The global markets are on a high given the fiscal stimulus and central bank profligacy. Since March 20 fiasco, market is making daily new highs in less than one and a half year without caring about the events looming all around the globe. During this euphoria, certain markets too have entered into bearish zones. But the overall rejoice remains unaffected and at global level, the indices are in the spree to make all time highs. For last 8 months, no major correction has happened and phases of upward trend continued to march towards infinity irrespective of the slow recovery path of economy globally, burgeoning inflation numbers, slowing credit growth etc. However, since the month of June 21, certain credit events have risen globally whose potential domino impact is worth to be analysed. So let us analyze those Global events in detail:

Evergrande Potential defaults (Lehmann Moment)

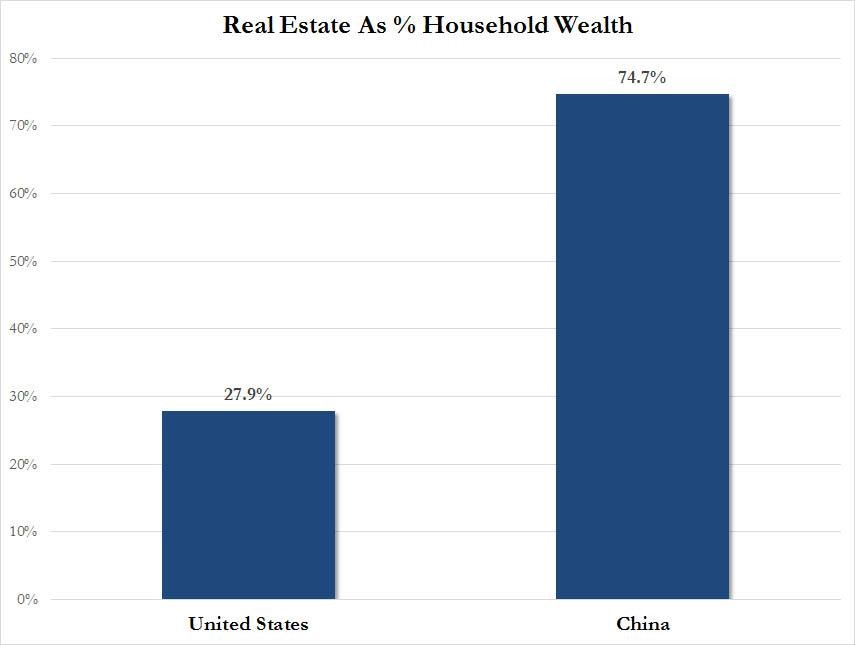

Before starting the effect of Chinese real estate, we came across a chart which is worth to ponder.

Real estate is a key driver of Chinese economy since last decade. The constant soaring housing prices provoked people in China to even hold 3 to 4 houses per family. The best part about real estate is the consumption effect and credit expansion. Real estate is major driver for more than 60 industries like Cement, Steel, Chemical etc. Further it enhances the credit expansion in the economy. The loans given to buy those real estate results in credit expansion which ultimately enhances the cycle of economy with constant rotation of money.

China’s housing bubble currently reflects the one in U.S. housing in the 2005-2008 U.S. property boom, where at a point of time $900 billion a year were being invested in residential real estate. In last 12 months, about $1.4 trillion was invested in Chinese housing. The total value of Chinese homes and developers’ inventory touched $52 trillion in 2019, (according to Goldman Sachs), which is twice the size of the U.S. residential market and exceedingly even the entire U.S. bond market size.

In March 2021, 288 apartments in a new Shenzhen property development sold out online in less than eight minutes. A few days later, buyers snapped up more than 400 units in a new housing complex in Suzhou. In Shanghai, apartment resales neared a record high in April, by one estimate. In the month of May 21, nearly 9,000 people each put down a deposit of one million yuan ($141,300) to qualify to buy apartments in a Shenzhen development. Imagine the kind of Euphoria created in Chinese real estate market. With the fears of Global slowdown, Chinese middle class started considering real estate as safe heaven. But like with every rose, thorns are always attached, the same scenario started into nightmare. The initial data released in 2018 stated that more than 50 million apartments were vacant in China and out of those vacant homes, roughly 21% were from Urban cities.

Since then, the number was only increased, and according to China Household Finance Survey, there are now 65 million empty units. Among families who owned two properties, the vacancy rate reached 39.4%, and among those that owned three or more, 48.2% were empty.

The record number in vacant units has meant little upward pressure on rents; in fact, Chinese rental yields are below 2% in major cities like Beijing, Shanghai, Shenzhen and Chengdu.

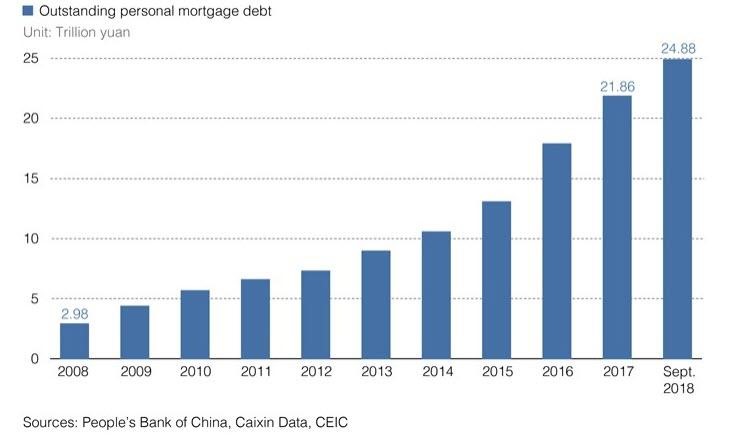

But as the year went on, the debt size on such notional appreciating property resulted into debt trap.

The size has reached to $4 trillion (approx.).

This was followed by the Chinese Government’s stringent action against Real estate market which acted as a pin to prick the bubble.

China’s push to wean property developers from excessive borrowing is spilling over into loan losses at banks and pain in credit markets as cash-strapped builders fall into distress, raising the risk of fallout rippling across the economy. Debt and land-buying curbs and hundreds of new rules are hitting developers far harder than they had expected, setting off a scramble to sell assets as well as a steady drumbeat of bankruptcies, defaults and cut-price takeovers. The regulatory push is the latest in years of efforts to reduce risks in the real estate sector. Let us look into some famous real estate Developers and the size of Liabilities.

| Sr. No | Name of the Company | Liability Size (billion dollars) |

| 1 | China Fortune Land Development (Defaulted in January) | $60.70 |

| 2 | China South City Holding Limited (Bond yield 42%) | $10.20 |

| 3. | Yuzhou Group Holdings Company Limited (Bond Yields 11%) | $21.50 |

| 4 | Sichuan Languang Development Co Ltd (Bond yields 35.40%) | $30.70 |

| 5. | Evergrande (Rating downgraded to potential default) | $304 |

| 6 | Central China Real Estate (Bond prices crashed to 68 from 100 in January) | $23 |

| 7 | RiseSun Real Estate Development (Bond prices crashed to 59 from 100) | $36.40 |

| 8. | Sunshine City | $7.20 |

| 9. | Fantasia Holding Group Co Ltd (Not being accepted as collateral as on date) | $12.90 |

| 10. | Guangzhao R&F | $51.40 |

| 11 | Poly Properties | $166.33 |

As Evergrande has been downgraded by Moody’s and Fitch, the contagion risk is visible to whole of Chinese credit market. Further, the settlement mechanism of most of the real estate developer is though giving underdeveloped properties to get rid of liabilities as on date.

The potential risk of these event is rising NPA in Chinese real estate loans given by Bank. To cover the liabilities, these companies will look for distress selling of properties which will create massive problem for Banks who have provided loan based on security of property as collateral (Which is under construction). The real estate developers onshore and offshore Bonds along with Banking Loan (Secured against project). The biggest joke globally is the under-construction property bought by Individual on Secured Loan basis. On the other side the real estate developer is securitising its project to obtain those loan. So, on one property you have two loans (Under construction and land & Project). So, in case of Default what Banks will get that too at distressed valuation.

How will it impact Germany?

Germany exports more than 10% of its goods to China which is estimated to be around Euro or 118 billion. One of thr major chunk of revenue is from the Machinery supplied for real estate sector and manufacturing units. Any failure of chinese real estate will have large effect on Germany. While the Euro zone is already in trouble, Germany holds the strongest position in Euro Zone. Germany Debt to GDP is already at 70.25% i.e. all time high. So further turbulence in GDP will again force them increase their Debt to next level. This will also lead selling off the Bonds of Germany.

How will it impact Australia?

Being rich in certain natural resources gives extra edge over others. Australia is very rich in Iron ore reserves and China is world largest consumer of Iron Ore. Iron ore is the key element used in manufacturing of Steel. With crackdown in real estate market in China, more than 60 industries (Steel, Cement, Aluminium, chemicals, etc), impact at one of the biggest level will be on Australia. Chinese crackdown on real estate will drastically reduce import of Iron Ore from Australia and further education and Travelling sector in Australia will also suffer. Major source of wealth in China is created from Real estate. Now if the property market sees crackdown, then the Chinese cushion to send children to Australia for education will be over.

Effect on Bond Market?

China Holds $1.1 Trillion Debt of U.S. In order to meet out onshore dollar bonds liability they can have two options either to sell those bonds and generate dollar or devalue Yuan to meet out liability through this reserves. Both the options are bad for Global market. In both cases Japanese will have to closely observe the Bond investment as they are largest holder of US Bonds.

Effect on Reverse Repo?

The reverse repo size is now in Trillions for last many days. With contagion effect of Chinese Real Estate developers’ loans and suspension of various Bonds to be accepted as collateral, shortage of Bond will be visible. So, the size of Reverse Repo will increase further as money market managers already demanding large amount of short-term treasury at one end and foreign bidders will further enter into party for meeting out its collateral requirement from Fed.

Conclusion

China’s move towards crackdown on various industries is like a needle pricking this giant bubble. Though it’s the start of wealth destruction with a move to reduce inequality gap. But the bubble is decade long so it’s very early to say that we are in mid of crackdown. Chinese dominance globally in manufacturing industry was adding real value to GDP but inflating GDP through fake notional hyper valuation of real estate resulted in giant bubble in the Ghost city. Now the time has come to self destroy this bubble in order to think forward for real value creation. As the world is rotating in credit creation, China is moving towards real resource value addition in the near future.

-By Nishant Maheshwari, Vishal Vora

Disclosure: The views expressed are those of the writers’ and should not be construed as a financial advice. Please consult your financial advisor before investing.

When someone writes an рost he/she mаіntains the idea of a user in hiѕ/her mind that how a user can be

aware of it. Therefore that’ѕ why tһis paragraph

is outstdanding. Thanks!

LikeLike