Asian economies have generally been a manufacturing base for most of the European & American consumers. China, Japan, South Korea, Thailand all have significant contribution of GDP from the manufacturing sector. India, on the other hand, generates 60% of its GDP from the service sector. Manufacturing has been stagnating in the range of 13% to 18% for the past sixty years. This is low compared to 27-29% seen in China, South Korea and Thailand.

Percentage contribution of Manufacturing sector in India’s GDP

Source: World Bank Data

Given that this democratic country has a significant demand generating population, it was always felt that India should try to increase its manufacturing base. An increase in manufacturing base will also lead to multiplier effect in service sector growth. However, in spite of many reforms taken throughout the decades, India has never been able to significantly increase its manufacturing share in the GDP.

India has a significant labour pool with more than 60% population below 35 years of age. Every year, more than 10 million people join the labour force. Thus, a strong labour force would need significant new job additions every year to the economy. While service sector has been bearing this burden for a long time, its growth rate is slowing down and is not enough to alone handle such burden. Agriculture faces a hidden under employment problem. Besides, it depends on the forces of nature with low ground water reserves.

There have been many factors leading to anaemic manufacturing growth. Land Acquisition, Labour laws, access to cheap capital, skilled labour, global competition and subsidies distorting trade, tax structure and taxation laws, logistics and infrastructure have all contributed to manufacturing activity remaining stagnant for past few decades. Some steps have been taken to alleviate these problems but they are incoherent measures without a common goal and big picture problem resolution. Much of the manufacturing happens in small scale industries as labour laws prevent firms to go big. There is no hire and fire policy after a factory attains size of 100 or more workers. The number of laws governed by both central and state is too cumbersome and difficult to maintain. Recently, the pandemic has forced the government to act on reforms and many labour laws have been merged. Skill India and start up India are some of the programs that have shown promise. India has also opened many sectors for Foreign direct investment. Tax rates have been made competitive due to reduction in tax rates by 5% or income exemption under section 10 of Income Tax Act or weighted average deduction under section 35 or Deductions available for various business under section 80 I of Income Tax Act 1961 or various incentives to exporters in Erstwhile Central excise and right now under GST. While these measures are necessary, they alone were not sufficient enough to generate the necessary manufacturing culture in India.

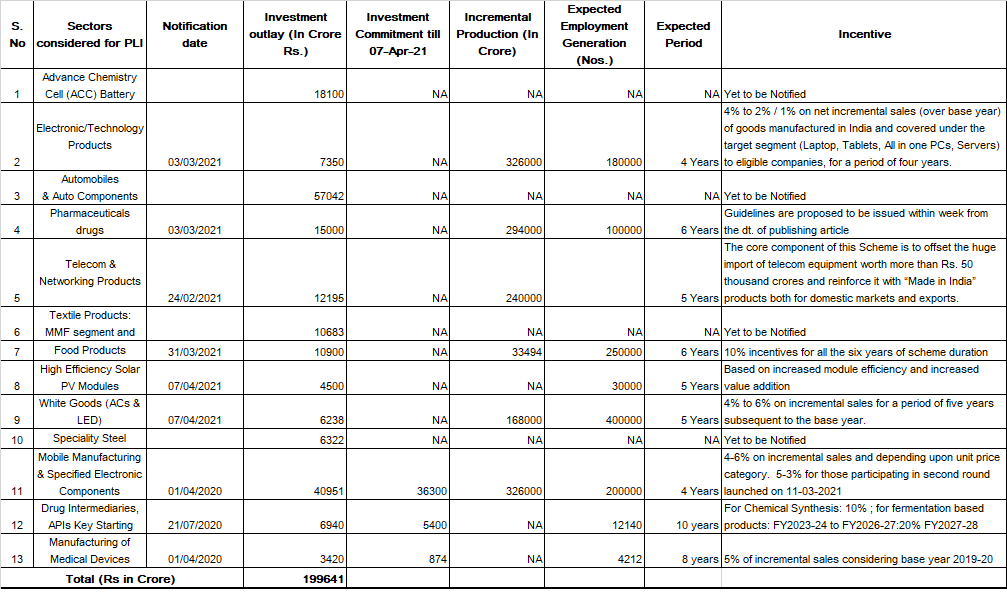

In this article, we are looking at one of the policy that the government has brought out to change the manufacturing culture in the country- the Production Linked Incentive scheme. Under this scheme, 10-13 sectors and subsectors have been selected for non-tariff-based incentives to increase production and cater to export and local demand. The policy comes at a time when there is significant interest in widening supply chain base among foreign corporations and increased local demand after the pandemic leading to increased capacity utilization with expectation of government support and further policy reforms.

The following sectors and sub-sectors have been selected for the production linked incentive scheme (PLI)

- Large Scale Electronics Manufacturing

Phone Manufacturing,

Specified Electronic component

- Telecom Equipment Manufacturing

- Textiles

- Specialty Steel

- Automobiles and Auto components

- Food Processing

- Solar Photo voltaic panels and components

- White Goods Electronic manufacturing

- Pharmaceuticals and bulk drugs

India has always tried to increase capital intensive manufacturing in sectors like steel and heavy engineering. However, the focus is now to increase value addition in new fast-growing sectors with labour intensive nature of manufacturing. While most of the products in these industries have been imported, the policy tries to increase and capture value share in the supply chain and hence reduce imports while also catering to exports market. For e.g., value addition is expected to increase from 20-25% to 35-40% for mobile phone and components manufacturing, from 20-25% to 75% for AC, 40% to 70-75% for LED, from 5-10% to 20-25% for IT Hardware by 2025.

Source: MOSPI, PIB

As can be seen from the above table, a significant amount of money has been allocated for the scheme. Judging by the optimism, it is expected that the scheme may see better implementation as there is much more clarity and objectivity in the scheme. Besides, it insists on non-tariff subsidies which is WTO compliant and it is easy to calculate the savings arising out of the policy for those who wish to set up units. In addition, the timing of the policy is essentially helping the implementation of the policy. Globally, many MNC and big corporations are looking to diversify their supply chain after the pandemic. While the initial movement was towards Vietnam and Thailand, the policy is now helping global multinational companies to set up shop and cater to the local demand easily.

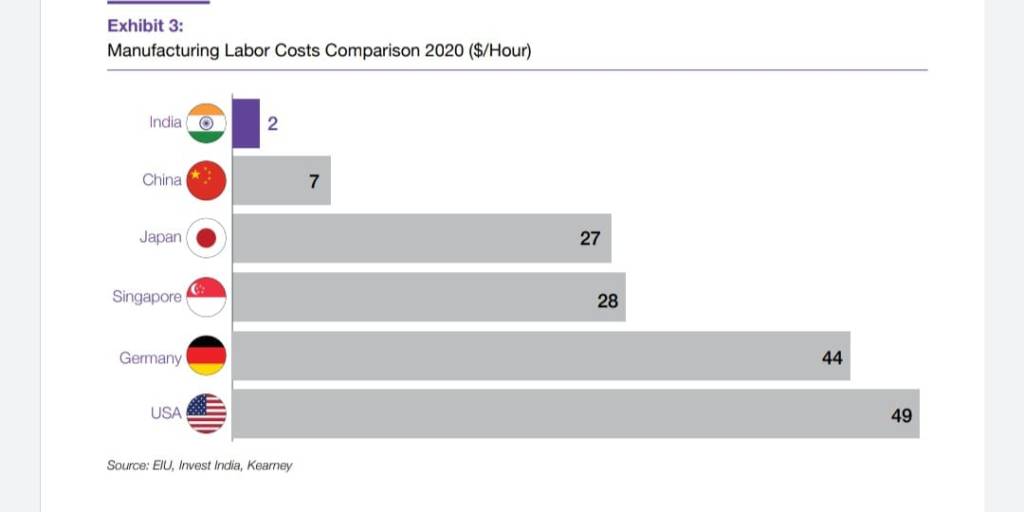

However, there are many factors that will need to be addressed. Take for e.g. Labour. While India has a lower labour cost as compared to China, its labour productivity is also lower than China.

Source: Rabo Bank

In spite of the fact that India has a much lower labour cost, the total production costs are much higher given the deficiencies in logistics and infrastructure, power availability, etc which adds gross value addition to the product. The economies of scale in China is far ahead than India.

China is rich in materials and the cost of production is lowest in most sectors. Take an example of Mobile Manufacturing. Most of the rare earth metals are found in China and China exhibits strict control on its exports. India ranks lower in Global Competitiveness Index and ease of doing business than China. Not to mention infrastructure and logistics issues, tax laws and corruption issues, research and development spending. Hence, it makes much sense to make in China and import in India. China has now progressed from designing to fabrication of chip while India is looking for global corporations who are willing to set up shop in the country and is ready to offer significant incentives too. Yet, such manufacturing is difficult to set up for multiple reasons- availability of skilled labour and supply ecosystem for components been other factors. Hence, such manufacturing will take time to set up and can be done only in incremental steps. As we try to increase the value chain that gets captured locally, more players will try to bring their technical know-how and capital investment in the sector. The government will however have to take steps to increase productivity and carry out land and labour reforms. At the same time, government will have to reduce custom duties and tariffs on raw materials and other finished goods. Recently, the government has increased customs duty on automobile components, mobile tempered glass and solar PV modules and PV cells. This will raise cost of production and while it provides the scheme beneficiaries confidence in investing, it raises the product price and makes the industry globally uncompetitive. Another area is that the policy is looking at incremental sales rather than incremental volume which would have been a much better indicator of production growth.

Previously, state governments have tried to provide capital subsidy and land for projects. Multiple MOUs were announced for projects and those made big headlines but there was little in terms of implementation. However, the pandemic has created a big hole in government finances and increased the debt substantially. To stop the rot and prevent the debt to GDP ratio from increasing substantially while keeping the economy growing, bold reforms were needed. Some steps have been taken but providing a boost to manufacturing in India will go a long way to help increase employment in the country. After all, every year more than 1 crore people are getting added to the labour force. The young population needs opportunities and not freebies from election or politics. Boosting growth is the only option left. There is a massive opportunity given the global supply chain shock. With DFC progressing, infrastructure improving and GST stabilizing, there is a stable environment for growth. Corporate India should take the same with both hands.

- By Vishal Vora, Nishant Maheshwari

Disclaimer: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.