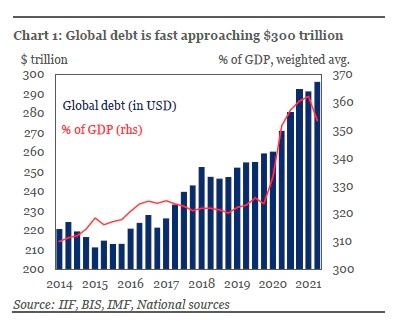

We all know that major world economies are roiling in debt. Recently published figures indicate the global debt has reached 296 trillion dollars in the second quarter of 2021 (IIF Global Debt Monitor Sept 14, 2021). Debt to GDP ratio is now around 350%. What is interesting is that from 2014 to 2020, the Global GDP has risen from 79 trillion dollars to 85 trillion dollars while the outstanding debt has risen from 199 trillion to 296 trillion dollars.

Source: World Bank

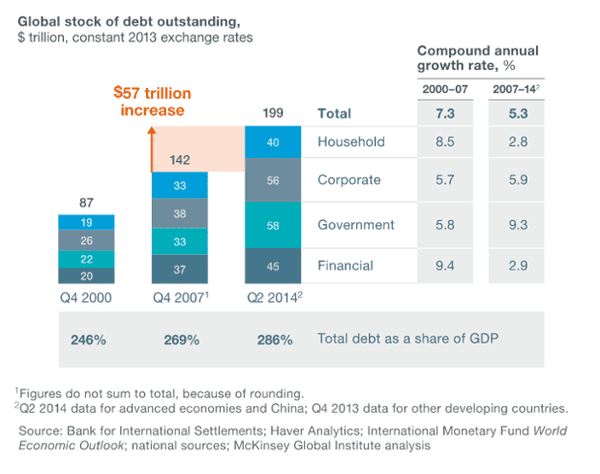

Source: IIF Debt Monitor July 2020

What it indicates is the reducing utility of debt to create GDP. Hence, we find two of the largest contributors to GDP, the USA and China struggling periodically from debt and deflation. There is a reason why the need to control debt is now becoming felt. Since the pandemic, the global central banks have been on a giant balance sheet expansion project unprecedented in recent times. With the pandemic in motion, it was necessary to save the customer to maintain demand. But now inflation in commodities and asset price inflation is forcing a roll back in demand and there is need to make a policy shift. Even the Chinese credit impulse is on a decline indicating weak recovery.

As central banks increased money supply, there was a surge in liquidity which went into assets that led to asset price inflation. Global stock markets went on a large run without consideration to the pandemic. Supply side constraints led to price increases in many commodities and goods and services. This has led to a decline in purchasing power globally. Due to the above factors, nominal GDP increases while debt which is measured in devalued currency goes down. Hence, we are experiencing this war on savers and creditors who are losing money every day. Increase in nominal GDP is helping the stock markets as margins have improved leading to increased stock prices. Corporate debt has been going lower in some countries. However, as inflation rages on, the demand is getting impacted and leading to stagflation. The next steps seem to be to increase the taxes as it will help to pay off the debt. We expect increase in taxes in most economies as the palatable monetary policy and fiscal policy options are getting exhausted.

Impact on China

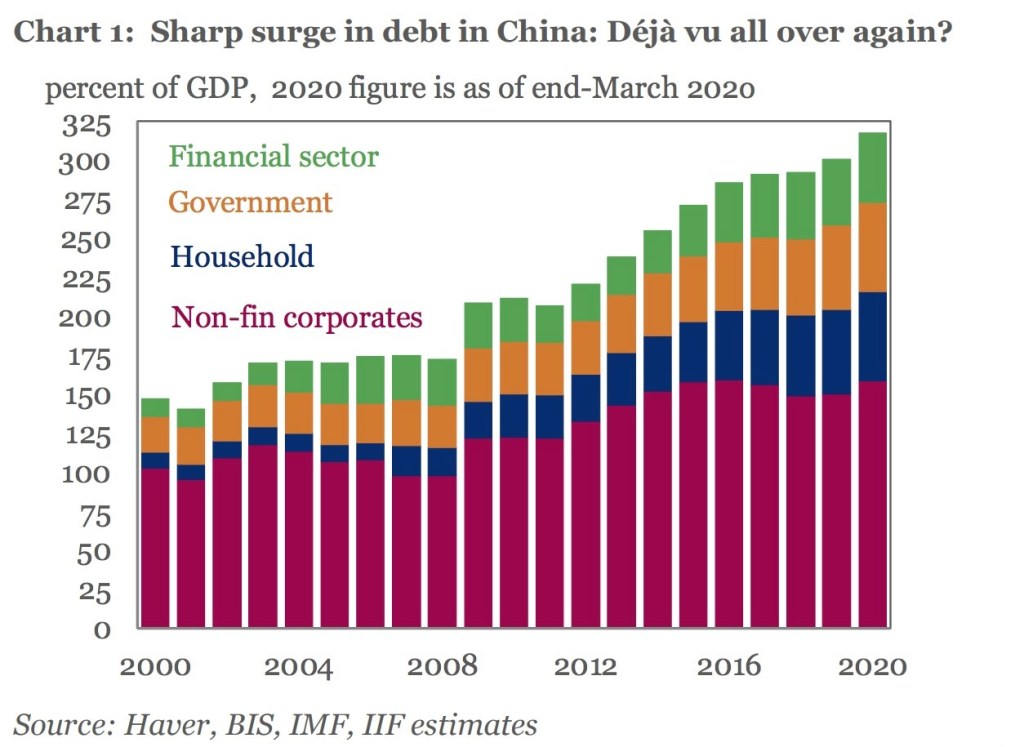

China has been growing its own debt bubble which has fueled its GDP growth. The big question however is can the titanic avoid the iceberg? Its one thing when the economy has 90% debt to GDP ratio where as one compared to 300% debt to GDP (public and private debt). This is something not seen before and there are many other factors that can impact. For e.g., most of the AMCs that have held the non-performing assets of the Chinese economy from the previous crisis have seen their assets further deteriorate. Chinese labor costs have risen in the past few years and there is now parity with neighboring countries in some sectors like textiles. Besides, been a communist country, it exerts control on how it wants to shape the economy which reduces the incentives for many companies to set up shop as there is always the danger of the axe falling. These factors coupled with an already slowing global economy is now creating a deflationary scenario for the Chinese economy.

The recent bubble bursting exercise is a tough one. Recent example is one in India where Gross NPA of scheduled commercial banks reached 11.5% in March 2018. India had a similar growth in real estate from 2007-2013. This had led to excesses in many sectors and debt burden among the corporates were the highest. Banks had given loans to many promoters without proper due diligence and were left with large non-performing assets at the end of the cycle. It took few tough regulatory norms and years of pain for the real estate to recover. Yet after the pandemic, the Gross NPA is still expected to be at a higher level in 2022 (9.8% as per RBI Financial Stability Report July 2021).

The losses from the blow out of Evergrande will mainly befall on the foreign investors who were enamored by the double-digit returns. But these losses will make a hole on their balance sheets which will have to be filled by pulling money from other places. As of this writing, new names of companies are cropping up whose bonds trade at pennies on the dollar (Sunac, Kaisa, etc.). While the Evergrande problem is more of a collateral issue (too many under construction properties made at places having less demand which means asset sale won’t fetch much), it has strong linkages to the Chinese economy as it holds 2% of the Chinese real estate market. Employees of the company are demanding their pay and money invested in wealth management products. Chinese government has always tried to resolve social unrest head on. This real estate problem can have a massive negative wealth effect on the Chinese. As mentioned in the previous articles, there are repercussions for the Australian, Japan, Germany, Canada and rest of the world markets.

China obviously has been impacted negatively from the pandemic. First, it has been accused of promoting the pandemic which is still not clear. Second, it forced many companies to look for other alternative countries to avoid the supply chain shock. China like other countries doesn’t want to devalue its currency. It wants the yuan to be the centerstage of the global economy. Therefore, it can’t follow the policies of the western governments. Also, China knows that once the wealth effect turns negative, global consumer is going to be extremely fragile to afford its products. Therefore, it needs its own citizens to become consumers of its products. The past few attempts at doing so have failed. Chinese consumers have historically relied on the housing sector to store their wealth. So much has been the addiction, that it forms the major driver of local growth. For the consumer to consume its products, it needs to have disposable income. But a majority of them have been levered up to their eye balls and can’t afford to drive the economy. China wants to remove this addiction. It wants to start a controlled fire to remove the deadwood so that the addiction dies with reduction in leverage. It is what the Chinese Premier calls “inflated growth” that the local governments have created as they had the incentive to do so (Failure would jeopardize their position). This will enable it to do well when the global economy is in downturn. We can also see similar steps taken to control the direction of the economy by increasing regulations in the digital economy. China is choosing a different direction than the western counterparts. Whether it is the right one only time will tell.

– By Nishant Maheshwari, Vishal Vora

Disclosure: This article is the opinion of the writers and should not be construed as a financial advice. Please consult your financial advisor before investing.

One thought on “Global Update – Evergrande (Part 2)”