While in our previous blog of Update on Estimated loss of 563 Crore to Mutual Fund for holding RBL Bank Share, lots of readers have requested us to give a detailed analysis on how to analyze a Banking company and what all aspects we should cover to understand Banking fundamentals.

So in this blog, we will show our viewers some simplified model of understanding core banking business along with analysis of Yes Bank and RBL Bank.

Understanding core business of Banking

The core business of Banking in India is mainly lending. The source of lending is either equity capital or borrowings or deposits from saving bank account.

Let us explain with example and go with basic maths in a simplified manner.

Suppose M/s ABC Bank wants to start lending business. It has Rs 100 in its pocket and the break up that capital is Rs 20 as equity, Rs 30 as borrowings from Debenture holder or perpetual bond or Infra Bonds or long-term bonds and remaining amount from Saving bank account holders. Now the Bank is lending Rs 100 and will charge 8% as interest. The amount borrowed by Bank in the form of borrowings and deposits is at 7% rate. Now effectively what Bank needs to do is to collects Rs 8 as interest from Customer and pay Rs 7 as interest to borrowers or they can collect Rs 100 by charging interest in a period of 10 years based on reducing balance method say Rs 2 EMI for 5 years and similarly Bank will raise long term borrowings and will match similar period.

In a simple language the method is simple. Whatever you have lent, the same is required to be repaid and effectively the margin is your real income.

Practical situation with Banks

At present what is practically happening with many banks is the Evergreening concept. In our above case, interest of Rs 8 was required to be collected from customer yearly or EMI of Rs 24 was required to be collected. But what is happening is different.

Like in case of Yes Bank (Can take name as NPA fiasco happened) or other Bank (Will not name) they aggressively lent to entities having stressed assets. Like in case of real estate, if the builder requires Rs 100 loan then they provide Rs 140 loan for 5 years with moratorium period. For Rs 40(140-100) (i.e. the amount not required) they securitize it as FDR with bank besides the project which was offered as collateral security. Now here the picture becomes interesting as the bank have safeguarded few years cycle even if the stress becomes severe. Repayment is ensured when through invoking FDR as security. The cycle still continues when your interest is considered as advance i.e capitalization of interest in account instead of receiving the same and bank charges Interest on interest. Like in our example when we were required to receive Rs 8 as interest then instead of receiving Rs 8 the bank accounted loan balance of Rs 108 as receivable in advance side and in next year charged interest on Rs 108. After telling the basic level of understanding lets analyze Yes bank and RBL Bank. The red marks are areas of concern.

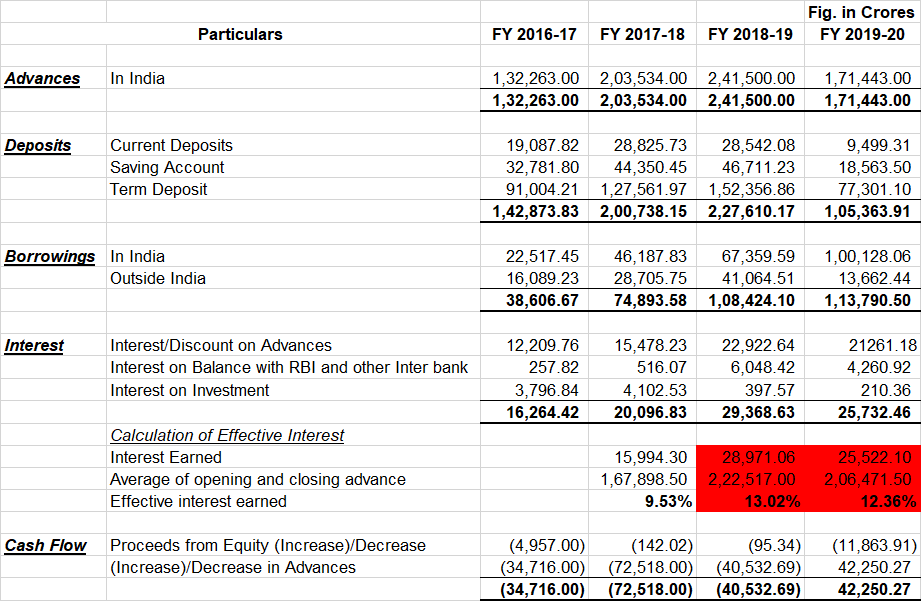

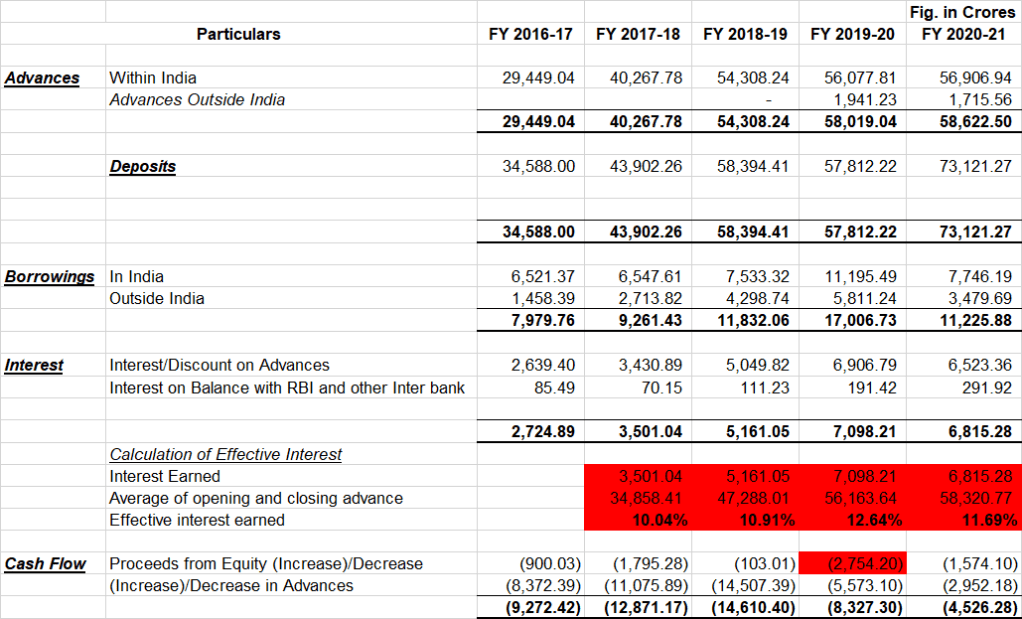

Below is the analysis of Yes Bank

Analysis of Red marks

In case of effective interest earned, the average rate at which leading banks were earning was 8% to 9% while all of a sudden the the effective interest rate for Yes bank increased from 9.53% in FY 2017-18 to 13.02% in FY 2018-19. It usually happens when we have mismatch in our advances to borrowings/equity. This usually happens when we capitalise interest portion in our advances instead of receiving them or we have given large number of unsecured loans.

It may be noted that this was the period when maximum high ranking officials in Yes Bank sold large chunks of shares before annual report got published.

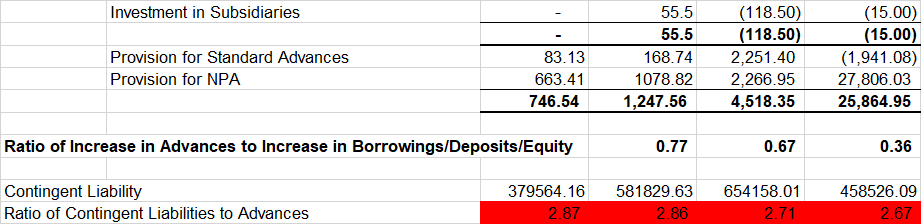

Similarly in case of contingent liability the ratio is always problematic as the aggressive loans disbursement policy forced bank to enter into high risk ventures.

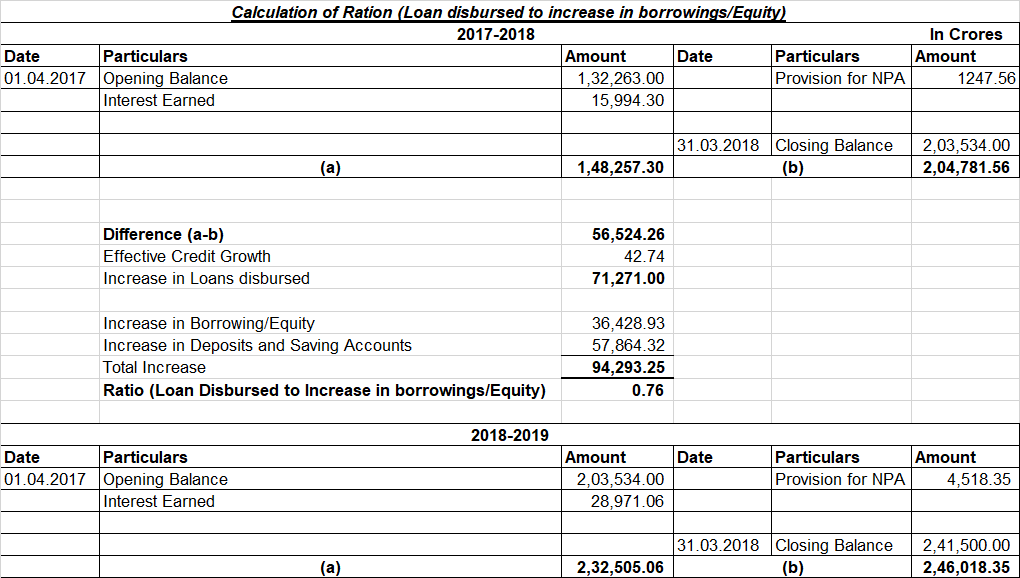

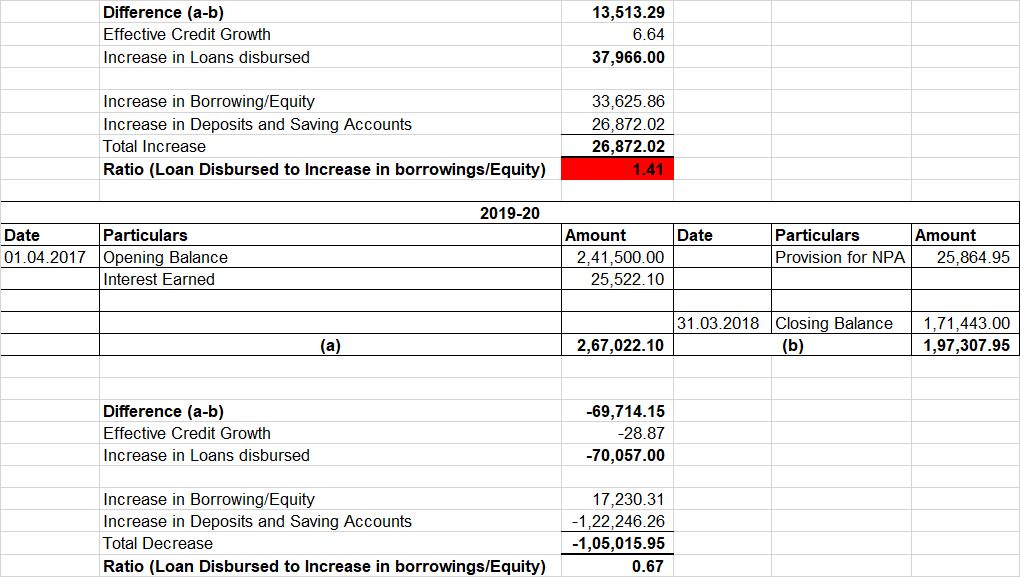

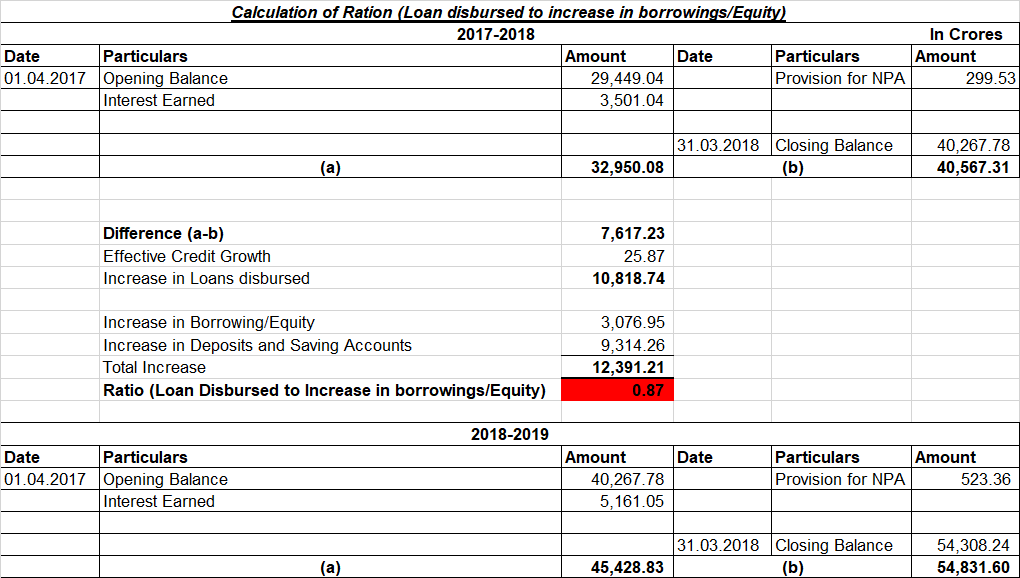

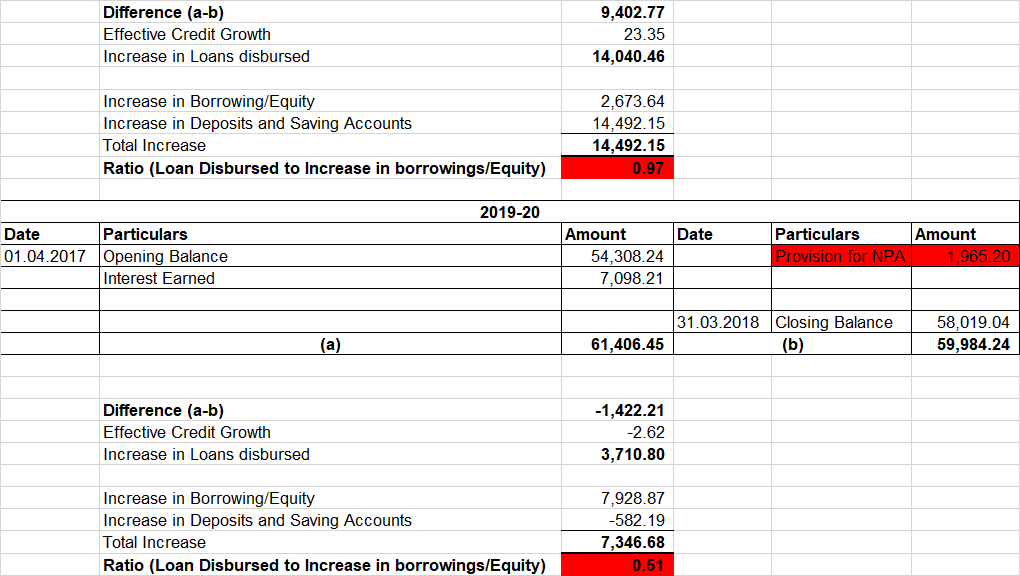

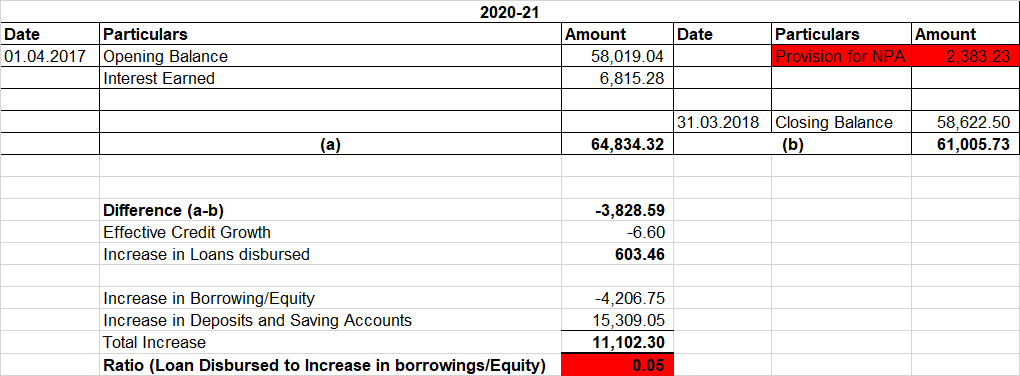

In case of Loan disbursed to increase in borrowings/Equity, the ratio is semi variable. Being statutory branch auditor for various PSU for last 10 years, we have made a range for same. When it is 0.50 to 0.90 the inflow and outflow of cash is regular in bank and is in a comfortable position. But when it crosses 0.90 and starts touching 1, the stress level in bank is at highest. So when it touched 1.41 in FY 2018-19, bank was at critical stage and the fall of bank was inevitable. Similarly when the ratio falls below 0.50 the surplus deposits or borrowings (which we will show you in RBL bank where ratio is 0.05 for FY 2020-21) are in excess of advances and slowly the margins shrink and borrowing costs become heavy.

RBL Bank Analysis

Conclusion

The above ratio represented for two banks are mathematically easy to calculate and no rocket science is required to understand the fundamentals of banks. Investors and analysts can use such analysis to find out if a bank is going to struggle in future.

Those who wish information on other banks can contact us.

– By Nishant Maheshwari & Vishal Vora

Disclosure: The above article is based on views expressed by the authors and are meant for information purpose only. Readers are requested to take investment decisions by consulting financial advisors.

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Number: 00000037522669317

Account Holder Name:Rashi Maheshwari

IFSC:SBIN0030115

Name of the Bank:SBI India, YN Road Branch, Indore, India