air quality concerns and taxation changes have led to the big slump in diesel sales resulting in substantial plunge in new car registration in Europe since 2018. Introduction of new CO2 emission standards make it much more expensive to build a car. From 2021, manufacturers will face big fines in European Union if their fleet break agreed emissions limit. It is believed that carmakers will have to add on an average 1000 Euros to comply with those standards. This has shaken the confidence of consumer to buy cars in Europe.

Tax hike in Japan has also resulted decline in Auto sales after three years.

- Shift of Ownership

The emergence of fleet companies like Ola, Uber, Meru, etc has radically changed the mindset of user from owning a car to taking car on rent with reasonable rates and opportunity cost. The cost of travel per mile has been slashed due to emergence of such model which made ownership of car less appealing. The traditional car companies are having to fight to stay relevant as technology giants Waymo dive into this market. These models appeared as boon to industry when massive demand was created by these unicorns. But after certain time, it has resulted into bane for automobile industry.

Further, if driver less cars go mainstream over next few years then many people will opt to share or rent rather than owning a vehicle.

The fear of such model has forced companies like Ford or Volkswagen to investigate ways on electric and autonomous vehicles. Similarly, Honda invested $2.75 Billion in rival General Motors driver less unit with a view to launching a fleet of unmanned taxis.

- Headwinds from China

The Chinese auto sales saw 20 consecutive months on month declines. China’s deleveraging program has tightened credit for prospective buyers and a slowing economy has hurt consumer sentiments. The central Government subsidies for Electric Vehicles were slashed by 45% to 60% and subsidies for Electric vehicles with range of less than 250 miles were eliminated altogether. Further for clean Blue-sky policies, the new emission regulations i.e. China 6 standards kicked in from July, 2019. This has resulted into increase in cost of vehicles resulting in lower sales. As pointed in point no. (1), the trade war was having significant adverse impact on consumer sentiments and was one of the key reasons for plunging automobile sales.

- Electric vehicle

In order to reduce the level of emissions, the automobile industry is making a shift from the legacy of fuel-based vehicle to electric vehicle.The industry is going to sell more electric vehicles in future, but there are many obstacles in the way. Global sales of battery based electric cars surged to peak at 1.3 Million units registering massive 73% growth in 2018 but its just a fraction of overall 86 million car sold in 2018. Now, these numbers are falling, and electric car sales are reducing due to lack of significant incentives. But with the introduction of this electric vehicle concept, the intended buyers are in real dilemma of owning car. On one side, they intend to buy these electric cars but refrain on account of cost. On other side, they don’t see value in buying the fuel-based cars.

- COVID 19 impact

As the COVID-19 crisis drags on, the pandemic’s economic impact is very much visible on vulnerable Automobile industry. The automotive sector is among the industries most exposed to the negative impact of the virus. Previously due to prolonged lock down in China, Chinese production suffered a significant hit which has resulted in production outages to many manufacturers around the world who rely on Chinese parts. And now with extended lock down globally (Excluding China), the automobile industry in China is also suffering with fall in global demand. China is among the world’s largest suppliers of car parts, exporting motor vehicle parts and accessories worth $34.8 billion in 2018, according to the UN’s Comtrade database.

Source: Statista, UN Comtrade

Further with lack of sales from Global market due to lockdown, the major giants like Ford Motors, Tata Motors, etc can see multiple downgrades in ratings which will result in expensive borrowing costs. With lack of cash flows on account of negligible sales, it will result in risk of going concern for these companies.

It is also felt that increased debt burden on the consumer has also played a role in reducing demand. As consumers levered on more debt, their credit rating has come down and default rates among sub prime borrowers is now reaching 2008 crisis levels.Cheap financing has brought demand forward but it seems demand has reached a peak.

Scenario of Indian Automobile industry

The industry is one of India’s biggest, considering it employs some 35 million people, directly or indirectly, and contributes more than 7% to the country’s GDP. From the analysis, it is visible that if we own petrol or diesel vehicle in India on loan basis, the cost of ownership per km for 8 years is Rs 24 per km for Diesel car and Rs 22 per km for Petrol car which is relative in terms of number of kms you drive your car (for smaller distances up to 30 km/day). This shows that ownership costs are increasingly becoming a factor in determining whether owning a vehicle is better as compared to renting or sharing rides.

The Indian Automobile Industry saw its golden era with huge spurt in demand before 2019. The major factor which contributed to the industry is demand from Tier 2 and Tier 3 cities along with the financial sector giving auto loans with low down payment. In addition, the ambitious infrastructure spending which central Government undertook on account of reduced crude prices and hiked taxes. This helped them to float huge infrastructure tender year on year basis. The debt of NHAI inflated from 44,567 crore in 2016 to 1,78,867 crore in 2019. The major portion of this debt is attributed to land acquisition. This is turn resulted in sweet fruits to automobile industries too. Small chunks of amount received from compulsory land acquisition resulted in buying of premium cars or small segment cars depending on the amount of compensation on land received in Tier 2 and Tier 3 Cities. Enhanced portion of compensation further helped automobile industries to get demand from Tier 2 and Tier 3 Cities. Then came the demand from ride hailing industries like Ola,Uber, Swiggy, Zomato, Food Panda, etc which increased its presence on PAN India unprecedentedly. e.g Uber buying 2,00,000 cars from Maruti with a whooping investment of 2600 crore. It helped the industry with huge spurt in demand. However, post capex of these ride hailing industry or delivery distribution companies and spurt in petrol and diesel cost (which resulted in decline in floating of Infrastructure project) resulted in decline in demand from Tier 2 and Tier 3 cities. The demand from Tier 1 cities was already declining since past few years and post Ola and Uber,the dilemma of people completely shifted from owning a car to taking car on rent.

Further with the introduction of BS-VI emission norms, the industry is forced to do capex of multi billion dollars to comply with the norms.

Now what changed the mindset of owning car in India?

As discussed above, ownership costs, opportunity cost of driving vs hiring a car ride,the comfort of ride hailing technology along with BS-VI emission norms and EV vehicles have confused the willing buyers to refrain from owning car. The additional cost impact on the industry will be huge considering the capex done for BS-VI. This increased cost burden will ultimately be passed on to the customers which will make the vehicles further expensive. If customer opts for BS-IV, then fear of judicial pronouncement with respect to life of vehicle can give set back to intended users. Whatever measures government announces to liquidate BS-IV vehicles, it will not help to boost confidence of intended buyers.

Therefore, we see automotive industry declined for the 17th month in a row in March (leaving festive season which is not comparable).

As a result, more than 100,000 workers, many of them contractual, have lost their jobs so far as per some estimates. Now post corona, fears are rising that forced lower production will result in more job cuts in upcoming months.

Future Outlook

Before the Crisis, the global automobile industry saw a sharp slump in sales due to sharp fall in consumer demand. In fact, there were many instances where production halts were visible in September or October for few days.

As the sector was heading for major slowdown since last few years, after the crisis the situation is expected to further deteriorate. Even during the crisis, we have seen companies deferring the payments to vendors or giving OEMs (Original Equipment Manufacturers) to get payment from Banks on Letter of Credit(LC) basis. If debt ridden OEMs opt for such option, then the margins will further shrink resulting in solvency problem. Further, dealers of Automobiles will vanish if such crisis continues for a longer period as interest on the working capital of these dealers will cause huge dent in their margins. The ratings of debt-ridden OEMs globally will get revised lower resulting in expensive cost of funding. In recent times, we have also seen downgrading of ratings of some established players with high debt. This scenario is very precarious and may result in stress on balance sheets of big giants.

Further with fear of job loss post Corona crisis, people will shift the mind set of considering Vehicle as necessary item to discretionary item. The main emphasis will be on savings. With plunge in earnings of existing vehicle owners, we can see defaults in repayment of EMIs to a great extent. This will result in invocation of hypothecated vehicles by Banks. Thus, the same will be flooding the market reducing prices of used cars further and thereby affecting demand for new cars too. While interest rates may come down, banks will be reluctant to lend to consumers with low credit scores.

At last, we conclude that the current scenario is not at all favorable for the industry considering the domino impact of disruption in supply chain and the automobile industry needs some magic stick to get itself back on track. If the demand is not revived in coming months (which is most likely scenario) then we can see increase in inventory of these companies and dealers with few willing buyers. This will be biggest risk for industries connected directly or indirectly with automobile sector.

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors. The article is published in ICAI Journal in June 2020 edition and the rights are reserved with ICAI.

Excellent analysis…. Thanks

LikeLike

Good data analysis..👌👍

LikeLike