In last few days, we are seeing a lot of tweets about BOJ Bond buying programmes especially about a single day spike of $24 Billion Bond buying or exhausting 10 days quota of buying in one day. However, in spite of such large level of intervention, the Yield Curve Control (monetary policy action whereby a central bank purchases variable amounts of government bonds or other financial assets in order to target interest rates at a certain level) is failing. The yields of Japanese 10 years Bonds have reached to more than targeted area i.e 0.50%.

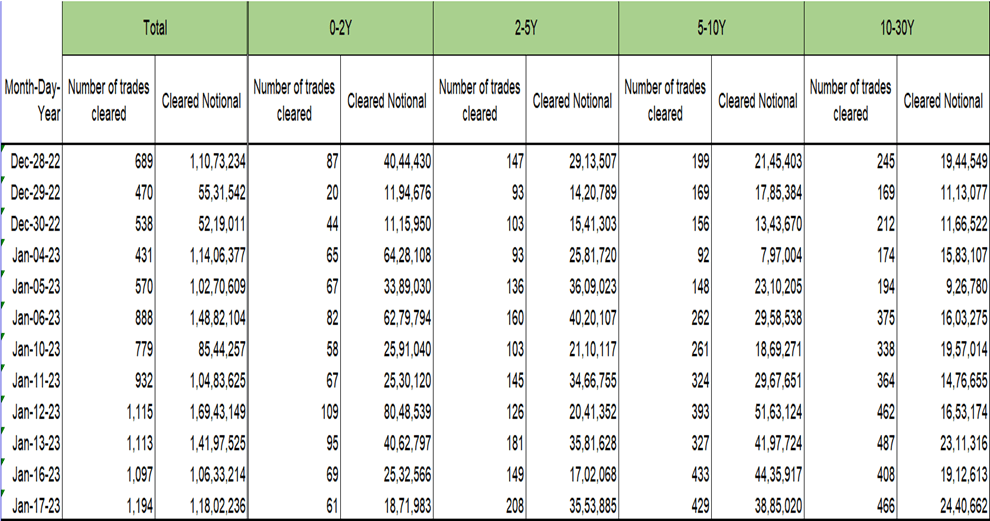

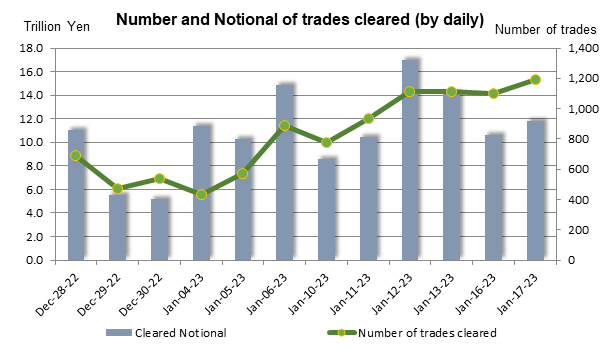

Lets look at the actual number of contracts traded in last 19 days:

Source:Japan Securities clearing corporation

Source:Japan Securities clearing corporation

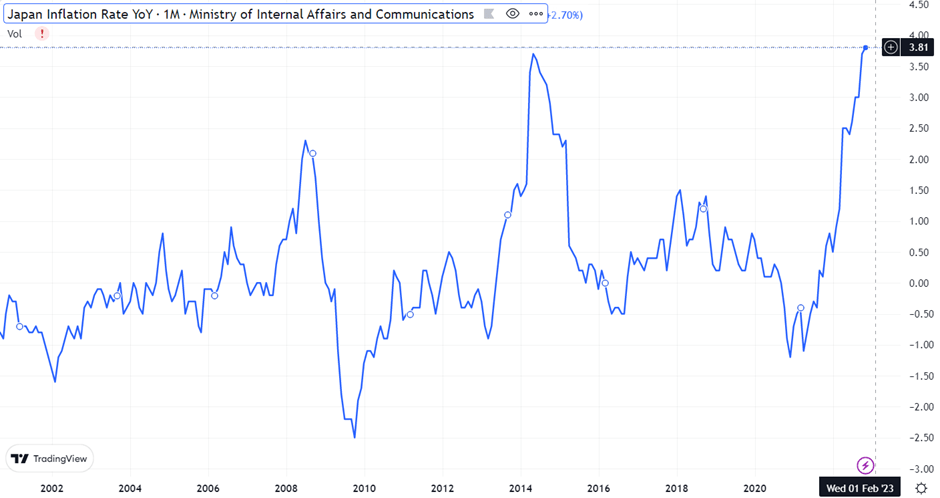

From -0.28% in 26.08.2019 to 0.59% in 18.01.2023, the era of negative interest rate In Japanese debt market seems to be fading. With jitters of inflation globally, Japan also got into turbulence of Inflationary spikes and the Inflation touched new highs and crossed highs of Nov 2014 when the CPI was reported at 3.68%

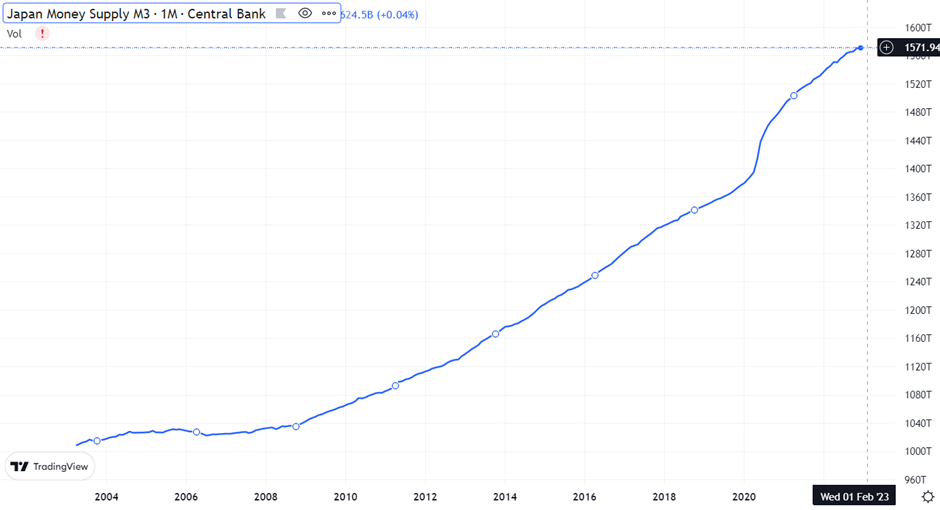

With over 36 years of constant increase in M3 money supply, the country went in hidden inflation loosing money value while deflation data remained strong. Thus the whole purchasing power became deteriorated.

Note: (M3) includes currency, deposits with an agreed maturity of up to two years, deposits redeemable at notice of up to three months and repurchase agreements, money market fund shares/units and debt securities up to two years.

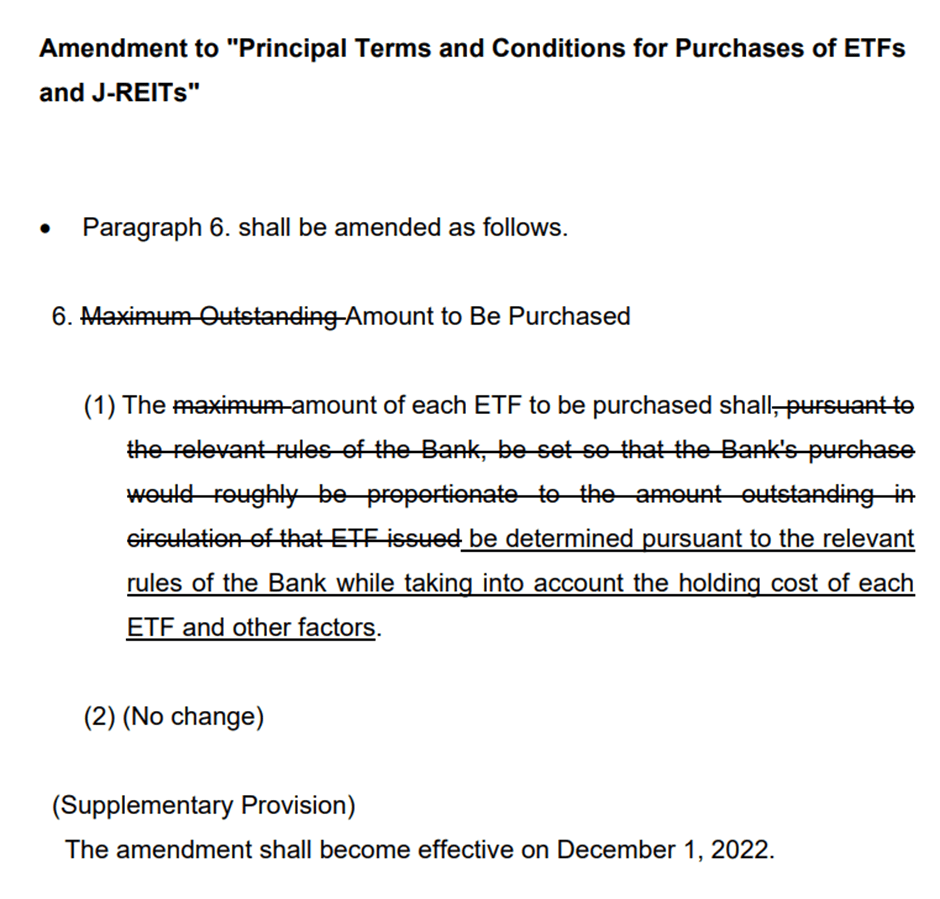

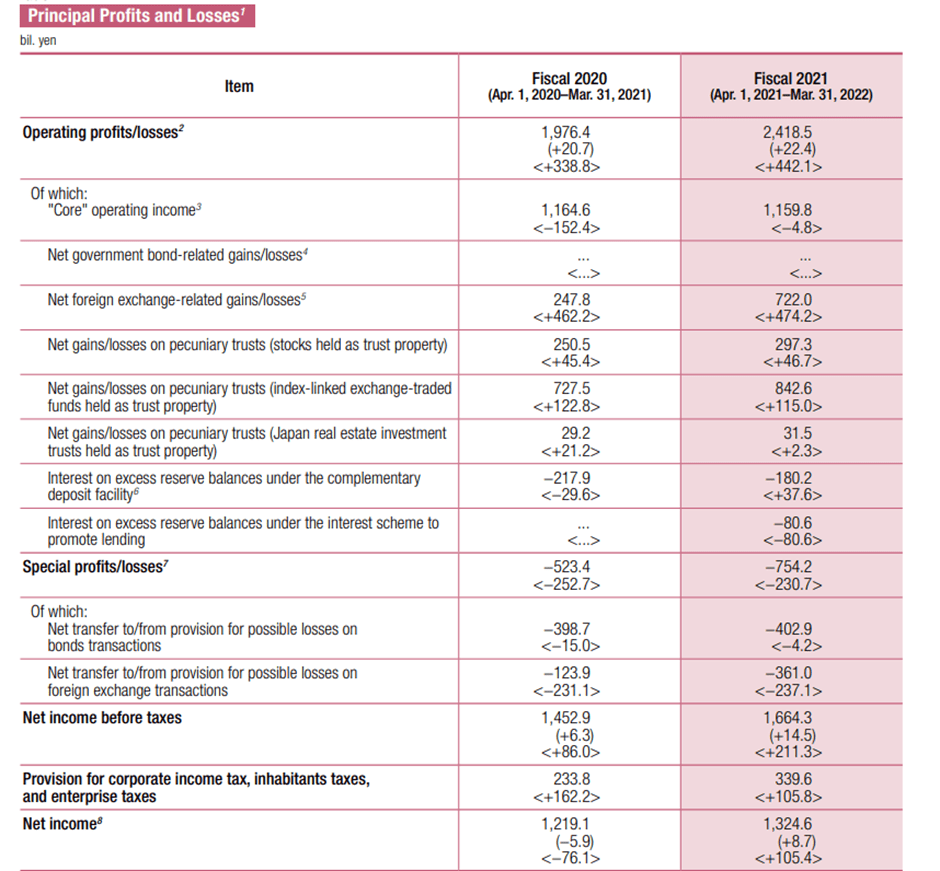

Control of Bonds & Index linked ETF

Before analysing this data, lets produce some statistics of Borrowings of Government from Ministry of Finance:

Source:Ministry of FInance, Japan

A whooping 9.70 trillion dollars of Borrowings as on 30.09.2022

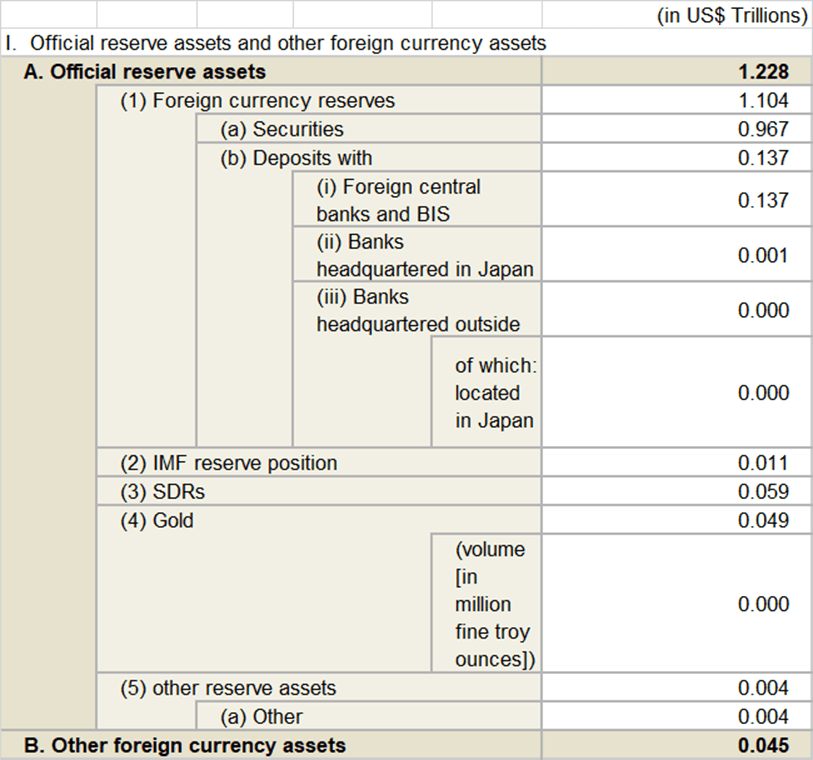

(Notes) B. Other foreign currency assets include loans to The Japan Bank for International Cooperation (JBIC) in total of $ 44.77 Billion as on 31.12.2022.

Source:Ministry of Finance Japan

Now a simple question arises in mind that what is the per day reserve of reserve of Japan in USD?

It comes out at $ 2.50 Billion and seeing the domestic consumption of Japan it is more visible that the country is export dependent. So the reserves are evidence of Gross value addition in economy.

When the same is linked with Bond buying programme by Bank of Japan, the figures are more shady. In December month, BOJ bought $128 Billion Japanese Bonds($4.26 Billion per day in simple maths). In the month of Jan $78 Billion ($4.87 Billion per day in Jan till 16th Jan). All in all BOJ financed more than 50% borrowing of Government in Japan and 85% of the same borrowings are new borrowings.

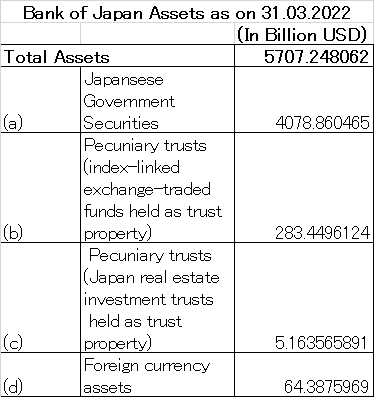

Source:Bank of Japan

NOTE:Right hand side represents the increase from last data

When the market tumbled, BOJ changed the policy and started more intervention in Financial market

Source:Bank of Japan

Source:Bank of Japan

It is always interesting to see how the bonds mark to market losses were always minimum as the Bonds became highly illiquid and so is the accounting policies where the bonds are treated as long term investment and recorded at cost and thanks to YCC due to which loss on short term bonds never arise. This time when the spread is increased for YCC, it will be interesting to see the loss in BOJ books which I am sure will be above $200 billion dollars considering the movement of -0.28 to 0.50% in Japanese 10 year Bonds.

Summary

In financial market, loss of one party is gain of other party. So is the Bond swaps and implied volatility in currency market of Japan telling. At a single time either you can save your currency or Bonds or Stock market. All the three cannot be saved in parallel. With inflation into play, it is difficult to understand how BOJ will not end up blowing its books with notional losses or how the debt will be rolled over from short term to long term. Let’s say the BOJ in trying to protect its currency and bond market blew through a huge dollar amount and hence caused the dollar to go down. This would create an artificial signal indicating bullishness when there is none. Most analysts expect Japanese central bank to fold and let the yields rise at least upto 1%. The question is when? Most likely when they are done through their dollars reserves. Now all depends on Monetary policy decision to hike interest rate.

General Conclusion on Global Macro Environment

These are interesting times. On one hand there are people who believe the bottom is in as CPI has started to fall. Well if cpi goes to 10% in one year and 0% next year it means it averaged 5% inflation. The feds official target is 2%, we are not reverting to those levels on average basis at least this decade. But given how the market participants have been incentivized to predict the feds move and position for it, there is now a direct conflict with the fed and market participants for the market participants want the fed to fold and start a rally. The problem is the fed can’t do that until they see two things

High unemployment

Low inflation

Right now none of this is available.

We see bitcoin and gold jumping and everyone is convinced we are out of the woods now. The dollar index is another reason for the bullishness.

But what if they are all linked. Also indicating the relative weakness have been corporate earnings. We haven’t seen pain yet but corporates have been warning about inherent issues regarding provisioning especially US banks. And we know tech results aren’t going to fire the markets. This is therefore very interesting and next week we shall see.

There are 2 weeks till China goes on holiday and probably some time for inflation story to play out. Once that is done, we will know if the stimulus was enough. At this moment it is raising boats. But whether Chinese consumers would like to fire economy by going into more debt? Things are interesting from a macro economic point of view for such a climate rarely exists. But for an investor these are testing times.

Join us on a learning experience and develop the edge of understanding market events so that you are able to negotiate the volatile macro environment and distortions in the markets. For more details on group, please review the link provided below:

From CA Nishant Maheshwari and Vishal Vora

Disclosure: This article is for information only and should not be construed as a financial advice.

In case you are interested in making a contribution to our writing, please do so in the following account:

Account Holder Name:Rashi Maheshwari

IFSC:SBIN0030115

Name of the Bank:SBI India, YN Road Branch, Indore, India

Account Number: 00000037522669317`

2 thoughts on “Bank of Japan-Self created Trap of 36 years”